PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045839

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045839

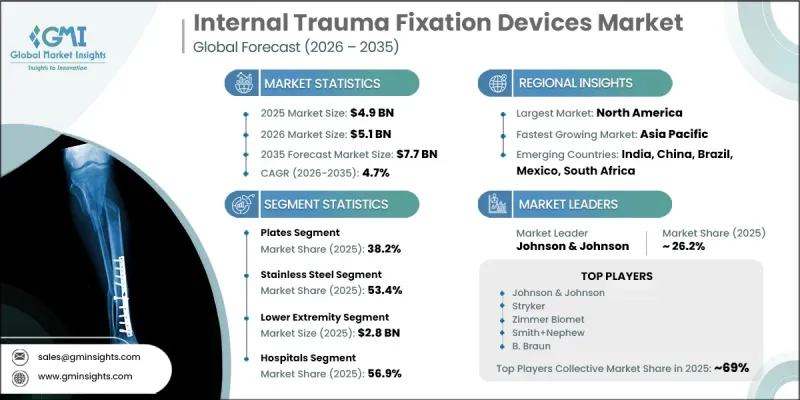

Internal Trauma Fixation Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Internal Trauma Fixation Devices Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 4.7% to reach USD 7.7 billion by 2035.

The market is witnessing expansion driven by a rising number of traumatic injuries, increasing fracture cases, and a growing aging population with higher susceptibility to bone-related conditions such as osteoporosis. Advancements in orthopedic implant technologies are further strengthening market development, particularly through innovations that enhance surgical precision and recovery outcomes. Internal trauma fixation devices are surgically implanted medical tools designed to stabilize fractured or damaged bones, ensuring proper alignment and supporting the natural healing process. These devices, including plates, screws, rods, and nails, are widely used to restore anatomical structure and functional mobility. The increasing incidence of road accidents, sports injuries, occupational hazards, and fall-related fractures is significantly contributing to market growth. Rapid urbanization and increasing vehicle usage in developing economies are further intensifying trauma cases, thereby driving surgical intervention demand. In addition, improved access to orthopedic care services across both developed and emerging healthcare systems is supporting wider adoption. Continuous technological progress, including anatomically shaped implants, bioresorbable fixation systems, and advanced biomaterials such as titanium alloys and PEEK, is enhancing clinical efficiency and patient recovery outcomes, thereby accelerating market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 4.7% |

The plates segment held a 38.2% share in 2025, driven by its extensive use in managing complex fractures and its strong biomechanical stability. Plates are widely preferred for fractures that require precise anatomical alignment and rigid fixation, particularly in load-bearing bones and joint-adjacent injuries. Continuous improvements in locking plate systems and implant design have further strengthened their clinical effectiveness and adoption across orthopedic procedures.

The stainless steel segment held a 53.4% share and is projected to reach USD 4 billion during 2026-2035. Stainless steel implants continue to be widely utilized due to their cost-effectiveness compared to alternative materials such as titanium and bioresorbable options. Their affordability makes them highly suitable for budget-sensitive healthcare environments. Additionally, long-standing clinical use and strong surgeon familiarity have reinforced confidence in their performance, supporting consistent adoption in both routine and complex fracture treatments.

North America Internal Trauma Fixation Devices Market held a 44.5% share in 2025. The region experiences a high burden of trauma cases resulting from traffic incidents, sports injuries, and workplace accidents, all of which contribute to a strong demand for fixation devices such as screws, plates, and nails. Well-established healthcare infrastructure, along with advanced trauma care facilities, enables rapid surgical response and effective fracture management. Continuous investments in modern orthopedic technologies by hospitals and trauma centers further support regional market growth.

Key companies operating in the Global Internal Trauma Fixation Devices Market include Acumed, Arthrex, B. Braun, CONMED, Globus Medical, Implanet, Inion, Johnson & Johnson, KLS Martin Group, Medartis, Medicon, Orthofix, Smith+Nephew, Stryker, and Zimmer Biomet. Companies operating in the internal trauma fixation devices market are focusing on innovation-led strategies to strengthen their competitive positioning and expand clinical adoption. Leading manufacturers are investing heavily in research and development to introduce advanced fixation systems that enhance surgical precision, reduce recovery time, and improve patient outcomes. Product diversification across plates, screws, rods, and bioresorbable implants is helping companies address a wide range of fracture types and surgical requirements. Strategic collaborations with hospitals, trauma centers, and orthopedic specialists are supporting broader product acceptance and clinical integration. Companies are also expanding manufacturing capabilities and optimizing supply chains to ensure cost efficiency and product availability across global markets.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Material type trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of sports and traumatic injuries

- 3.2.1.2 Growing demand for orthopedic implants

- 3.2.1.3 Technological advancements in implant design and materials

- 3.2.1.4 Rising adoption of minimally invasive surgical techniques

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of implants and surgical procedures

- 3.2.2.2 Risk of post-operative complications and implant failure

- 3.2.3 Market opportunities

- 3.2.3.1 Development of bioresorbable and smart fixation materials

- 3.2.3.2 Customized and patient-specific implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape (Driven by primary research)

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario (Driven by primary research)

- 3.7 Future market trends (Driven by primary research)

- 3.8 Value chain analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Pricing analysis, 2025

- 3.12 Customer insights (Driven by primary research)

- 3.13 Start-up scenarios

- 3.14 Investment & funding analysis (Driven by primary research)

- 3.15 Impact of AI & Generative AI on the market (Driven by primary research)

- 3.16 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Plates

- 5.3 Nails

- 5.4 Screws

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Titanium alloy

- 6.4 Bioabsorbable

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Lower extremity

- 7.2.1 Foot & ankle

- 7.2.2 Knee

- 7.2.3 Lower leg

- 7.2.4 Hip and pelvic

- 7.2.5 Spine

- 7.2.6 Thigh

- 7.3 Upper extremity

- 7.3.1 Arm

- 7.3.2 Hand & wrist

- 7.3.3 Shoulder

- 7.3.4 Elbow

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Orthopedic clinics

- 8.4 Ambulatory surgical centers

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Acumed

- 10.2 Arthrex

- 10.3 B. Braun

- 10.4 CONMED

- 10.5 Globus Medical

- 10.6 Implanet

- 10.7 Inion

- 10.8 Johnson & Johnson

- 10.9 KLS Martin Group

- 10.10 Medartis

- 10.11 Medicon

- 10.12 Orthofix

- 10.13 Smith+Nephew

- 10.14 Stryker

- 10.15 Zimmer Biomet