PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038800

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038800

Automotive Hydraulics System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

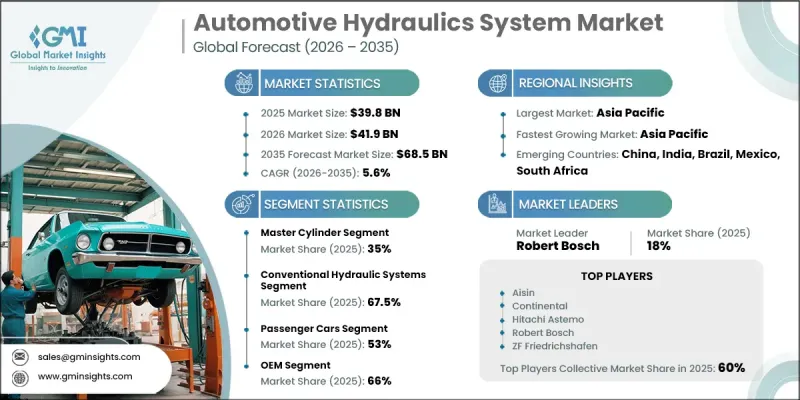

The Global Automotive Hydraulics System Market was valued at USD 39.8 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 68.5 billion by 2035.

Growing regulatory pressure to enhance vehicle safety and reduce emissions is encouraging manufacturers to integrate advanced hydraulic technologies into modern vehicles. These systems play a critical role in improving operational efficiency by minimizing energy losses while supporting essential vehicle functions. Continuous innovation in hydraulic components is enabling better performance and enhanced system reliability. The demand for improved driveline efficiency and reduced energy consumption is also contributing to market growth. In addition, the rising adoption of commercial vehicles is increasing the need for heavy-duty hydraulic solutions designed to support demanding operational requirements. The evolution of advanced hydraulic subsystems is aligning with industry goals related to fuel efficiency and performance optimization, making them an integral component in the automotive sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.8 Billion |

| Forecast Value | $68.5 Billion |

| CAGR | 5.6% |

The automotive hydraulics system market is further supported by ongoing advancements in system design and performance optimization. Manufacturers are focusing on improving efficiency and durability while ensuring compatibility with modern vehicle architectures. Increasing emphasis on reliability and cost-effectiveness continues to drive the adoption of hydraulic systems across various vehicle categories.

The master cylinder segment accounted for 35% share in 2025 and is expected to grow at a CAGR of 5.4% from 2026 to 2035. This segment is evolving toward more compact and lightweight designs that integrate seamlessly with advanced braking technologies. The growing adoption of systems requiring precise pressure control is driving demand for high-performance components capable of supporting modern vehicle requirements.

The conventional hydraulic systems segment held a share of 67.5% in 2025 and is projected to grow at a CAGR of 4.6% through 2035. Their widespread use is attributed to their simplicity, reliability, and cost efficiency. These systems continue to be preferred across a wide range of vehicles due to their ease of implementation and proven performance, particularly in applications where affordability and durability are key considerations.

U.S. Automotive Hydraulics System Market reached USD 6.8 billion in 2025. Market growth in the region is supported by continuous advancements in vehicle technology and increasing focus on energy efficiency. Manufacturers are integrating advanced hydraulic solutions to improve system performance while aligning with regulatory requirements. The adoption of innovative technologies is further contributing to the development of more efficient and responsive vehicle systems.

Key companies operating in the Global Automotive Hydraulics System Market include Robert Bosch, ZF Friedrichshafen, Continental, Aisin, Hitachi Astemo, Advics, Akebono Brake, Knorr-Bremse, Mando, and BWI. Companies in the Automotive Hydraulics System Market are focusing on innovation, efficiency, and technological integration to strengthen their market position. They are investing in advanced component design to improve performance and reduce energy losses. Many players are developing systems that align with modern vehicle requirements, including compatibility with electrified platforms. Strategic collaborations and partnerships are helping companies expand their capabilities and reach new markets. Additionally, firms are enhancing manufacturing processes to improve product quality and reduce costs. Continuous research and development efforts, along with a focus on durability and reliability, are enabling companies to maintain a competitive edge while addressing evolving industry demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Application

- 2.2.4 Vehicle

- 2.2.5 Technology

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing vehicle production and sales

- 3.2.1.2 Stricter safety and emission regulations

- 3.2.1.3 Demand for improved fuel efficiency

- 3.2.1.4 Growth in commercial vehicles segment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system complexity and integration cost

- 3.2.2.2 Dependence on traditional hydraulic fluids and components

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in electric and hybrid vehicles

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Aftermarket replacements and retrofits

- 3.2.3.4 Development of eco-friendly hydraulic fluids

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis (Driven by Primary Research)

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 Environmental Protection Agency (EPA)

- 3.5.1.2 California Air Resources Board (CARB)

- 3.5.2 Europe

- 3.5.2.1 European Commission - F-Gas Regulation

- 3.5.2.2 United Nations Economic Commission for Europe (UNECE) - ATP Agreement

- 3.5.3 Asia Pacific

- 3.5.3.1 Ministry of Ecology and Environment of China

- 3.5.3.2 Ministry of Land, Infrastructure, Transport and Tourism (MLIT), Japan

- 3.5.4 Latin America

- 3.5.4.1 Agencia Nacional de Transportes Terrestres (ANTT), Brazil

- 3.5.4.2 Secretaria de Infraestructura, Comunicaciones y Transportes (SICT), Mexico

- 3.5.5 Middle East & Africa

- 3.5.5.1 Emirates Authority for Standardization and Metrology (ESMA)

- 3.5.5.2 South African Bureau of Standards (SABS)

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Trade data analysis (Driven by paid database)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Capacity & production landscape (Driven by primary research)

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.13 Cost breakdown analysis

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Master cylinder

- 5.3 Slave / wheel cylinder

- 5.4 Hydraulic pumps (Steering & ABS specific)

- 5.5 Hoses & tubing

- 5.6 Reservoirs

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Brake systems

- 6.3 Steering systems

- 6.4 Suspension systems

- 6.5 Clutch systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Conventional hydraulic systems

- 8.3 Electro-hydraulic system

Chapter 9 Market Estimates & Forecast, By Sales channel, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.4.8 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Aisin

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 Hitachi Astemo

- 11.1.5 Knorr-Bremse

- 11.1.6 Robert Bosch

- 11.1.7 Schaeffler

- 11.1.8 ZF Friedrichshafen

- 11.2 Regional players

- 11.2.1 ADVICS

- 11.2.2 BWI

- 11.2.3 Eaton

- 11.2.4 FTE Automotive

- 11.2.5 JTEKT

- 11.2.6 KYB

- 11.2.7 Mando

- 11.2.8 Parker Hannifin

- 11.3 Emerging players

- 11.3.1 Brembo

- 11.3.2 Dantal Hydraulics

- 11.3.3 Hawe Hydraulik

- 11.3.4 Nissin Kogyo