PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045812

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045812

Automotive Ceramics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

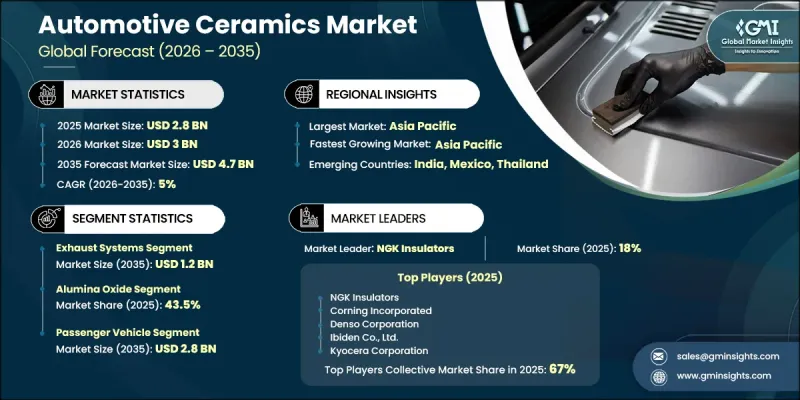

The Global Automotive Ceramics Market was valued at USD 2.8 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 4.7 billion by 2035.

Market growth is driven by increasingly stringent vehicle emission regulations introduced between 2022 and 2025, which have accelerated the adoption of ceramic-based emission control components. Automakers are increasingly relying on durable ceramic substrates manufactured from cordierite and silicon carbide to meet evolving environmental compliance standards while maintaining vehicle efficiency. Demand for advanced ceramic filtration technologies is stable across replacement and original equipment applications despite ongoing shifts in vehicle powertrain technologies. The automotive ceramics industry is also benefiting from rising electrification trends, as ceramic materials are becoming essential in electric and hybrid vehicle systems, including power electronics, battery insulation, and inverter components. Materials such as alumina and aluminum nitride are witnessing growing utilization due to their superior thermal conductivity and electrical insulation capabilities in high-voltage environments. Additionally, automotive manufacturers are increasingly seeking lightweight materials with high thermal shock resistance to improve fuel efficiency, enhance compact vehicle designs, and support performance stability under fluctuating operating temperatures.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 5% |

The exhaust systems segment generated USD 723.4 million in 2025 and is anticipated to reach USD 1.2 billion by 2035, supported by continued advancements in emission control technologies and increasing demand for catalytic converters and particulate filtration systems. The growing focus on reducing vehicle emissions globally is sustaining strong demand for ceramic substrates used in exhaust treatment applications. Automotive manufacturers continue to integrate advanced ceramic materials into exhaust systems to enhance durability, improve filtration efficiency, and comply with tightening environmental standards across global automotive markets.

The alumina oxide segment accounted for 43.5% share in 2025 and is expected to witness strong growth through 2035. Market expansion for this segment is being driven by the material's cost-effectiveness, excellent electrical insulation performance, and broad compatibility with automotive electronic systems and sensor technologies. Alumina oxide ceramics are increasingly utilized across modern vehicle applications due to their ability to withstand high temperatures and provide reliable operational performance in electrically demanding environments. Their widespread use in automotive electronics continues to support segment growth as vehicle technologies become more advanced and electronically integrated.

North America Automotive Ceramics Market reached USD 633.1 million in 2025 and is projected to reach to USD 1.1 billion by 2035, supported by increasing upgrades in vehicle emission control systems and the rapid integration of electrified vehicle technologies. Rising investments in electric and hybrid vehicle manufacturing, along with stricter environmental regulations, are accelerating the demand for advanced ceramic materials across automotive applications. In addition, the growing focus on high-performance thermal management and electrical insulation solutions within next-generation vehicles is further contributing to market expansion across North America.

Leading companies operating in the Global Automotive Ceramics Market include Corning Incorporated, Kyocera Corporation, NGK Insulators, Denso Corporation, Ceramtec GmbH, Coorstek Inc., 3M, Almatis GmbH, Elan Technologies, Ferrotec Corporation, Hoganas AB, and Ibiden Co., Ltd. Companies operating in the automotive ceramics market are focusing on several strategic initiatives to strengthen their market presence and enhance long-term competitiveness. Manufacturers are investing heavily in research and development activities to create advanced ceramic materials with improved thermal resistance, lightweight properties, and higher electrical insulation performance. Many industry participants are also expanding production capabilities to meet increasing demand from electric and hybrid vehicle manufacturers. Strategic collaborations with automotive OEMs and technology providers are helping companies accelerate product innovation and improve integration across next-generation vehicle platforms. In addition, businesses are prioritizing the development of high-efficiency emission control ceramics to comply with tightening global environmental regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Application

- 2.2.3 Material

- 2.2.4 Vehicle Type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Application

- 3.8 Production Capacity, 2025

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Engine Parts

- 5.3 Exhaust Systems

- 5.4 Automotive Electronics

- 5.5 Braking Systems

- 5.6 Others (friction components, heat shields)

Chapter 6 Market Estimates and Forecast, By Material, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Titanate Oxide

- 6.3 Zirconia Oxide

- 6.4 Alumina Oxide

- 6.5 Others (silicon nitride (Si3N4), silicon carbide (SiC))

Chapter 7 Market Estimates and Forecast, By Vehicle Type, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.3 Commercial Vehicle

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Almatis GmbH

- 9.3 Ceramtec GmbH

- 9.4 Coorstek Inc.

- 9.5 Corning Incorporated

- 9.6 Denso Corporation

- 9.7 Elan Technologies

- 9.8 Ferrotec Corporation

- 9.9 Hoganas AB

- 9.10 Ibiden Co., Ltd.

- 9.11 Kyocera Corporation

- 9.12 NGK Insulators