PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045773

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045773

Robotic Vacuum Cleaner Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

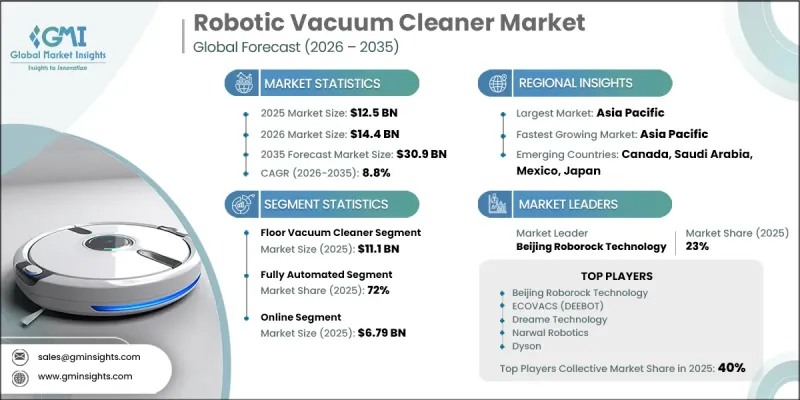

The Global Robotic Vacuum Cleaner Market was valued at USD 12.5 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 30.9 billion by 2035.

Rising awareness regarding indoor cleanliness, healthier living environments, and improved air quality is significantly contributing to market growth. Consumers are increasingly adopting robotic vacuum cleaners to reduce dust accumulation, allergens, pet hair, and airborne particles inside residential spaces, particularly in densely populated urban homes with limited ventilation. Advanced robotic cleaning devices equipped with HEPA filtration systems, enhanced suction capabilities, and automated cleaning schedules are gaining widespread popularity for their ability to maintain consistent floor hygiene with minimal manual effort. Consumer attitudes toward home sanitation have shifted considerably in recent years, leading to stronger demand for proactive and routine cleaning solutions rather than occasional deep-cleaning practices. Automated robotic vacuum cleaners support this trend by offering touch-free cleaning operations and scheduled maintenance that help minimize exposure to dust and debris. As smart home adoption continues to rise globally, robotic vacuum cleaners are increasingly viewed as long-term lifestyle and wellness investments rather than simple convenience appliances. Technological advancements in navigation systems, AI-powered mapping, obstacle detection, and smart connectivity features are further strengthening product demand across residential markets worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.5 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 8.8% |

The floor vacuum cleaner segment accounted for USD 11.1 billion in 2025. Consumer demand for efficient and easy-to-operate floor cleaning solutions continues to rise across different flooring surfaces, including hardwood, tiles, and carpets. While conventional vacuum cleaners remain widely used because of their affordability and strong cleaning performance, robotic alternatives are rapidly gaining preference due to increasing urbanization and changing lifestyles. Growing numbers of apartment and compact housing developments are also encouraging consumers to adopt faster and more convenient cleaning technologies for daily use.

The fully automated segment held a 72% share in 2025. Rising consumer preference for reduced manual involvement in household cleaning activities is driving strong adoption of fully automated robotic vacuum cleaners. These products utilize intelligent sensors, advanced mapping technologies, autonomous navigation systems, and self-adjusting cleaning capabilities to complete cleaning tasks independently. Consumers are increasingly valuing the convenience of automated cleaning solutions that consistently maintain cleanliness without requiring regular supervision or operational effort.

United States Robotic Vacuum Cleaner Market accounted for 77.9% share and generated USD 3.2 billion in 2025. Demand across the country remains strong due to growing consumer preference for convenience-oriented, hygienic, and time-saving household appliances. Increasing adoption of smart home ecosystems and rising consumer spending on connected home technologies are accelerating sales of robotic vacuum cleaners throughout the region. Consumers in the United States continue to prioritize cleaning products that deliver reliable performance, user-friendly functionality, and versatile cleaning capabilities for residential applications.

Major companies operating in the Global Robotic Vacuum Cleaner Market include Beijing Roborock Technology, ECOVACS (DEEBOT), Samsung Electronics, LG Electronics, Dyson, SharkNinja, Eufy, Haier Group, Hoover (TTI), Bissell, Vorwerk (Kobold), Miele, Cecotec, Viomi, Dreame Technology, Narwal Robotics, SwitchBot, Wyze Labs, ILIFE, Proscenic, and Lefant. Companies operating in the robotic vacuum cleaner market are focusing heavily on product innovation, smart technology integration, and portfolio expansion to strengthen their market position. Manufacturers are investing in artificial intelligence, advanced navigation systems, LiDAR mapping, and self-emptying technologies to improve cleaning efficiency and user convenience. Businesses are also introducing connected features such as voice assistant compatibility, mobile app controls, and personalized cleaning schedules to enhance customer engagement. Strategic partnerships with smart home ecosystem providers and expansion into emerging markets are helping brands increase their global reach. In addition, companies are prioritizing sleek product designs, improved battery performance, and multi-surface cleaning capabilities to differentiate their offerings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Operation mode

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing health & hygiene awareness

- 3.2.1.2 Growth of smart homes & IoT ecosystems

- 3.2.1.3 Advancements in robotics & AI

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost sensitivity

- 3.2.2.2 Maintenance & after-sales issues

- 3.2.3 Opportunities

- 3.2.3.1 Product customization & localization

- 3.2.3.2 Maintenance & after-sales issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Safety & certification standards (UL, CE, FCC)

- 3.7.2 Data privacy regulations (GDPR, CCPA impact)

- 3.7.3 E-waste & environmental compliance (WEEE, ROHS)

- 3.7.4 Energy efficiency standards by region

- 3.7.5 Cybersecurity regulations for smart devices

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (2022-2025)

- 3.8.2 Pricing strategy by player type (premium/mid-range/budget)

- 3.8.3 Price elasticity of demand

- 3.8.4 Regional price variation analysis

- 3.9 Trade data analysis (driven by paid data base)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.11.1 Channel coverage by region & format (modern vs. Traditional trade)

- 3.11.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.11.3 Direct-to-consumer vs. retail partnership models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Floor vacuum cleaner

- 5.3 Pool vacuum cleaner

- 5.4 Window vacuum cleaner

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Estimates and Forecast, By Operation Mode, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Fully automated

- 7.3 Remote control

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 Company websites

- 8.2.2 E-commerce platforms

- 8.3 Offline

- 8.3.1 Department stores

- 8.3.2 Supermarkets/hypermarkets

- 8.3.3 Other retail stores (specialty kitchenware stores, etc)

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Beijing Roborock Technology

- 10.1.2 ECOVACS (DEEBOT)

- 10.1.3 Samsung Electronics

- 10.1.4 LG Electronics

- 10.1.5 Dyson

- 10.1.6 SharkNinja

- 10.1.7 Eufy

- 10.2 Regional players

- 10.2.1 Haier Group

- 10.2.2 Hoover (TTI)

- 10.2.3 Bissell

- 10.2.4 Vorwerk (Kobold)

- 10.2.5 Miele

- 10.2.6 Cecotec

- 10.2.7 Viomi

- 10.3 Emerging players

- 10.3.1 Dreame Technology

- 10.3.2 Narwal Robotics

- 10.3.3 SwitchBot

- 10.3.4 Wyze Labs

- 10.3.5 ILIFE

- 10.3.6 Proscenic

- 10.3.7 Lefant