PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061303

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061303

Commercial Earth Observation Satellite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

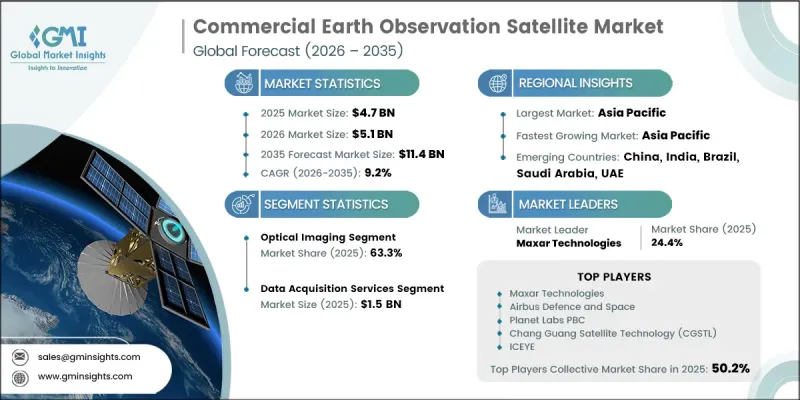

The Global Commercial Earth Observation Satellite Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 11.4 billion by 2035.

The market is witnessing strong growth driven by rising demand for high-precision geospatial intelligence across multiple sectors. Increasing emphasis on environmental monitoring, disaster response, agriculture optimization, and natural resource assessment is significantly supporting market expansion. Improvements in satellite imaging technologies, combined with lower launch costs, are making space-based data more accessible to commercial users. At the same time, advancements in analytics platforms are enhancing the usability and commercial value of satellite-derived insights. Growing reliance on real-time spatial intelligence for decision-making in both public and private sectors is further accelerating adoption. The integration of artificial intelligence and cloud-based processing systems is also transforming data interpretation capabilities, enabling faster insights and more efficient operational planning. Overall, the convergence of technological innovation and expanding application areas continues to strengthen long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.7 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 9.2% |

The optical imaging segment held a 63.3% share in 2025, owing to its extensive use in agriculture, urban development, environmental surveillance, and other large-scale monitoring applications. Optical imaging satellites deliver high-resolution visual data that enables precise interpretation of surface conditions, making them highly valuable for both government and commercial users. Their ability to provide reliable, cost-effective, and detailed imagery supports sustained demand across multiple industries.

The data acquisition services segment reached USD 1.5 billion in 2025, driven by the growing requirement for continuous access to high-resolution satellite imagery. These services play a fundamental role in supplying raw geospatial data used across defense, agriculture, and environmental analysis applications. Their importance in enabling downstream analytics and informed decision-making processes ensures consistent demand and reinforces their central role in the earth observation value chain.

North America Commercial Earth Observation Satellite Market accounted for a 39.8% share in 2025. The region is experiencing strong growth supported by increasing demand from defense and intelligence organizations for high-resolution geospatial intelligence and advanced surveillance capabilities. Expanding integration of satellite-based insights into national security frameworks, infrastructure development, and border monitoring operations is further driving adoption across both government and commercial sectors. In addition, rising investments by major space technology firms and satellite operators are accelerating the deployment of advanced satellite constellations and analytics platforms across the region.

Major companies operating in the Global Commercial Earth Observation Satellite Market include Planet Labs PBC, Maxar Technologies, Airbus Defence and Space, BlackSky Technology, ICEYE, Capella Space, Satellogic, Spire Global, GHGSat, HawkEye 360, Pixxel, Chang Guang Satellite Technology (CGSTL), Synspective, iQPS (Institute for Q-shu Pioneers of Space), OroraTech, Orbital Insight, and Descartes Labs. Companies operating in the commercial earth observation satellite market are focusing on expanding satellite constellations to improve revisit frequency and data coverage across global regions. They are heavily investing in artificial intelligence and machine learning-based analytics to enhance image processing accuracy and reduce time-to-insight for end users. Strategic partnerships with government agencies, defense organizations, and commercial enterprises are being strengthened to expand application reach and long-term contracts. Many players are also adopting cloud-native platforms to enable scalable data distribution and easier integration with enterprise workflows. Cost optimization through small satellite deployment and shared launch systems is another key strategy for improving commercial viability. Firms are additionally prioritizing the development of high-resolution imaging sensors and advanced radar technologies to improve data quality.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Service type trends

- 2.2.3 Orbit type trends

- 2.2.4 End-User trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for real-time geospatial intelligence

- 3.2.1.2 Increasing climate monitoring and disaster management requirements

- 3.2.1.3 Expansion of precision agriculture and natural resource monitoring

- 3.2.1.4 Declining satellite launch costs and growth of small satellite constellations

- 3.2.1.5 Integration of AI and cloud based geospatial analytics platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High data processing and analysis complexity

- 3.2.2.2 Regulatory restrictions and data privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into insurance, financial services, and risk analytics

- 3.2.3.2 Development of digital twins and geospatial simulation platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Optical imaging

- 5.2.1 Panchromatic

- 5.2.2 Multispectral

- 5.2.3 Hyperspectral

- 5.3 Synthetic aperture radar (SAR)

- 5.4 Other sensing technologies

Chapter 6 Market Estimates and Forecast, By Service Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Data acquisition services

- 6.3 Data processing services

- 6.4 Standardized data products

- 6.5 Analytics & insights services

Chapter 7 Market Estimates and Forecast, By Orbit Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Low earth orbit (LEO)

- 7.3 Medium earth orbit (MEO)

- 7.4 Geostationary earth orbit (GEO)

Chapter 8 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Government & defense

- 8.2.1 Defense, intelligence & national security agencies

- 8.2.2 Civil government agencies

- 8.3 Commercial enterprises

- 8.3.1 Insurance & reinsurance

- 8.3.2 Agriculture & food companies

- 8.3.3 Energy & utilities

- 8.3.4 Real estate & construction

- 8.3.5 Logistics, transportation & maritime operations

- 8.3.6 Financial services

- 8.4 Research & academia

- 8.5 NGOs & multilateral organizations

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Maxar Technologies

- 10.1.2 Airbus Defence and Space

- 10.1.3 Planet Labs PBC

- 10.1.4 Chang Guang Satellite Technology (CGSTL)

- 10.1.5 ICEYE

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 BlackSky Technology

- 10.2.1.2 Capella Space

- 10.2.1.3 Spire Global

- 10.2.1.4 HawkEye 360

- 10.2.1.5 Orbital Insight

- 10.2.1.6 Descartes Labs

- 10.2.2 Asia Pacific

- 10.2.2.1 Pixxel

- 10.2.2.2 Synspective

- 10.2.2.3 Institute for Q-shu Pioneers of Space (iQPS)

- 10.2.3 Europe

- 10.2.3.1 GHGSat

- 10.2.3.2 OroraTech

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Satellogic