PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045769

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045769

Defense Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

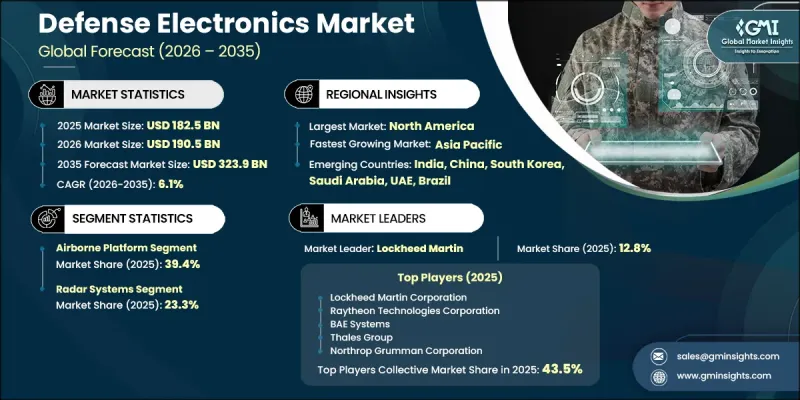

The Global Defense Electronics Market was valued at USD 182.5 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 323.9 billion by 2035.

The defense electronics industry is witnessing strong momentum due to rising investments in advanced military technologies, modernization of defense infrastructure, and growing emphasis on intelligence-driven warfare systems. Increasing geopolitical tensions and the growing need for highly secure communication systems are encouraging defense organizations to strengthen their electronic warfare capabilities. Advanced radar technologies, surveillance systems, secure communication networks, and integrated sensor platforms are becoming essential components across military operations. In addition, rising procurement of next-generation aircraft, naval systems, and unmanned defense platforms is creating sustained demand for sophisticated electronic solutions. The market is also benefiting from rapid technological advancements in memory storage, semiconductor technologies, and high-speed data processing systems that improve operational performance in critical defense environments. Furthermore, increasing government spending on defense modernization programs, combined with stronger collaboration between defense contractors and technology providers, continues to support long-term market expansion across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $182.5 Billion |

| Forecast Value | $323.9 Billion |

| CAGR | 6.1% |

The defense electronics industry is further supported by increasing mergers, acquisitions, and strategic collaborations among major companies aiming to strengthen technological capabilities and expand defense portfolios. Market participants are focusing heavily on innovation, operational efficiency, and cybersecurity integration to secure long-term defense contracts and enhance competitive positioning. The growing demand for sophisticated defense and aerospace systems is also encouraging companies to invest in highly specialized electronic technologies designed for mission-critical military operations. Additionally, continuous progress in high-performance memory and storage technologies is reshaping the industry landscape. Advanced solutions, including solid-state storage systems, high-bandwidth memory platforms, and next-generation flash technologies, are improving speed, reliability, and storage density in demanding defense applications.

The airborne platform segment accounted for 39.4% share in 2025. Growth in this segment is driven by rising deployment of advanced avionics, radar systems, and surveillance technologies across fighter aircraft, unmanned aerial vehicles, and reconnaissance platforms. Increasing investments in intelligence gathering, air superiority missions, and tactical defense operations are accelerating demand for advanced airborne electronic systems. Continuous technological advancements are also improving operational flexibility, mission accuracy, and overall combat effectiveness across airborne defense platforms.

The electronic warfare and spectrum operations segment held a 16.8% share in 2025. The segment continues to witness strong growth due to increasing demand for advanced signal interception capabilities, electronic attack systems, and communication disruption technologies. Military organizations are placing greater emphasis on spectrum dominance, cyber-electromagnetic superiority, and integrated battlefield awareness solutions to counter evolving electronic threats. Rising deployment of sophisticated jamming systems and secure defense communication technologies is further contributing to segment growth.

North America Defense Electronics Market held a 40.8% share in 2025. The region continues to maintain a dominant position due to its highly developed defense manufacturing ecosystem, substantial defense budgets, and extensive investments in military modernization initiatives. Strong research and development capabilities, combined with the presence of leading aerospace and defense technology providers, are driving innovation across radar systems, communication technologies, electronic warfare solutions, and advanced sensing platforms. Continuous focus on maintaining military technological superiority is supporting significant procurement of advanced defense electronics systems across the region.

Key companies operating in the Global Defense Electronics Market include Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems, Thales Group, and Northrop Grumman Corporation. Companies operating in the defense electronics market are strengthening their market position through continuous investments in advanced research and development, strategic partnerships, and technology-focused acquisitions. Leading players are prioritizing innovation in radar systems, electronic warfare technologies, secure communications, and integrated sensor platforms to enhance operational capabilities and secure long-term defense contracts. Many organizations are also expanding their cybersecurity offerings to address rising concerns related to digital warfare and data protection. In addition, manufacturers are increasing investments in artificial intelligence, autonomous systems, and next-generation semiconductor technologies to improve mission efficiency and real-time decision-making capabilities. Companies are also collaborating closely with government defense agencies to support modernization initiatives while expanding their global footprint through regional partnerships, localized manufacturing facilities, and long-term supply agreements to strengthen customer relationships and maintain competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform trends

- 2.2.2 Application trends

- 2.2.3 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased demand for advanced surveillance and reconnaissance systems.

- 3.2.1.2 Rapid advancements in storage and high-speed memory technologies.

- 3.2.1.3 Expansion of data storage solutions for defense applications.

- 3.2.1.4 Integration of AI and machine learning in defense electronics.

- 3.2.1.5 Rising military budgets and investments in modernization projects.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs and budget constraints in defense programs.

- 3.2.2.2 Security risks related to advanced technology implementations.

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of electronic warfare and cyber defense systems.

- 3.2.3.2 Development of next-generation communication and radar systems.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia-Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Defense budget analysis

- 3.9 Global defense spending trends

- 3.10 Regional defense budget allocation

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Middle East and Africa

- 3.10.5 Latin America

- 3.11 Trade Data Analysis (Based on Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Production Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Airborne

- 5.2.1 Military Aircraft (Fixed-Wing)

- 5.2.2 Military Helicopters (Rotary-Wing)

- 5.2.3 Unmanned Aerial Vehicles (UAVs)

- 5.3 Marine

- 5.3.1 Aircraft Carriers

- 5.3.2 Amphibious Ships

- 5.3.3 Destroyers

- 5.3.4 Frigates

- 5.3.5 Submarines

- 5.3.6 Unmanned Maritime Vehicles (UMVs)

- 5.4 Land

- 5.4.1 Dismounted Soldier Systems

- 5.4.2 Military Fighting Vehicles

- 5.4.3 Command & Control Centers

- 5.4.4 Unmanned Ground Vehicles (UGVs)

- 5.5 Space

- 5.5.1 Low Earth Orbit (LEO) Satellites

- 5.5.2 Medium Earth Orbit (MEO) Satellites

- 5.5.3 Geostationary Earth Orbit (GEO) Satellites

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Command, Control & Mission Systems

- 6.2.1 C4ISR Systems

- 6.2.2 Command & Control (C2) Systems

- 6.2.3 Battle Management Systems

- 6.2.4 Mission Planning & Decision Support Systems

- 6.2.5 Others

- 6.3 Navigation, Communication & Networking

- 6.3.1 Navigation Systems

- 6.3.2 Secure Military Communication Systems

- 6.3.3 Tactical Data Links & Networking Technologies

- 6.3.4 Displays & Human-Machine Interfaces (HMI)

- 6.3.5 Others

- 6.4 Sensing & Situational Awareness

- 6.4.1 Sensor Systems

- 6.4.2 Optronics

- 6.4.2.1 EO/IR Payloads

- 6.4.2.2 Handheld Optronic Systems

- 6.4.3 Missile Warning & Threat Detection Systems

- 6.4.4 Others

- 6.5 Radar Systems

- 6.5.1 Surveillance & Airborne Early Warning Radars

- 6.5.2 Tracking & Fire Control Radars

- 6.5.3 Multifunction Radars

- 6.5.4 Ground Penetrating Radars

- 6.5.5 Counter-Drone Radars

- 6.5.6 Airborne Moving Target Indicator (AMTI) Radars

- 6.5.7 Military Air Traffic Control Radars

- 6.5.8 Others

- 6.6 Electronic Warfare & Spectrum Operations

- 6.6.1 Electronic Support Measures (ESM)

- 6.6.2 Electronic Attack Systems

- 6.6.2.1 Jammers

- 6.6.2.2 Directed Energy Weapons

- 6.6.2.3 Electromagnetic Pulse (EMP) Weapons

- 6.6.3 Electronic Protection Systems

- 6.6.3.1 Radar Warning Receivers (RWR)

- 6.6.3.2 Laser Warning Systems (LWS)

- 6.6.3.3 Electromagnetic Shielding

- 6.6.4 Anti-Radiation & EW-Enabled Missiles

- 6.6.5 Others

- 6.7 Force Protection & Counter-Threat Systems

- 6.7.1 Counter-Unmanned Aerial Systems (C-UAS)

- 6.7.2 Active Protection & Missile Defense Electronics

- 6.7.3 Infrared Missile Warning Systems (IR-MWS)

- 6.7.4 Others

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.3.7 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

- 7.6.4 Rest of MEA

Chapter 8 Company Profiles

- 8.1 Global Players

- 8.1.1 Lockheed Martin

- 8.1.2 RTX Corporation (Raytheon Technologies Corporation)

- 8.1.3 Northrop Grumman

- 8.1.4 BAE Systems

- 8.1.5 Thales Group

- 8.1.6 Airbus SE

- 8.1.7 The Boeing Company

- 8.1.8 Leonardo S.p.A.

- 8.1.9 L3Harris Technologies

- 8.2 Regional Players

- 8.2.1 General Dynamics

- 8.2.2 Rheinmetall AG

- 8.2.3 Safran

- 8.2.4 Saab AB

- 8.2.5 Israel Aerospace Industries

- 8.2.6 Elbit Systems

- 8.2.7 Tata Advanced Systems Limited

- 8.2.8 Curtiss-Wright

- 8.3 Emerging Players

- 8.3.1 DIGICOM Electronics

- 8.3.2 Kaynes Technology India Limited (KTIL)