PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045770

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045770

Automotive Intelligent Cockpit Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

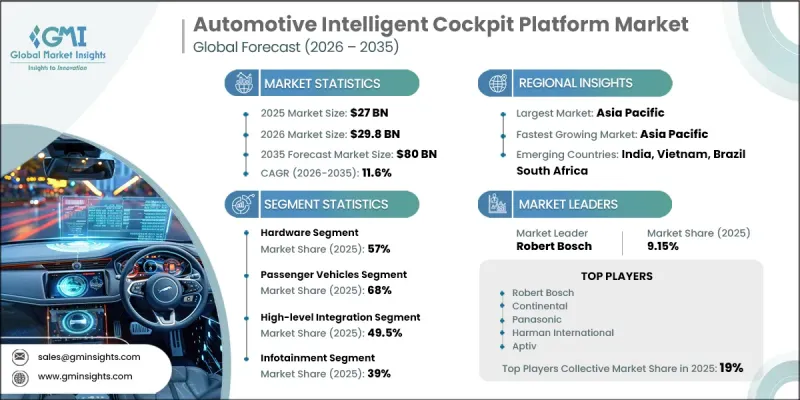

The Global Automotive Intelligent Cockpit Platform Market was valued at USD 27 billion in 2025 and is estimated to grow at a CAGR of 11.6% to reach USD 80 billion by 2035.

The industry is gaining significant momentum due to the rapid adoption of connected mobility technologies and the growing transition toward software-defined vehicles. Automakers are increasingly integrating infotainment systems, navigation platforms, advanced driver assistance functions, connectivity tools, and vehicle control operations into centralized cockpit ecosystems to deliver seamless digital experiences for drivers and passengers. Rising consumer expectations for intelligent, interactive, and personalized in-vehicle environments are further accelerating market expansion. In addition, continuous advancements in artificial intelligence, cloud computing, machine learning, and real-time data processing technologies are transforming vehicle interiors into highly adaptive digital platforms. These innovations are improving voice interaction, predictive customization, multi-screen management, and overall system responsiveness. Regulatory requirements related to cybersecurity, driver safety, and distraction management are also encouraging manufacturers to develop more secure and reliable cockpit architectures. As a result, the automotive intelligent cockpit platform market is evolving toward highly integrated, AI-driven, and software-centric ecosystems capable of delivering enhanced connectivity, convenience, and user engagement across modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27 Billion |

| Forecast Value | $80 Billion |

| CAGR | 11.6% |

The automotive intelligent cockpit platform industry is witnessing rapid technological transformation as vehicle manufacturers prioritize advanced digital experiences and enhanced software functionality. Automakers are increasingly investing in centralized computing architectures that allow multiple in-vehicle systems to operate through unified software platforms. This transition is helping manufacturers improve operational efficiency, simplify hardware complexity, and accelerate feature deployment timelines. The growing integration of digital displays, smart sensors, voice-controlled systems, and connected services is also improving user interaction and in-vehicle convenience. Furthermore, rising demand for over-the-air software updates and real-time system diagnostics is supporting the expansion of intelligent cockpit technologies across passenger and commercial vehicles. Increasing collaboration between automotive manufacturers and technology companies is further accelerating innovation within the market.

The passenger vehicles segment accounted for 68% share in 2025. The segment continues to dominate due to rising consumer demand for advanced infotainment systems, connected vehicle technologies, and interactive digital interfaces. Intelligent cockpit platforms have become central to modern passenger vehicle design by enabling the integration of digital instrument clusters, infotainment systems, navigation tools, vehicle monitoring functions, and driver assistance visualization within a unified operating environment. Automakers are increasingly focusing on delivering immersive and user-friendly cabin experiences supported by real-time computing capabilities and enhanced graphical performance. Rising demand for personalized driving experiences, smart connectivity, and integrated mobility solutions is further contributing to the strong growth of the passenger vehicle segment across global automotive markets.

The high-level integration segment held a 49.5% share in 2025. The segment is expanding rapidly due to increasing industry preference for integrated computing architectures capable of combining multiple cockpit functions into a centralized system. High-level integration platforms enable automakers to unify infotainment systems, digital displays, connectivity tools, and vehicle control operations within a single framework, improving operational efficiency and reducing hardware complexity. This approach also supports faster software deployment, improved data synchronization, and enhanced system performance across connected vehicle ecosystems. Automakers are increasingly adopting these platforms to accelerate product development cycles and support the growing demand for feature-rich digital cabin environments. Continuous advancements in semiconductor technologies and software optimization are further strengthening segment growth.

China Automotive Intelligent Cockpit Platform Market held a 54% share, generating USD 4.3 billion in 2025. The country continues to lead regional market growth due to rapid automotive digitalization, strong consumer demand for advanced in-vehicle technologies, and expanding adoption of connected mobility solutions. Rising urbanization and increasing preference for intelligent cabin experiences are encouraging automotive manufacturers to integrate advanced cockpit systems across a wide range of vehicle categories. Domestic automakers and technology-focused automotive companies are heavily investing in digital vehicle ecosystems designed to improve infotainment functionality, occupant monitoring, connectivity, and driver assistance visualization. In addition, China's strong manufacturing capabilities, expanding electric vehicle industry, and rapid adoption of smart mobility technologies continue to position the country as a major innovation hub for intelligent cockpit platform development across the Asia Pacific region.

Major companies operating in the Global Automotive Intelligent Cockpit Platform Market include Robert Bosch, Continental, Panasonic, Harman International, Aptiv, EcarX, NVIDIA, Advanced Micro Devices, Denso, and Qualcomm Technologies. Companies operating in the automotive intelligent cockpit platform market are implementing multiple strategic initiatives to strengthen their market position and expand technological capabilities. Leading players are investing heavily in artificial intelligence, cloud-enabled computing systems, and software-defined vehicle platforms to improve cockpit functionality and user experience. Strategic partnerships between automotive manufacturers, semiconductor companies, and software developers are becoming increasingly important for accelerating innovation and reducing product development timelines. Many companies are also focusing on advanced display technologies, voice recognition systems, and real-time connectivity solutions to enhance digital cabin experiences. Expansion of research and development centers, increased investments in cybersecurity infrastructure, and adoption of over-the-air update technologies are further supporting competitive growth strategies.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Component

- 2.2.4 Platform

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing rollout of 5G networks

- 3.2.1.2 Rising consumer demand for connected experiences

- 3.2.1.3 Increasing emphasis on personalization and enhanced user experience

- 3.2.1.4 Proliferation of electric vehicles g demand for secure messaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Hardware limitations

- 3.2.2.2 Software update challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Software-Defined Vehicles (SDVs)

- 3.2.3.2 Integration of AI-powered In-Vehicle Assistants

- 3.2.3.3 Growth of Autonomous and Semi-Autonomous Driving Interfaces

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 Vehicle Data Privacy and Cybersecurity Regulations (CCPA / CPRA)

- 3.6.1.2 NHTSA Vehicle Cybersecurity Guidelines

- 3.6.1.3 FCC and Connected Vehicle Communication Standards

- 3.6.1.4 Canada Digital Charter Implementation Act (CPPA)

- 3.6.2 Europe

- 3.6.2.1 EU General Data Protection Regulation (GDPR)

- 3.6.2.2 EU Cybersecurity Act & UNECE WP.29 Regulations

- 3.6.2.3 European Data Act (Connected Vehicle Data Access)

- 3.6.2.4 Germany Road Traffic Act (Automated Driving Framework)

- 3.6.3 Asia Pacific

- 3.6.3.1 China Cybersecurity Law (CSL)

- 3.6.3.2 China Personal Information Protection Law (PIPL)

- 3.6.3.3 Japan Act on Protection of Personal Information (APPI)

- 3.6.3.4 South Korea Personal Information Protection Act (PIPA)

- 3.6.3.5 India Digital Personal Data Protection Act (DPDP Act)

- 3.6.4 Latin America

- 3.6.4.1 Brazil General Data Protection Law (LGPD)

- 3.6.4.2 Mexico Federal Law on Protection of Personal Data

- 3.6.4.3 Argentina Personal Data Protection Law (Law 25.326)

- 3.6.4.4 Regional Mobility and Data Integration Initiatives

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE Federal Data Protection Law (PDPL)

- 3.6.5.2 Saudi Arabia Personal Data Protection Law (PDPL - SDAIA Framework)

- 3.6.5.3 South Africa Protection of Personal Information Act (POPIA)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Passenger vehicle

- 5.3 Commercial vehicle

Chapter 6 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Display systems

- 6.2.2 Sensors

- 6.2.3 ECUs

- 6.2.4 Others

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates & Forecast, By Platform, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 SoC-based

- 7.3 High-level Integration

- 7.4 Personalized

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 Infotainment

- 8.3 Navigation

- 8.4 Driver assistance

- 8.5 Connectivity & communication

- 8.6 Climate control

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Norway

- 9.3.8 Netherlands

- 9.3.9 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Advanced Micro Devices

- 10.1.2 Aptiv

- 10.1.3 Continental

- 10.1.4 Denso

- 10.1.5 DXC Technology Company

- 10.1.6 Elektrobit

- 10.1.7 Forvia Hella

- 10.1.8 Infineon Technologies

- 10.1.9 Intel

- 10.1.10 LG Electronics

- 10.1.11 MediaTek

- 10.1.12 NVIDIA

- 10.1.13 NXP Semiconductors

- 10.1.14 Panasonic Automotive Systems

- 10.1.15 Qualcomm Technologies

- 10.1.16 Robert Bosch

- 10.1.17 Visteon

- 10.2 Regional Players

- 10.2.1 Baidu

- 10.2.2 Desay SV Automotive

- 10.2.3 HiRain Technologies

- 10.2.4 Horizon Robotics

- 10.2.5 Huawei Technologies

- 10.2.6 Joyson Electronics

- 10.2.7 NavInfo

- 10.2.8 Neusoft

- 10.2.9 ThunderSoft