PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061292

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061292

Counter-Drone Swarm Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

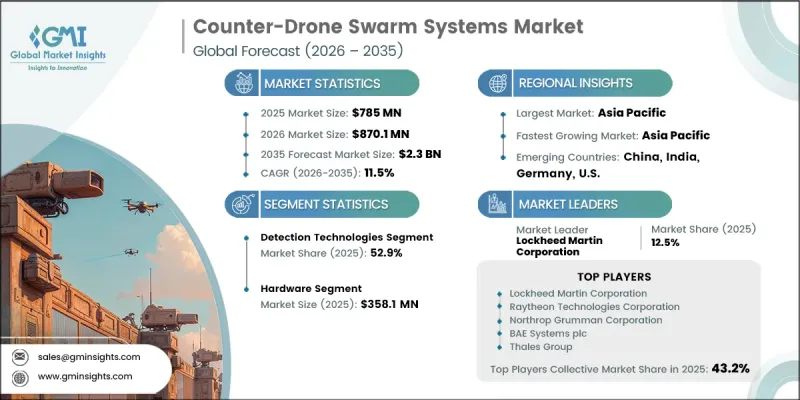

The Global Counter-Drone Swarm Systems Market was valued at USD 785 million in 2025 and is estimated to grow at a CAGR of 11.5% to reach USD 2.3 billion by 2035.

Growth across the global counter-drone swarm systems industry is fueled by the increasing occurrence of sophisticated multi-drone threat environments, rising deployment of low-cost unmanned aerial platforms in asymmetric warfare scenarios, and the growing need to secure strategic infrastructure and high-value assets. Expanding government-backed defense modernization initiatives and rising investments in airspace security technologies are also accelerating market development. In addition, continuous progress in artificial intelligence, electronic warfare systems, sensor fusion technologies, and autonomous threat detection capabilities is significantly improving the operational effectiveness of counter-drone solutions. The market is gaining momentum as defense organizations and security agencies increasingly prioritize scalable systems capable of identifying, tracking, and neutralizing multiple airborne threats simultaneously. Technological advancements are enabling faster response times, enhanced situational awareness, and improved operational reliability, supporting broader deployment across military, homeland security, and critical infrastructure protection applications. These evolving security requirements are transforming counter-drone swarm systems into an essential component of modern defense and surveillance frameworks worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $785 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 11.5% |

The global counter drone swarm systems market is witnessing strong growth due to the increasing use of coordinated unmanned aerial threats designed to challenge conventional air defense systems. Rising investments in next-generation defense programs and increasing government funding aimed at addressing evolving aerial threat environments are further supporting market expansion. Strengthening regulatory frameworks and accelerated procurement activities are contributing to faster deployment of advanced counter-drone technologies across defense and security operations. At the same time, rapid advancements in artificial intelligence, integrated sensing systems, and electronic warfare capabilities are improving the accuracy, scalability, and responsiveness of counter-drone solutions. These developments are positioning counter-drone swarm technologies as a critical element within modern security infrastructure and long-term defense strategies.

The mitigation technologies segment is expected to register a CAGR of 13.1% throughout 2035. Rising demand for active drone neutralization systems capable of addressing increasingly sophisticated and autonomous swarm threats is driving segment growth. Technologies focused on disruption, interception, and airborne threat suppression are witnessing rapid integration across military and security applications. Growing emphasis on strengthening protective capabilities for sensitive infrastructure and strategic facilities is further accelerating adoption within this segment.

The hardware segment accounted for USD 358.1 million in 2025. Market dominance is primarily attributed to large-scale procurement of advanced detection, monitoring, and interception equipment designed to identify and neutralize drone swarm threats. Defense agencies and homeland security organizations continue to prioritize physical defense assets that provide immediate operational response and threat mitigation capabilities. Significant investments associated with system deployment and infrastructure integration are maintaining hardware as the leading revenue-generating segment within the industry.

North America Counter-Drone Swarm Systems Market held a 31.4% share in 2025. Regional market expansion is being driven by rising homeland security concerns, increased focus on safeguarding military facilities and national airspace, and growing awareness regarding unauthorized drone activities. Demand for advanced counter-drone systems is also increasing due to the need to protect critical infrastructure and strategically important facilities from emerging aerial threats. Continuous investments in advanced surveillance and defense technologies are supporting steady deployment of counter-drone swarm solutions across the region.

Major companies operating in the Global Counter-Drone Swarm Systems Market include Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, Thales Group, Leonardo S.p.A., Israel Aerospace Industries (IAI), Elbit Systems Ltd., Saab AB, Rheinmetall AG, L3Harris Technologies, Inc., Anduril Industries, Inc., Dedrone Holdings, Inc., DroneShield Ltd., and Hensoldt AG. Companies active in the counter-drone swarm systems industry are focusing on technological innovation, strategic defense collaborations, and advanced product development to strengthen their market position. Industry participants are investing heavily in artificial intelligence-enabled threat detection, sensor fusion platforms, autonomous interception systems, and next-generation electronic warfare capabilities to improve operational performance and response accuracy. Many organizations are also expanding partnerships with defense agencies, security contractors, and government institutions to accelerate system deployment and broaden their market reach. Continuous investments in research and development are enabling companies to enhance scalability, real-time threat analysis, and integrated airspace security solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Component / offering trends

- 2.2.3 Deployment platform trends

- 2.2.4 End-user trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising threat of coordinated drone swarm attacks

- 3.2.1.2 Escalation of asymmetric and urban warfare

- 3.2.1.3 Protection of critical infrastructure and high-value assets

- 3.2.1.4 Government regulations and defense modernization programs

- 3.2.1.5 Rapid advancements in AI, sensors, and electronic warfare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory constraints and operational authorization limitations

- 3.2.2.2 High system complexity and integration challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into civilian and commercial security applications

- 3.2.3.2 Integration of counter-drone capabilities into broader airspace security platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Detection technologies

- 5.3 Mitigation technologies

Chapter 6 Market Estimates and Forecast, By Component / Offering, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Sensors

- 6.2.2 Effectors - non-kinetic

- 6.2.3 Effectors - kinetic

- 6.2.4 Command & control hardware units

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Deployment Platform, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Ground-based

- 7.2.1 Fixed mount

- 7.2.2 Vehicle mount

- 7.2.3 Portable/handheld

- 7.3 Airborne

- 7.3.1 Manned aircraft

- 7.3.2 UAV-based

- 7.4 Naval

- 7.4.1 Ship-mounted

- 7.4.2 Submarine

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Military & defense

- 8.3 Homeland security & law enforcement

- 8.4 Critical infrastructure operators

- 8.5 Energy & utilities

- 8.6 Oil & gas

- 8.7 Transportation hubs

- 8.8 Airports

- 8.9 Ports

- 8.10 Dams

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Lockheed Martin Corporation

- 10.1.2 Raytheon Technologies Corporation

- 10.1.3 Northrop Grumman Corporation

- 10.1.4 BAE Systems plc

- 10.1.5 Thales Group

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 L3Harris Technologies, Inc.

- 10.2.1.2 Anduril Industries, Inc.

- 10.2.1.3 Dedrone Holdings, Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 DroneShield Ltd.

- 10.2.3 Europe

- 10.2.3.1 Leonardo S.p.A.

- 10.2.3.2 Saab AB

- 10.2.3.3 Rheinmetall AG

- 10.2.3.4 Hensoldt AG

- 10.2.4 Middle East & Africa

- 10.2.4.1 Israel Aerospace Industries (IAI)

- 10.2.4.2 Elbit Systems Ltd.

- 10.2.1 North America