PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045779

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045779

Class 7 Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

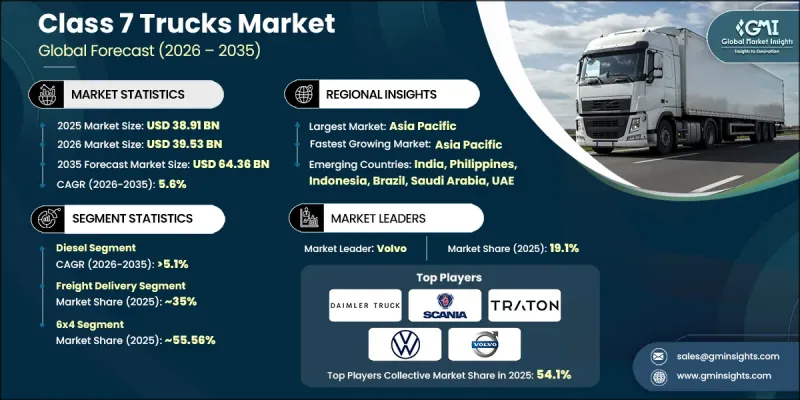

The Global Class 7 Trucks Market was valued at USD 38.91 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 64.36 billion by 2035.

The market is undergoing structural transformation as freight logistics, infrastructure development, and industrial operations evolve toward more optimized and technology-enabled fleet ecosystems. Class 7 trucks, typically defined by a GVWR range of 26,001 to 33,000 lbs, are increasingly positioned as essential assets in medium-duty transportation networks supporting distribution activities, construction-related operations, municipal functions, and utility-based services. Fleet operators are rapidly adopting telematics solutions, advanced driver-assistance systems, and alternative fuel technologies, which are reshaping fleet efficiency, route optimization, and lifecycle cost management strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $38.91 Billion |

| Forecast Value | $64.36 Billion |

| CAGR | 5.6% |

Regulatory pressure is playing a defining role in shaping market direction, with stringent emission standards, zero-emission freight mandates, and sustainability-focused transport policies influencing purchasing behavior across major economies. Regions such as North America and Europe are accelerating fleet renewal cycles due to compliance requirements, while emerging economies are progressively tightening emission frameworks, encouraging modernization of medium-duty fleets. These regulatory dynamics are also influencing powertrain selection, infrastructure investments, and long-term procurement planning. In parallel, rising demand from expanding logistics networks and industrial supply chains is reinforcing the need for reliable and adaptable Class 7 trucks, making them central to modern freight mobility strategies across global markets.

The diesel-powered segment held a 77.01% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. Diesel technology continues to lead the Class 7 trucks space due to its high torque output, fuel efficiency, and strong suitability for long-distance and heavy-load operations. These trucks are widely preferred in sectors requiring durability and consistent performance under demanding conditions, including logistics, infrastructure development, municipal operations, and regional distribution activities. Established fueling infrastructure and widespread diesel availability further reinforce its strong adoption across both developed and developing regions, ensuring continued market stability for diesel-powered medium-duty trucks.

The utility services application segment is expected to grow at a CAGR of 6.4% through 2035, supported by increasing deployment of Class 7 trucks across public infrastructure maintenance, waste handling systems, energy distribution networks, and municipal operations. Governments and private operators are actively modernizing utility fleets to enhance efficiency, reduce operational downtime, and comply with tightening environmental standards. Fleet upgrades are also being driven by the adoption of alternative fuel systems, integrated telematics platforms, and enhanced safety technologies, which are improving operational performance and supporting long-term sustainability goals in utility-based transportation services.

China Class 7 Trucks Market held a 64.2% share in 2025 and generated USD 9.3 billion through 2035. The country's market expansion is strongly supported by large-scale infrastructure investment, rapid growth in urban freight systems, and sustained government initiatives aimed at modernizing commercial vehicle fleets. Ongoing development of industrial zones, smart city projects, and transportation infrastructure is significantly increasing demand for medium-duty trucks across construction support, municipal services, and regional freight movement. Additionally, the rapid expansion of digital commerce and time-sensitive delivery services is strengthening demand for efficient mid-mile logistics solutions, further reinforcing the importance of Class 7 trucks in China's evolving transport ecosystem.

Key players operating in the Global Class 7 Trucks Industry include Volvo, PACCAR, Isuzu Motors, Daimler Trucks, Volkswagen, Traton, Scania, Kenworth, and Peterbilt. Companies in the Class 7 Trucks Market are prioritizing fleet electrification strategies and alternative fuel integration to align with global emission targets and regulatory mandates. They are investing heavily in telematics-based fleet intelligence systems to enhance route optimization, predictive maintenance, and real-time performance tracking. Strategic collaborations with logistics providers and infrastructure developers are strengthening their supply chain presence. Manufacturers are also focusing on modular truck platforms to improve customization flexibility across applications. In addition, continuous R&D investments are being directed toward improving vehicle efficiency, safety systems, and autonomous driving capabilities. Expansion of service networks and lifecycle support programs is further helping companies retain long-term customer relationships and reinforce market competitiveness across diverse regions.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast Model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel

- 2.2.3 Application

- 2.2.4 Axle

- 2.2.5 Horsepower

- 2.2.6 Ownership

- 2.2.7 Transmission

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for electric & hybrid class 7 trucks across the globe

- 3.2.1.2 Growing freight transportation activities across North America

- 3.2.1.3 Implementation of stringent emission regulations in Europe

- 3.2.1.4 Rising investments in infrastructure development activities in Asia Pacific

- 3.2.1.5 Growing demand for class 7 from mining and oil & gas sector in MEA

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial and maintenance costs

- 3.2.2.2 Shortage of truck drivers

- 3.2.3 Market opportunities

- 3.2.3.1 Electrification of municipal and urban logistics fleets

- 3.2.3.2 Expansion of infrastructure and construction activities in emerging economies

- 3.2.3.3 Growth of flexible ownership, leasing, and Truck-as-a-Service (TaaS) models

- 3.2.3.4 Integration of advanced telematics and fleet analytics solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and Innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 NEVI / IIJA, Advanced Clean Trucks (ACT) Regulation.

- 3.6.2 Europe

- 3.6.2.1 Germany: Electric Mobility Act (EmoG)

- 3.6.2.2 UK: Clean Vehicle Retrofit Accreditation Scheme (CVRAS), Ultra-Low Emission Zone (ULEZ)

- 3.6.2.3 France: Mobility Orientation Law (LOM Act)

- 3.6.2.4 Italy: National Integrated Plan for Energy and Climate (PNIEC)

- 3.6.3 Asia Pacific

- 3.6.3.1 China: New Energy Vehicle (NEV) Mandate

- 3.6.3.2 India: FAME II Scheme

- 3.6.3.3 Japan: Strategic Roadmap for EV/FCV Deployment

- 3.6.3.4 Australia: State-Level Zero-Emission Vehicle Mandates

- 3.6.4 Latin America

- 3.6.4.1 Brazil: National Electric Mobility Policy (PNME)

- 3.6.4.2 Mexico: Urban Zero-Emission Fleet Programs

- 3.6.4.3 Argentina: Provincial EV Incentive Regulations (Buenos Aires)

- 3.6.5 MEA

- 3.6.5.1 UAE: EV Charging Infrastructure Regulation (ADDM/DEWA)

- 3.6.5.2 Saudi Arabia: EV Deployment Regulatory Framework (SASO)

- 3.6.5.3 South Africa: Green Transport Strategy

- 3.6.1 North America

- 3.7 Patent Landscape (Driven by Primary Research)

- 3.8 Trade Data Analysis (Based on Paid Database)

- 3.8.1 Import/Export Volume & Value Trends

- 3.8.2 Key Trade Corridors & Tariff Impact

- 3.9 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.9.1 AI-Driven Disruption of Existing Business Models

- 3.9.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.9.3 Risks, Limitations & Regulatory Considerations

- 3.10 Capacity & Production Landscape (Driven by Primary Research)

- 3.10.1 Production Capacity by Region & Key Producer

- 3.10.2 Capacity Utilization Rates & Expansion Pipelines

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favourable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Company market share analysis

- 4.1.1 North America

- 4.1.2 Europe

- 4.1.3 Asia Pacific

- 4.1.4 Latin America

- 4.1.5 MEA

- 4.2 Competitive analysis of major market players

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New Product Launches

- 4.4.4 Expansion Plans and funding

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Natural gas

- 5.4 Hybrid electric

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Freight delivery

- 6.3 Utility services

- 6.4 Construction & mining

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Axle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 4x2

- 7.3 6x4

- 7.4 6x2

Chapter 8 Market Estimates & Forecast, By Horsepower, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Below 300HP

- 8.3 300HP - 400HP

- 8.4 400HP - 500HP

- 8.5 500HP & Above

Chapter 9 Market Estimates & Forecast, By Ownership, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Fleet operator

- 9.3 Independent operator

Chapter 10 Market Estimates & Forecast, By Transmission, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Manual transmission

- 10.3 Automatic transmission

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Daimler Truck

- 12.1.2 Ford Motor Company

- 12.1.3 Hino Motors

- 12.1.4 Isuzu Motors

- 12.1.5 Navistar

- 12.1.6 Scania

- 12.1.7 TRATON

- 12.1.8 Volvo Trucks

- 12.2 Regional Players

- 12.2.1 Ashok Leyland

- 12.2.2 BYD

- 12.2.3 Eicher Motor

- 12.2.4 GMC

- 12.2.5 Hyundai

- 12.2.6 JAC Motors

- 12.2.7 Kenworth

- 12.2.8 Kia

- 12.2.9 Mack Trucks

- 12.2.10 Mahindra & Mahindra

- 12.2.11 Mitsubishi Fuso Truck and Bus Corporation

- 12.2.12 Peterbilt

- 12.2.13 SML Isuzu

- 12.2.14 Tata Motors

- 12.3 Emerging Players

- 12.3.1 Dongfeng Motor

- 12.3.2 Rivian Automotive

- 12.3.3 SAIC Maxus