PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038803

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038803

Foam Plastics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

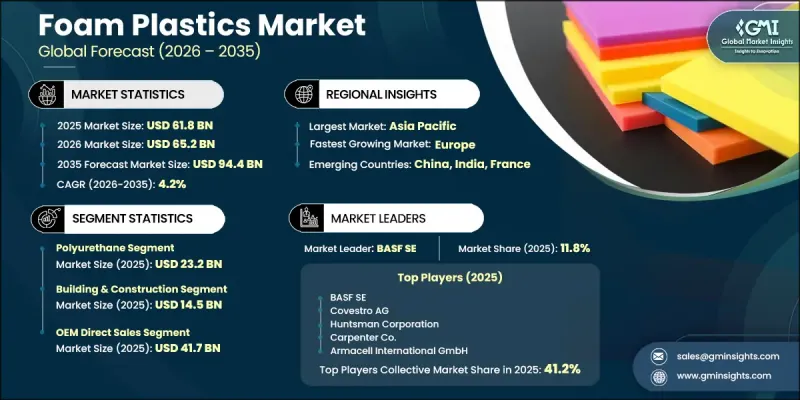

The Global Foam Plastics Market was valued at USD 61.8 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 94.4 billion by 2035.

Foam plastics are lightweight polymer-based materials formed with a cellular structure that delivers strong insulation performance and versatile mechanical properties. These materials are produced by introducing gas into molten resin through chemical or mechanical foaming techniques, resulting in open-cell or closed-cell configurations tailored to end-use needs. Their unique combination of thermal resistance, cushioning ability, buoyancy, and energy absorption makes them essential across construction, packaging, automotive, furniture, footwear, and sports industries. They are also valued for resistance to moisture, chemicals, and environmental wear, enabling both indoor and outdoor applications across residential, commercial, and industrial environments. Advances in manufacturing technologies such as extrusion foaming, injection molding, and bead expansion have improved precision in density and cell structure control. Additionally, emerging innovations in nanotechnology integration and bio-based polymers are enhancing performance while supporting sustainability goals. Growing demand across energy-efficient construction and lightweight automotive components continues to accelerate adoption across global markets over the forecast period significantly expanding.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $61.8 Billion |

| Forecast Value | $94.4 Billion |

| CAGR | 4.2% |

The polyurethane segment reached USD 23.2 billion in 2025. Its strong market position is driven by widespread use in both flexible and rigid foam applications across multiple industries. Flexible polyurethane foams are extensively used in mattresses, seating, and cushioning products due to their comfort, resilience, and durability, while rigid polyurethane foams are widely adopted for insulation purposes in refrigeration systems, building envelopes, and cold storage infrastructure because of their superior thermal resistance. The segment benefits from ongoing advancements in environmentally friendly foaming technologies, including water-blown and carbon dioxide-blown processes, which help reduce ecological impact while preserving high-performance characteristics required in demanding industrial and commercial applications.

The building and construction applications segment reached USD 14.5 billion in 2025, owing to rising demand for high-performance insulation materials in global infrastructure development. Foam-based insulation products are widely used in wall cavities, roofing systems, and foundation structures, where their high thermal resistance and superior R-value per inch enable more efficient energy performance compared to conventional alternatives. These materials also support continuous insulation systems on exterior walls and under-slab installations, helping reduce thermal bridging and improve overall building efficiency. Increasingly stringent energy regulations and green building standards are further driving adoption as developers and contractors prioritize materials that enhance energy savings, occupant comfort, and long-term structural performance.

North American Foam Plastics Market is projected to grow from USD 20.1 billion in 2025 to USD 31.2 billion by 2035, supported by strong expansion in construction activity across residential, commercial, and infrastructure renovation projects. Regulatory frameworks focused on energy efficiency across the United States and Canada are encouraging the use of advanced insulation materials in both new builds and retrofit applications. Demand is also reinforced by the region's well-established cold chain logistics network serving food and pharmaceutical industries, where foam insulation is essential for refrigerated warehouses, transport vehicles, and shipping containers. These factors collectively contribute to sustained market growth and stable demand for high-performance foam plastic solutions.

Covestro AG, BASF SE, DuPont, Owens Corning, Sealed Air Corporation, Armacell International GmbH, Carpenter Co., Huntsman Corporation, Rogers Corporation, Toray Plastics (America), Inc., Trocellen GmbH, Zotefoams plc, Sekisui Chemical Co., Ltd., JSP Corporation, and General Plastics Mfg. Co. are among the leading participants in the foam plastics industry. Companies operating in the foam plastics market are strengthening their market position through a combination of innovation, sustainability initiatives, and strategic expansion efforts. They are heavily investing in research and development to introduce advanced materials with improved thermal efficiency, durability, and reduced environmental impact. Many players are adopting bio-based polymers, eco-friendly foaming agents, and recycling technologies to align with global sustainability goals. Companies are also expanding production capacities, forming strategic partnerships, and entering emerging regional markets to strengthen distribution networks and customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Application

- 2.2.3 Sales channel

- 2.2.4 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane

- 5.3 Polystyrene

- 5.4 Polyolefin

- 5.5 Phenolic

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Building & Construction

- 6.2.1 Roofing Insulation

- 6.2.2 Wall Insulation

- 6.2.3 Flooring Insulation

- 6.2.4 Pipe Insulation

- 6.2.5 Others

- 6.3 Packaging

- 6.3.1 Protective Packaging

- 6.3.2 Food Containers

- 6.3.3 Electronics Packaging

- 6.3.4 Others

- 6.4 Automotive

- 6.4.1 Seating & Cushions

- 6.4.2 Headliners & Interior Trim

- 6.4.3 Dashboards & Doors

- 6.4.4 Others

- 6.5 Furniture & Bedding

- 6.5.1 Upholstered Furniture

- 6.5.2 Mattresses & Toppers

- 6.5.3 Pillows

- 6.5.4 Others

- 6.6 Footwear

- 6.7 Sports & Recreational

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Sales Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 OEM Direct Sales

- 7.3 Indirect Sales

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF SE

- 9.2 Covestro AG

- 9.3 Huntsman Corporation

- 9.4 Carpenter Co.

- 9.5 Armacell International GmbH

- 9.6 Sealed Air Corporation

- 9.7 General Plastics Mfg. Co.

- 9.8 DuPont

- 9.9 Owens Corning

- 9.10 Rogers Corporation

- 9.11 Toray Plastics (America), Inc.

- 9.12 Trocellen GmbH

- 9.13 Zotefoams plc

- 9.14 Sekisui Chemical Co., Ltd.

- 9.15 JSP Corporation