PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045735

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045735

Dump Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

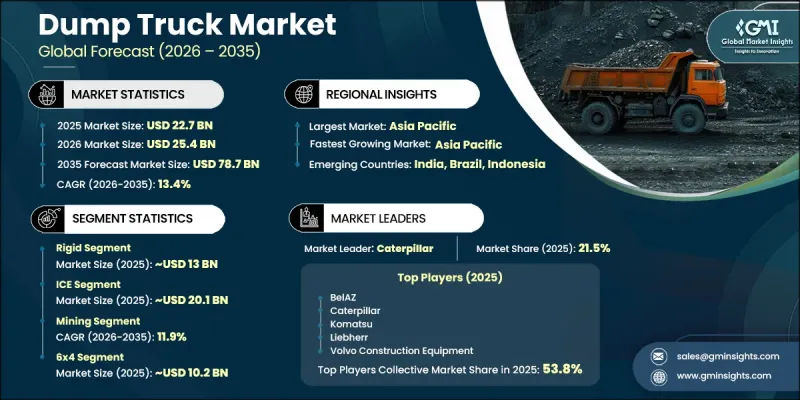

The Global Dump Truck Market was valued at USD 22.7 billion in 2025 and is estimated to grow at a CAGR of 13.4% to reach USD 78.7 billion by 2035.

Strong growth in construction and mining activities worldwide is significantly contributing to the rising demand for dump trucks across multiple industries. Increasing investments in infrastructure development, large-scale excavation projects, and mineral extraction activities are creating sustained demand for heavy-duty hauling equipment. In addition, the market is witnessing a shift toward high-value electric, hybrid, and autonomous dump trucks, which command higher average selling prices compared to conventional internal combustion engine models. Growing focus on automation and operational efficiency is encouraging manufacturers to introduce advanced autonomous hauling technologies equipped with intelligent navigation systems, sensors, cameras, and AI-powered software. These next-generation vehicles are improving workplace safety, reducing operational downtime, and enhancing material transportation efficiency across mining and construction sites. Furthermore, stricter emission standards and rising corporate sustainability goals are accelerating the adoption of low-emission and zero-emission dump trucks. Increasing government funding for public infrastructure projects between 2026 and 2029 is also expected to support near-term market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.7 Billion |

| Forecast Value | $78.7 Billion |

| CAGR | 13.4% |

The dump truck industry is evolving rapidly with growing investments in advanced hauling technologies and fleet modernization initiatives. Construction contractors and mining operators are increasingly adopting intelligent and automated equipment to improve productivity while reducing labor dependency and operational risks. Autonomous haulage systems are becoming an important revenue stream for manufacturers, extending value creation through software upgrades, retrofits, and long-term service contracts. At the same time, electrification trends are reshaping product development strategies as operators seek environmentally sustainable transportation solutions capable of supporting planned charging cycles and lower emissions. Advancements in battery technologies, vehicle connectivity, and predictive maintenance systems are further supporting market transformation. Rising demand for efficient material transportation in harsh operating conditions is also strengthening the adoption of technologically advanced dump trucks worldwide.

The articulated dump trucks segment accounted for 42.9% share in 2025 and is anticipated to register a CAGR of 14.4% through 2035. The segment is gaining significant traction as contractors and mining companies prioritize enhanced maneuverability, traction performance, and operational efficiency across rough terrains and confined worksites. The commercialization of electric articulated dump trucks is further supporting segment growth as manufacturers continue introducing advanced hauling solutions capable of delivering extended operational runtime and improved sustainability performance.

The mining segment is expected to witness the fastest growth at a CAGR of 11.9% between 2026 and 2035. Demand for dump trucks within mining operations continues to rise due to the constant requirement for transporting ore, overburden, and waste materials in challenging environments. Mining projects typically involve extended operational cycles and intensive equipment utilization, creating consistent demand for durable hauling machinery. In addition, growing global demand for critical minerals and metals is accelerating mining activities, which is further strengthening the requirement for high-capacity dump trucks across major mining regions.

U.S. Dump Truck Market reached USD 4.7 billion in 2025 and is projected to grow at a CAGR of 13.2% during 2026-2035. Growth in the country is driven by large-scale federal infrastructure investments focused on highways, bridges, freight rail systems, and urban development projects. Expanding construction activities are increasing demand for heavy-duty hauling equipment capable of supporting material transportation across infrastructure supply chains. Additionally, evolving emission regulations are encouraging manufacturers to develop cleaner and more energy-efficient dump truck technologies, including electric-powered and low-emission vehicle platforms.

Major companies operating in the Global Dump Truck Market include BelAZ, Bell Equipment, Caterpillar, Hitachi Construction Machinery, Komatsu, LGMG, Liebherr, SANY, Volvo Construction Equipment, and XCMG. Companies operating in the dump truck market are focusing heavily on technological innovation, electrification, and automation to strengthen their competitive position and expand market presence. Leading manufacturers are investing in research and development to introduce autonomous hauling systems, intelligent fleet management solutions, and energy-efficient vehicle platforms that improve productivity and operational safety. Many companies are also prioritizing the development of electric and hybrid dump trucks to meet evolving emission regulations and sustainability goals across the mining and construction industries. Strategic collaborations with mining operators, infrastructure contractors, and technology providers are helping manufacturers accelerate product deployment and expand service capabilities. In addition, businesses are strengthening aftermarket services, predictive maintenance solutions, and retrofit offerings to build long-term customer relationships while improving recurring revenue opportunities across global construction and mining operations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Truck

- 2.2.3 Axle

- 2.2.4 Propulsion

- 2.2.5 Ownership Model

- 2.2.6 Application

- 2.2.7 Distribution Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global Infrastructure Development & Urbanization

- 3.2.1.2 Expanding Mining Activities & Critical Mineral Demand

- 3.2.1.3 Expansion of Renewable Energy & Metal Extraction Projects

- 3.2.1.4 Growth in Large-Scale Construction & Quarrying Activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Capital Expenditure for Electric & Autonomous Trucks

- 3.2.2.2 Persistent Labor Shortages in Driver & Technician Roles

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging Markets Infrastructure Boom

- 3.2.3.2 Government Incentives for Zero-Emission Equipment

- 3.2.3.3 Expansion of Rare Earth & Lithium Mining Projects

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 Diesel-Electric Powertrain Technology

- 3.3.1.2 Advanced Hydraulic Control Systems

- 3.3.2 Emerging technologies

- 3.3.2.1 Hydrogen Fuel Cell Powertrain Technology

- 3.3.2.2 Solid-State Battery Technology

- 3.3.2.3 Fully Integrated Remote & Autonomous Mining Operations

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - U.S. Clean Air Act (CAA)

- 3.6.1.2 US - EPA Tier 4 Emission Regulations

- 3.6.1.3 Canada - Canadian Environmental Protection Act

- 3.6.2 Europe

- 3.6.2.1 EU - European Union Stage V Emission Standards

- 3.6.2.2 UK - Non-Road Mobile Machinery Emission Standards

- 3.6.3 Asia Pacific

- 3.6.3.1 China - China IV non-road emission standards

- 3.6.3.2 India - Bharat Stage V CEV Emission Norms

- 3.6.4 LATAM

- 3.6.4.1 Brazil - PROCONVE MAR-1 Emission Standards

- 3.6.4.2 Mexico - NOM-044-SEMARNAT Heavy Vehicle Emission Rules

- 3.6.5 MEA

- 3.6.5.1 South Africa - National Environmental Management Air Quality Act

- 3.6.5.2 GCC - GCC Diesel Emission Regulations

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Trade Data Analysis (Driven by Paid Database)

- 3.9.1 Import/Export Volume & Value Trends

- 3.9.2 Key Trade Corridors & Tariff Impact

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Installed Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Cost breakdown analysis

- 3.11.1 Raw Materials & Components Costs

- 3.11.2 Labor & Assembly Costs

- 3.11.3 Engine & Propulsion System Costs

- 3.11.4 Overhead & Facility Costs

- 3.11.5 Compliance, Testing & Certification Costs

- 3.12 Patent analysis (Driven by Primary Research)

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Impact of AI & generative AI on the market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.3 Risks, limitations & regulatory considerations

- 3.15 Electrification & energy transition impact

- 3.15.1 Battery technology advancements & cost curves

- 3.15.2 Charging infrastructure deployment in mining & construction sites

- 3.15.3 Total cost of ownership

- 3.15.4 Grid capacity & renewable energy integration

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.16.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Truck, 2022 - 2035 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Articulated

- 5.2.1 Below 50 Metric Tons

- 5.2.2 50 Metric Tons and above

- 5.3 Rigid

- 5.3.1 Below 50 metric tons

- 5.3.2 50 to 100 metric tons

- 5.3.3 101 - 200 metric tons

- 5.3.4 201 - 300 metric tons

- 5.3.5 Above 300 metric tons

Chapter 6 Market Estimates and Forecast, By Axle, 2022 - 2035 ($ Mn, Units)

- 6.1 Key trends

- 6.2 4x2

- 6.3 4x4

- 6.4 6x4

- 6.5 6x6

- 6.6 8x4

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Propulsion, 2022 - 2035 ($ Mn, Units)

- 7.1 Key trends

- 7.2 Internal Combustion Engine (ICE)

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates and Forecast, By Ownership Model, 2022 - 2035 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Mining companies

- 8.3 Rental / leasing companies

- 8.4 Others

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Construction

- 9.3 Mining

- 9.4 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn, Units)

- 10.1 Key trends

- 10.2 Direct Sales

- 10.3 Distributors/Dealers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Poland

- 11.3.8 Sweden

- 11.3.9 Norway

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Indonesia

- 11.4.6 South Korea

- 11.4.7 Thailand

- 11.4.8 Vietnam

- 11.4.9 Philippines

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Caterpillar

- 12.1.2 Komatsu

- 12.1.3 Volvo Construction Equipment

- 12.1.4 Hitachi Construction Machinery

- 12.1.5 Liebherr

- 12.1.6 BelAZ

- 12.1.7 Bell Equipment

- 12.1.8 Terex

- 12.1.9 SANY

- 12.1.10 XCMG

- 12.1.11 HD Hyundai

- 12.1.12 John Deere

- 12.2 Regional players

- 12.2.1 BEML

- 12.2.2 SINOTRUK

- 12.2.3 FAW Trucks

- 12.2.4 Dongfeng Motor

- 12.2.5 Ashok Leyland

- 12.2.6 Tata Motors

- 12.3 Emerging players

- 12.3.1 Epiroc

- 12.3.2 LGMG