PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045778

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045778

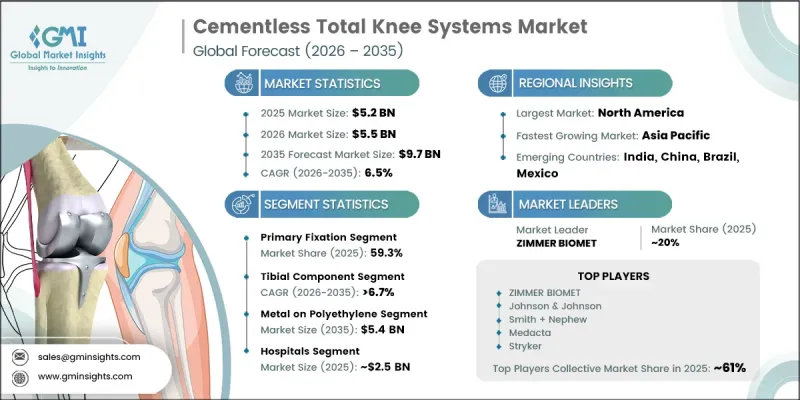

Cementless Total Knee Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Cementless Total Knee Systems Market was valued at USD 5.2 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 9.7 billion by 2035.

The market growth is supported by the rising incidence of degenerative joint disorders, increasing demand for advanced orthopedic procedures, and growing adoption of minimally invasive surgical approaches worldwide. Cementless total knee systems are designed to achieve implant fixation without the use of bone cement, instead relying on biological integration between the implant and surrounding bone structures. These systems use specialized porous coatings and surface technologies that encourage natural bone growth and long-term implant stability. Compared to conventional fixation methods, cementless systems are increasingly preferred due to their ability to improve implant longevity, reduce loosening risks, and support enhanced patient mobility over time. In addition, the rapidly expanding elderly population and rising number of patients requiring joint reconstruction procedures are contributing significantly to market demand. Healthcare providers are also increasingly focusing on long-term treatment sustainability and reducing revision surgery rates, further accelerating the adoption of cementless knee replacement technologies across developed and emerging healthcare markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.2 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 6.5% |

The cementless total knee systems industry is witnessing increasing technological advancements aimed at improving implant precision, surgical outcomes, and patient recovery experiences. Manufacturers are concentrating on advanced implant materials, enhanced porous structures, and surface engineering technologies that support faster osseointegration and improved biomechanical performance. Growing awareness among orthopedic surgeons regarding the long-term clinical benefits of cementless fixation is also strengthening market penetration. In addition, the integration of robotic-assisted surgical systems and digital planning technologies is improving procedural accuracy and implant positioning, contributing to higher success rates in knee replacement procedures. Expanding healthcare infrastructure, improved patient access to orthopedic treatments, and rising healthcare expenditure are further supporting the growth of the cementless total knee systems market.

The primary fixation segment accounted for a 59.3% share in 2025. The segment continues to dominate due to its ability to provide strong immediate implant stability, reliable biological fixation, and long-term implant durability in primary knee arthroplasty procedures. Advanced press-fit implant designs and highly engineered biologic fixation surfaces are increasing surgeon confidence in cementless technologies, particularly in patients requiring durable and long-lasting joint replacement solutions. Demand for primary fixation systems is also rising among younger and physically active patient groups seeking improved implant performance and reduced likelihood of future revision procedures. Continuous improvements in porous metal technologies and long-term osseointegration outcomes are further supporting segment growth and strengthening its position across orthopedic healthcare facilities worldwide.

The femoral component segment is anticipated to grow at a CAGR of 6.2% and is projected to reach USD 3.6 billion by 2035. Growth within the segment is driven by ongoing advancements in implant contouring, enhanced surface coating technologies, and improved compatibility with cementless fixation systems. Manufacturers are increasingly focusing on optimizing biomechanical alignment, wear resistance, and implant performance to support better long-term clinical outcomes. The segment is also benefiting from the development of integrated implant systems designed to improve joint movement, balanced kinematics, and implant survivorship. Increasing emphasis on personalized orthopedic solutions and improved anatomical fit is further contributing to the rising demand for advanced femoral component technologies within cementless total knee replacement procedures.

North America Cementless Total Knee Systems Market accounted for 39.2% share in 2025 and is expected to record substantial growth throughout the forecast period. The region remains a major market for cementless orthopedic implants due to high surgical procedure volumes, advanced healthcare infrastructure, and early adoption of biologic fixation technologies. Strong demand is supported by the growing patient population affected by arthritis and other degenerative joint conditions, along with increasing preference among surgeons for cementless implants in younger and active individuals. Favorable reimbursement policies, widespread adoption of robotic-assisted orthopedic procedures, and continuous product innovation by leading medical device manufacturers are further reinforcing market expansion across North America. In addition, growing investments in orthopedic research and technological development continue to strengthen the region's leadership position within the global cementless total knee systems industry.

Key companies operating in the Global Cementless Total Knee Systems Market include AESCULAP, CONFORMIS, Corin, Enovis, EPISURF, Exactech, Johnson & Johnson, LINK, Medacta, MicroPort Orthopedics, Smith + Nephew, Stryker, Symbios, UNITED ORTHOPEDIC, and Zimmer Biomet. Companies operating in the cementless total knee systems market are adopting several strategic initiatives to strengthen their competitive positioning and expand global market presence. Leading manufacturers are investing heavily in research and development activities focused on advanced implant materials, porous coating technologies, and robotic-assisted surgical systems to improve implant performance and patient outcomes. Strategic collaborations with hospitals, orthopedic centers, and healthcare providers are also helping companies increase product adoption and strengthen clinical relationships. Many market participants are expanding manufacturing capabilities and geographic distribution networks to improve accessibility across emerging and developed healthcare markets. In addition, businesses are prioritizing product portfolio diversification and personalized implant solutions tailored to patient-specific anatomical requirements. Continuous investments in surgeon training programs, digital surgical planning technologies, and long-term clinical studies are further supporting brand credibility and strengthening market foothold across the global orthopedic industry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Fixation method trends

- 2.2.3 Component trends

- 2.2.4 Material trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of osteoarthritis and rheumatoid arthritis globally

- 3.2.1.2 Increasing adoption of minimally invasive surgical techniques

- 3.2.1.3 Technological advancements in cementless fixation methods

- 3.2.1.4 Growing geriatric population prone to joint disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with cementless knee systems

- 3.2.2.2 Limited skilled orthopedic surgeons for specialized procedures

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of robotic-assisted and digital surgery platforms

- 3.2.3.2 Expansion in emerging healthcare markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pricing trend analysis

- 3.6 Technology and innovation landscape (Driven by Primary Research)

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Future market trends (Driven by Primary Research)

- 3.8 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by Primary Research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Fixation Method, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Primary fixation

- 5.3 Hybrid fixation

Chapter 6 Market Estimates and Forecast, By Component, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Tibial component

- 6.3 Femoral component

Chapter 7 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Metal-on-polyethylene

- 7.3 Ceramic-on-polyethylene

- 7.4 Other materials

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Orthopedic centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AESCULAP

- 10.2 CONFORMIS

- 10.3 Corin

- 10.4 Johnson & Johnson

- 10.5 enovis

- 10.6 EPISURF

- 10.7 exactech

- 10.8 LINK

- 10.9 Medacta

- 10.10 MicroPort Orthopedics

- 10.11 Smith + Nephew

- 10.12 stryker

- 10.13 symbios

- 10.14 UNITED ORTHOPEDIC

- 10.15 ZIMMER BIOMET