PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045871

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045871

Polyol Sweeteners Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

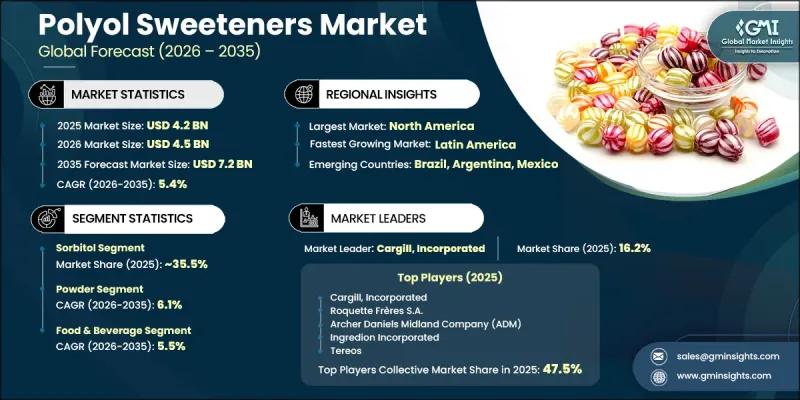

The Global Polyol Sweeteners Market was valued at USD 4.2 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 7.2 billion by 2035.

The industry is gaining consistent traction as consumers increasingly shift toward low-calorie alternatives to traditional sugar, driven by rising health awareness and dietary preferences. Polyol sweeteners play a vital role across food and beverage, personal care, pharmaceutical, and industrial applications due to their multifunctional properties. Their ability to support weight management, blood sugar control, and dental health has strengthened their position in modern product formulations. Growing demand for clean-label and naturally derived ingredients is further accelerating adoption, supported by evolving consumer expectations and regulatory focus on healthier consumption patterns. Rapid urbanization and changing dietary habits have increased the intake of processed foods, where polyols serve as key ingredients in reduced-calorie formulations. Their functional benefits, including moisture retention, product stability, and extended shelf life, make them highly suitable for a wide range of applications. Continuous innovation in formulation technologies and product development is enabling manufacturers to deliver tailored nutrition solutions, further supporting market expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.2 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 5.4% |

The sorbitol segment accounted for 35.5% share in 2025 and is anticipated to grow at a CAGR of 5.6% through 2035. Its widespread use across multiple industries is driven by its versatility, as it provides moderate sweetness while also functioning as a stabilizing and moisture-retaining agent, making it suitable for diverse product formulations.

The powder segment held a share of 62% in 2025 and is expected to grow at a CAGR of 6.1% from 2026 to 2035. Powdered forms are preferred due to their ease of storage, efficient handling, and compatibility with automated production systems. Advancements in processing technologies have further enhanced product consistency and quality, supporting the segment's continued growth and broad adoption across applications.

North America Polyol Sweeteners Market accounted for a 40.5% share in 2025, supported by strong consumer awareness regarding health and wellness and increasing demand for reduced-sugar products. The region benefits from well-established food and beverage industries and continuous innovation by major manufacturers. Growing interest in functional foods and clean-label products is further contributing to market growth across the region.

Key companies operating in the Global Polyol Sweeteners Market include Cargill, Incorporated, Archer Daniels Midland Company (ADM), Ingredion Incorporated, Roquette Freres S.A., Sudzucker AG, Tereos, Associated British Foods, Jungbunzlauer Suisse AG, Gulshan Polyols Limited, Futaste Pharmaceutical Co., Ltd., Huakang Pharma (Zhejiang Huakang Pharmaceutical), B Food Science Co., Ltd., and Batory Foods. Companies in the polyol sweeteners market are focusing on strategic initiatives to strengthen their competitive positioning and expand their global footprint. They are investing in research and development to create advanced formulations that improve taste profiles, functionality, and nutritional value. Strategic partnerships and collaborations are being leveraged to enhance product portfolios and access new markets. Expansion of manufacturing capacities and supply chain optimization are helping companies meet rising demand efficiently. Firms are also emphasizing clean-label and sustainable production practices to align with evolving consumer preferences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sorbitol

- 5.3 Xylitol

- 5.4 Maltitol

- 5.5 Erythritol

- 5.6 Isomalt

- 5.7 Mannitol

- 5.8 Lactitol

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Liquid

- 6.4 Crystal

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.2.1 Bakery & confectionery

- 7.2.2 Beverages

- 7.2.3 Dairy products

- 7.2.4 Processed foods

- 7.3 Pharmaceuticals

- 7.3.1 Chewable tablets

- 7.3.2 Syrups & suspensions

- 7.4 Personal care & cosmetics

- 7.4.1 Oral care (toothpaste, mouthwash)

- 7.4.2 Skincare products

- 7.4.3 Hair care

- 7.5 Industrial applications

- 7.5.1 Chemical synthesis

- 7.5.2 Textile industry

- 7.5.3 Paper industry

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company (ADM)

- 9.2 Associated British Foods

- 9.3 B Food Science Co., Ltd.

- 9.4 Batory Foods

- 9.5 Cargill, Incorporated

- 9.6 Futaste Pharmaceutical Co., Ltd.

- 9.7 Gulshan Polyols Limited

- 9.8 Huakang Pharma (Zhejiang Huakang Pharmaceutical)

- 9.9 Ingredion Incorporated

- 9.10 Jungbunzlauer Suisse AG

- 9.11 Roquette Freres S.A.

- 9.12 Sudzucker AG

- 9.13 Tereos