PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045737

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045737

Facility Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

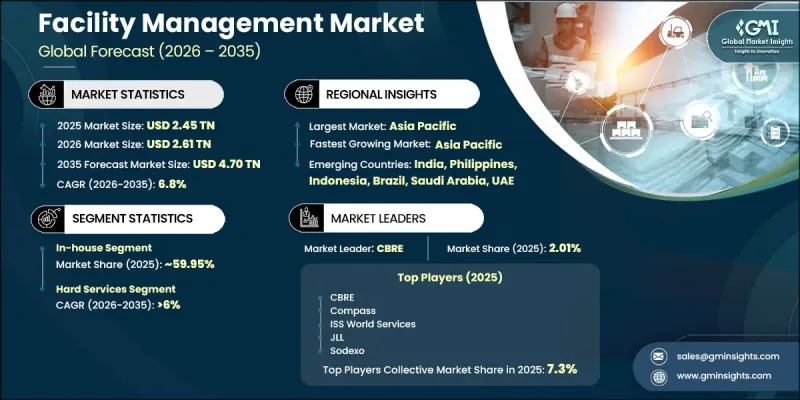

The Global Facility Management Market was valued at USD 2.45 trillion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 4.70 trillion by 2035.

Rapid urban development, expanding smart infrastructure projects, and growing demand for efficient building operations are significantly reshaping the facility management industry. Facility management has evolved far beyond conventional maintenance services and is now considered a strategic operational function that supports asset optimization, workplace efficiency, occupant safety, and sustainability goals. Modern commercial buildings, healthcare institutions, industrial facilities, and corporate campuses increasingly rely on intelligent facility management systems that integrate automation, predictive maintenance, and real-time monitoring technologies. Organizations are prioritizing advanced FM platforms that combine energy management, workspace optimization, and digital service management to improve operational visibility and reduce long-term costs. Features such as automated lighting systems, smart climate control, and digital maintenance scheduling are enhancing user experience while improving resource efficiency. Sustainability initiatives and ESG-focused operational strategies are also encouraging facility operators to adopt green building technologies and energy-efficient infrastructure solutions. The growing use of IoT-enabled systems, cloud-based management platforms, and AI-driven analytics is further accelerating digital transformation across the facility management landscape globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.45 Trillion |

| Forecast Value | $4.70 Trillion |

| CAGR | 6.8% |

The outsourced segment is expected to grow at a CAGR of 7.4% during 2026-2035. Increasing adoption of integrated facility management solutions, rising focus on cost optimization, and growing demand for specialized expertise are driving expansion within the outsourced services segment. Businesses are increasingly outsourcing non-core operational activities such as security services, cleaning operations, HVAC maintenance, and energy management to external service providers to focus more effectively on primary business functions while maintaining high operational standards.

The hard services segment accounted for 54.3% share in 2025 and is anticipated to grow at a CAGR of 6% from 2026 to 2035. This segment continues to dominate because it covers critical technical and infrastructure-related operations, including mechanical, electrical, plumbing, HVAC systems, fire protection, water management, and energy optimization services. Hard facility management services are essential for ensuring uninterrupted building performance, regulatory compliance, operational safety, and efficient asset utilization. Organizations continue to prioritize these services to minimize downtime, protect infrastructure investments, and improve long-term operational reliability.

China Facility Management Market held a 44.2% share in 2025 and generated USD 414.1 billion during 2026-2035. The country's market growth is being supported by rapid urbanization, large-scale infrastructure expansion, and increasing demand for professional property management services. Growth in commercial developments, industrial zones, healthcare infrastructure, and smart city initiatives is creating strong demand for advanced maintenance, energy management, and integrated facility management solutions. In addition, rising labor costs and increasing adoption of outsourced operational models are encouraging businesses across China to implement structured and technology-enabled facility management systems.

Major companies operating in the Global Facility Management Market include Apleona, Aramark, BGIS, CBRE, Compass, Cushman & Wakefield, IBM TRIRIGA, ISS World Services, JLL, and Sodexo. Companies operating in the Facility Management Market are focusing on digital transformation, integrated service offerings, and sustainability initiatives to strengthen their market position. Industry participants are investing heavily in smart building technologies, IoT-enabled monitoring systems, predictive maintenance platforms, and cloud-based facility management software to improve operational efficiency and service quality. Strategic mergers, acquisitions, and partnerships are helping companies expand geographic reach and diversify their service portfolios. Many providers are also emphasizing energy-efficient solutions and ESG-driven operational strategies to meet evolving client expectations and regulatory standards. In addition, businesses are enhancing workforce training, adopting automation technologies, and strengthening data analytics capabilities to deliver customized and value-driven facility management services.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Service

- 2.2.4 End Use

- 2.2.5 Organization Size

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapidly growing tourism and hospitality sectors

- 3.2.1.2 Rising demand for value-added services

- 3.2.1.3 Growing investments in construction sector

- 3.2.1.4 Supportive government initiatives for development of smart cities and business hubs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Slow adoption of outsourced facilities management services

- 3.2.2.2 Limited awareness about the benefits of advanced facility management technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for integrated FM services

- 3.2.3.2 HR tech integration & workforce analytics

- 3.2.3.3 Sustainability services & green building compliance

- 3.2.3.4 Tier 2 & tier 3 cities expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guideline

- 3.4.1 North America

- 3.4.1.1 U.S.: OSHA Workplace Safety & Energy Efficiency Regulations

- 3.4.1.2 Canada: National Building Code & Energy Efficiency Standards (NRCan)

- 3.4.2 Europe

- 3.4.2.1 Germany: Energy Saving Ordinance (EnEV) & Building Energy Act (GEG)

- 3.4.2.2 UK: Minimum Energy Efficiency Standards (MEES) & Health and Safety Regulations

- 3.4.2.3 France: Energy Performance of Buildings Directive (EPBD) Implementation

- 3.4.2.4 Italy: National Energy Efficiency Action Plan (NEEAP) Compliance

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Green Building Evaluation Standard & Energy Conservation Law

- 3.4.3.2 India: Energy Conservation Building Code (ECBC) & Smart Cities Mission Guidelines

- 3.4.3.3 Japan: Building Energy Efficiency Act & CASBEE Certification System

- 3.4.3.4 Australia: National Construction Code (NCC) & NABERS Rating System

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Energy Efficiency Plan & Green Building Council Standards

- 3.4.4.2 Mexico: NOM Energy Efficiency Standards & Sustainable Building Codes

- 3.4.4.3 Argentina: National Program for Rational Energy Use (PRONUREE)

- 3.4.5 MEA

- 3.4.5.1 UAE: Estidama Pearl Rating System & Dubai Green Building Regulations

- 3.4.5.2 Saudi Arabia: Saudi Building Code & Energy Efficiency Program (SEEP)

- 3.4.5.3 South Africa: SANS 10400-XA Energy Usage in Buildings Regulation

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 In-House

- 5.3 Outsourced

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Hard Services

- 6.2.1 Mechanical, Electrical, Plumbing & HVAC Maintenance

- 6.2.2 Energy Management

- 6.2.3 Fire Safety Systems

- 6.2.4 Water Management Systems

- 6.2.5 Asset Management

- 6.2.6 Others

- 6.3 Soft Services

- 6.3.1 Janitorial & Sanitization

- 6.3.2 Office Support & Security Services

- 6.3.3 Housekeeping

- 6.3.4 Pest Control

- 6.3.5 Catering Services

- 6.3.6 Ground Maintenance

- 6.3.7 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Healthcare

- 7.3 Business & Corporate

- 7.4 Manufacturing

- 7.5 Government & Public Sector

- 7.6 Education

- 7.7 Construction & Real Estate

- 7.8 Hospitality & Travel

- 7.9 Retail

- 7.10 Military & Defense

- 7.11 Others

Chapter 8 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Large Enterprises

- 8.3 Small & Medium Enterprises (SMEs)

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 ABM Industries

- 10.1.2 Archibus

- 10.1.3 CBRE

- 10.1.4 Compass

- 10.1.5 Cushman & Wakefield

- 10.1.6 IBM

- 10.1.7 ISS A/S

- 10.1.8 JLL

- 10.1.9 Planon

- 10.1.10 Sodexo

- 10.2 Regional Players

- 10.2.1 Apleona

- 10.2.2 Aramark

- 10.2.3 Atalian Servest

- 10.2.4 BGIS

- 10.2.5 Caverion

- 10.2.6 Emrill Services

- 10.2.7 Facilicom

- 10.2.8 Knight Facilities Management

- 10.2.9 Mitie

- 10.2.10 OCS

- 10.3 Emerging Players

- 10.3.1 Eptura

- 10.3.2 Facilio

- 10.3.3 Infogrid

- 10.3.4 UpKeep

- 10.3.5 VergeSense