PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045775

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045775

Third Party Payment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

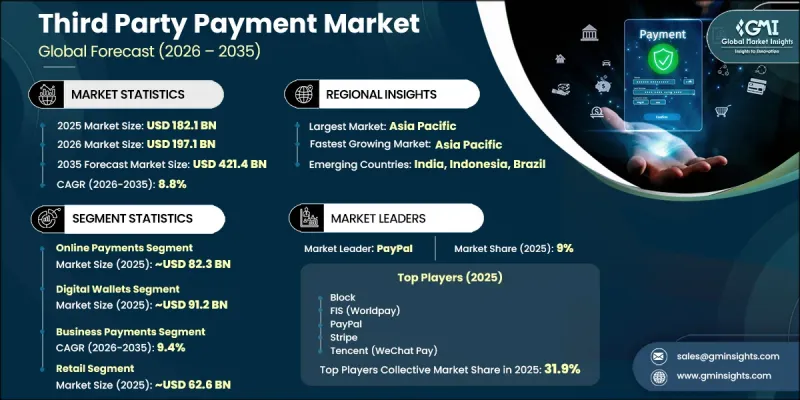

The Global Third Party Payment Market was valued at USD 182.1 billion in 2025 and is estimated to grow at a CAGR of 8.8% to reach USD 421.4 billion by 2035.

Market revenue is generated through transaction commissions, payment gateway services, acquiring fees, subscription-based software solutions, fraud prevention tools, analytics services, currency exchange processing, and embedded financial products rather than traditional bank-operated payment systems. The market is expanding rapidly as digital payment adoption continues to rise across both consumer and business applications. Increasing integration of instant payment infrastructure and embedded finance solutions within mobile commerce and online retail ecosystems is further accelerating industry growth. The ongoing shift toward cashless transactions and real-time payment processing is creating favorable conditions for third-party payment providers offering seamless, secure, and flexible transaction experiences. Payment service providers are increasingly focusing on multi-rail payment orchestration, tokenization technologies, and intelligent fraud management systems to improve transaction efficiency and user convenience. The growing popularity of real-time transfers, digital wallets, and account-to-account payment methods is also reshaping transaction ecosystems worldwide. Continuous advancements in payment infrastructure and strong institutional support for digital financial systems are contributing to long-term market expansion across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $182.1 Billion |

| Forecast Value | $421.4 Billion |

| CAGR | 8.8% |

Several structural developments are strengthening value creation across the third party payment industry. Instant payment systems are witnessing significant gains in adoption compared to traditional transaction methods, while conventional payment channels continue to lose market share across multiple regions. This shift is encouraging greater consolidation of payment activities onto real-time processing platforms and digital wallet ecosystems supported by widespread merchant acceptance and user familiarity. As a result, providers capable of supporting multi-rail payment routing, secure tokenization, and risk-based transaction authorization across cards, digital wallets, and account-to-account transfers are benefiting from stronger operational efficiency and improved profitability. National fast payment systems operating with continuous settlement capabilities are also enabling wider adoption of unified payment infrastructures for retail and peer-to-peer transactions.

The online payments segment held a 45.2% share, generating USD 82.3 billion in 2025. The segment continues to experience rapid growth as businesses increasingly prioritize frictionless checkout experiences, tokenized transactions, and multi-currency settlement capabilities. Expanding e-commerce activity and growing consumer preference for digital transactions are further supporting demand for online payment solutions worldwide.

The digital wallets segment captured 50.1% share in 2025. Digital wallets are becoming the preferred payment method among consumers in regions actively promoting cashless transactions and digital financial services. Their convenience, accessibility, and integration with mobile devices continue to accelerate adoption across both online and offline payment environments.

U.S. Third Party Payment Market generated USD 50.4 billion in 2025 and is projected to grow at a CAGR of 8.2% between 2026 and 2035. The United States remains one of the largest markets globally due to its advanced digital infrastructure, widespread card usage, and increasing adoption of mobile wallets and instant payment technologies. Businesses across retail, healthcare, hospitality, and e-commerce sectors are increasingly implementing third-party payment platforms to improve transaction speed, reduce checkout friction, and support omnichannel payment experiences.

Leading companies operating in the Global Third Party Payment Market include Adyen, Ant, Block, Checkout, CyberSource (Visa), FIS (Worldpay), Global Payments, PayPal, Stripe, and Tencent (WeChat Pay). Companies operating in the third party payment market are implementing several strategic initiatives to strengthen their market presence and expand customer reach. Leading firms are investing heavily in advanced payment technologies, including AI-powered fraud detection, real-time transaction processing, and tokenization systems to improve security and operational efficiency. Strategic partnerships with banks, merchants, fintech firms, and e-commerce platforms are helping providers broaden service capabilities and expand global acceptance networks. Businesses are also focusing on integrating multi-currency settlement options, embedded finance services, and seamless mobile wallet functionality to improve customer convenience. In addition, companies are enhancing cloud-based payment infrastructure and omnichannel payment solutions to support evolving digital commerce requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Payment

- 2.2.3 Payment Method

- 2.2.4 End Use

- 2.2.5 Industry Vertical

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Growth of E-Commerce and Online Retail

- 3.2.1.2 Increasing Smartphone and Mobile Wallet Adoption

- 3.2.1.3 Government Push for Digital Payments and Financial Inclusion

- 3.2.1.4 Shift Toward Cashless Economies and Digital Transactions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Dependence on Banking and Card Network Infrastructure

- 3.2.2.2 Cybersecurity Risks and Fraud Exposure

- 3.2.3 Market opportunities

- 3.2.3.1 Development of Value-Added Services

- 3.2.3.2 Integration of AI for Fraud Detection and Risk Management

- 3.2.3.3 Rising Demand for Cross-Border Payment Solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 Card Networks (Visa/Mastercard processing rails)

- 3.4.1.2 Payment Gateways (e.g., API-based checkout infrastructure)

- 3.4.1.3 Digital Wallet Platforms

- 3.4.2 Emerging technologies

- 3.4.2.1 Real-Time Payment (RTP) Networks

- 3.4.2.2 Open Banking APIs

- 3.4.2.3 AI-Powered Fraud Detection and Risk Scoring Systems

- 3.4.1 Current technological trends

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - Federal Reserve System

- 3.5.1.2 US- Consumer Financial Protection Bureau

- 3.5.1.3 Canada - FINTRAC

- 3.5.2 Europe

- 3.5.2.1 Germany - European Central Bank (ECB)

- 3.5.2.2 UK - Financial Conduct Authority (FCA)

- 3.5.3 Asia Pacific

- 3.5.3.1 India - Reserve Bank of India (RBI)

- 3.5.3.2 China - People's Bank of China

- 3.5.4 Latin America

- 3.5.4.1 Brazil - Banco Central do Brasil (BCB)

- 3.5.4.2 Mexico - Comision Nacional Bancaria y de Valores (CNBV)

- 3.5.5 MEA

- 3.5.5.1 Saudi Arabia - Saudi Central Bank (SAMA)

- 3.5.5.2 South Africa - South African Reserve Bank (SARB)

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Cybersecurity & Functional Safety Analysis

- 3.9.1 Threat Landscape & Attack Vector Analysis

- 3.9.2 Security Standards & Certification Requirements

- 3.9.3 Incident Response & Recovery Protocols

- 3.9.4 Emerging Cyber Threats (Ransomware, DDoS, Phishing)

- 3.10 Fraud Prevention, Risk Management & Chargeback Systems

- 3.10.1 Fraud Detection Technologies (ML, AI, Behavioral Analytics)

- 3.10.2 Real-Time Transaction Monitoring Systems

- 3.10.3 Chargeback Management & Dispute Resolution Processes

- 3.10.4 Identity Verification & Authentication Protocols

- 3.10.5 Fraud Loss Trends & Financial Impact

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Payment, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Online Payments

- 5.3 POS Payments

- 5.4 Peer-to-Peer Payments

Chapter 6 Market Estimates and Forecast, By Payment Method, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Credit & Debit Cards

- 6.3 Net Banking

- 6.4 Digital Wallets

- 6.5 Mobile Payments

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Consumer Payments

- 7.3 Business Payments

- 7.3.1 SMEs

- 7.3.2 Large Enterprises

Chapter 8 Market Estimates and Forecast, By Industry Vertical, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Retail

- 8.3 Hospitality

- 8.4 E-commerce

- 8.5 Healthcare

- 8.6 BFSI

- 8.7 Government

- 8.8 Travel

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Sweden

- 9.3.8 Switzerland

- 9.3.9 Poland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.4.7 Indonesia

- 9.4.8 Thailand

- 9.4.9 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Chile

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 PayPal

- 10.1.2 Stripe

- 10.1.3 Adyen

- 10.1.4 Block

- 10.1.5 FIS (Worldpay)

- 10.1.6 Checkout

- 10.1.7 Nuvei

- 10.1.8 Paysafe

- 10.1.9 Global Payments

- 10.1.10 Ant Group

- 10.1.11 Shift4 Payments

- 10.1.12 CyberSource (Visa)

- 10.2 Regional players

- 10.2.1 Tencent (WeChat Pay)

- 10.2.2 One97 Communications

- 10.2.3 Razorpay

- 10.2.4 Klarna Bank

- 10.2.5 Mollie

- 10.2.6 Mercado Pago

- 10.3 Emerging players

- 10.3.1 Airwallex

- 10.3.2 Rapyd