PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061308

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061308

North America Preschool Toys Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

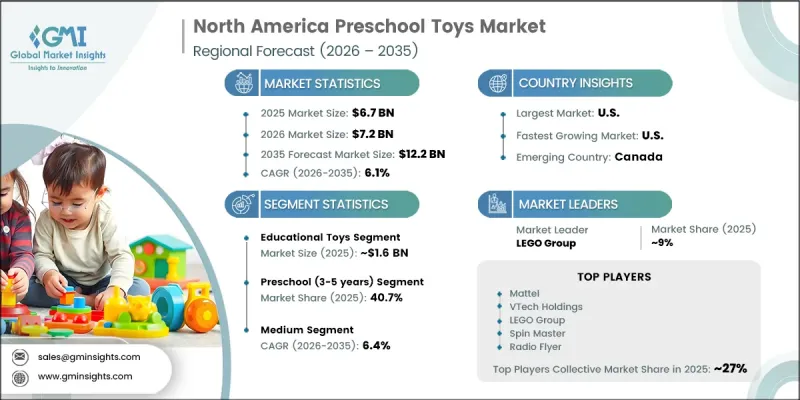

North America Preschool Toys Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 12.2 billion by 2035.

The preschool toys industry across North America continues to experience strong momentum as purchasing patterns evolve and demand rises for products that support early learning and child development. Parents and caregivers increasingly prefer toys that support intellectual growth, emotional development, creativity, communication, and physical coordination, prompting manufacturers to introduce more engaging, development-focused products. Rising consumer awareness of early education, combined with higher disposable incomes and expanding retail accessibility, continues to support market growth across the region. Sustainability remains a major focus area for toy manufacturers as companies adopt environmentally responsible production practices and safer raw materials to align with changing consumer expectations and regulatory standards. In addition, technological advancements are reshaping the preschool toy landscape through the incorporation of smart and interactive features that enhance play experiences. Digital integration and connected play solutions are becoming more prominent as manufacturers focus on creating immersive and learning-oriented products that appeal to modern consumers while strengthening product differentiation in the competitive North America preschool toys market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 6.1% |

The educational toys segment generated USD 1.6 billion in 2025 and is anticipated to witness a CAGR of 6.5% from 2026 to 2035. Educational toys continue to lead the North America preschool toys market as parents, schools, and childcare providers place greater emphasis on developmental learning during early childhood years. Demand remains particularly strong for products designed to encourage language development, analytical thinking, creativity, communication, and foundational academic skills among young children. Increasing recognition of the long-term value associated with learning-based play has accelerated consumer preference toward educational toy categories, strengthening their position within the overall market. This transition in buying behavior has significantly shifted attention away from conventional entertainment-oriented toys, making educational products a primary revenue contributor across the industry.

The preschool age category covering children between 3 and 5 years accounted for 40.7% share in 2025. This segment continues to dominate due to the rapid cognitive, behavioral, and emotional development observed during these formative years. Children within this age bracket demonstrate stronger interest in guided play experiences and activity-driven toys that encourage imagination, learning, communication, and social interaction. The growing preference for products that support developmental milestones and interactive engagement continues to drive consistent demand across several toy categories aimed at preschool-aged children.

United States Preschool Toys Market captured USD 5 billion in 2025. Strong household spending capacity, growing awareness surrounding child development, and a highly established retail infrastructure continue to support the country's dominant market position. Consumers across the U.S. increasingly prioritize toys that combine entertainment with educational value, creating sustained demand for premium and mid-priced offerings. The presence of globally recognized toy manufacturers, expanding online retail channels, and continuous product development activities further strengthen market expansion throughout the country. Strong distribution capabilities and ongoing innovation within the preschool toy sector also contribute to the continued leadership of the United States market.

Key companies operating in the North America Preschool Toys Market include LEGO Group, Mattel, Hasbro, VTech Holdings, Spin Master, MGA Entertainment, Tomy Company, Little Tikes, Step2 Company, Jakks Pacific, Radio Flyer, Crayola, Ravensburger Group, Chicco, PlanToys, Hape International, Green Toys, Plus-Plus, Learning Resources, Edushape, and B. toys. Companies operating in the North America preschool toys market are implementing several strategic initiatives to strengthen their market position and expand consumer reach. Leading manufacturers are increasing investments in product innovation by developing toys that combine educational value with interactive and technology-enabled features. Many companies are also focusing on sustainable manufacturing practices through the use of environmentally friendly materials and safer production standards to align with shifting consumer preferences. Strategic collaborations with retailers, educational institutions, and entertainment brands are helping companies improve brand visibility and market penetration. In addition, businesses are expanding their e-commerce presence and digital marketing capabilities to reach a broader customer base and improve direct-to-consumer sales.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Market estimates & forecasts parameters

- 1.4 Forecast Model

- 1.4.1 Key trends for market estimates

- 1.4.2 Quantified market impact analysis

- 1.4.2.1 Mathematical impact of growth parameters on forecast

- 1.4.3 Scenario analysis framework

- 1.5 Primary research and validation

- 1.5.1 Some of the primary sources (but not limited to)

- 1.6 Data mining sources

- 1.6.1 Paid Sources

- 1.7 Primary research and validation

- 1.7.1 Primary sources

- 1.8 Research Trail & confidence scoring

- 1.8.1 Research trail components

- 1.8.2 Scoring components

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market Definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Age group

- 2.2.4 Price

- 2.2.5 Material

- 2.2.6 End use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component suppliers & raw materials

- 3.1.2 Raw Material Suppliers

- 3.1.3 Toy Manufacturers

- 3.1.4 Distributors & Wholesalers

- 3.1.5 Retail Channels

- 3.1.6 End Users

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing emphasis on early childhood education & cognitive development

- 3.2.1.2 High disposable income and premium toy adoption

- 3.2.1.3 Advanced retail and e-commerce infrastructure

- 3.2.2 Pitfalls & challenges

- 3.2.2.1 Stringent safety regulations & compliance costs

- 3.2.2.2 Market saturation and high competition

- 3.2.3 Opportunities

- 3.2.3.1 Eco-friendly & sustainable toy innovation

- 3.2.3.2 Personalization & customization trends

- 3.2.1 Growth drivers

- 3.3 Technology and Innovation landscape

- 3.3.1 Smart & connected toys

- 3.3.2 STEM & educational technology integration

- 3.3.3 Sustainable material innovations

- 3.3.4 AR/VR in preschool play

- 3.4 Price trends (driven by primary research)

- 3.4.1 By country

- 3.4.2 By product type

- 3.4.3 Historical price trend analysis

- 3.4.4 Pricing strategy by player type

- 3.5 Future market trends

- 3.6 Growth potential analysis

- 3.7 Regulatory framework

- 3.7.1 U.S. toy safety standards

- 3.8 Trade statistics (driven by paid database) (HS Code- 9503)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.8.3 Regional trade balance analysis

- 3.9 Supply chain analysis

- 3.9.1 Global sourcing dynamics

- 3.9.2 Manufacturing hubs

- 3.9.3 Material sourcing challenges

- 3.9.4 Logistics & distribution networks

- 3.9.5 Sustainability & ethical sourcing initiatives

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-Driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

- 3.13 Consumer buying behavior analysis

- 3.13.1 Demographic trends

- 3.13.2 Factors affecting buying decisions

- 3.13.3 Consumer product adoption

- 3.13.4 Preferred distribution channel

- 3.13.5 Preferred price range

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By Country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Educational toys

- 5.2.1 STEM/STEAM toys

- 5.2.2 Puzzles

- 5.2.3 Alphabet & number toys

- 5.2.4 Learning tablets & electronic learning aids

- 5.3 Building & construction toys

- 5.3.1 Building blocks

- 5.3.2 Interlocking bricks

- 5.3.3 Stacking toys

- 5.3.4 Magnetic building sets

- 5.4 Doll & action figures

- 5.4.1 Fashion dolls

- 5.4.2 Character dolls

- 5.4.3 Baby dolls

- 5.4.4 Miniature figures

- 5.5 Vehicles & transportation toys

- 5.5.1 Cars & trucks

- 5.5.2 Trains & railway sets

- 5.5.3 Ride-on toys

- 5.5.4 Remote-controlled vehicles

- 5.6 Art & creative play toys

- 5.6.1 Art supplies

- 5.6.2 Craft kits

- 5.6.3 Modeling clay & dough

- 5.6.4 Drawing & coloring sets

- 5.7 Outdoor & active play toys

- 5.7.1 Sports equipment

- 5.7.2 Playground equipment

- 5.7.3 Water & sand play

- 5.7.4 Balance bikes & scooters

- 5.8 Others (soft toys & plush, musical toys & instruments, etc.)

Chapter 6 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low (Below USD 20)

- 6.3 Medium (Between USD 20-50)

- 6.4 High (More than USD 50)

Chapter 7 Market Estimates & Forecast, By Age Group, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Toddler (1-3 years)

- 7.3 Preschool (3-5 years)

- 7.4 Early childhood (5-7 years)

Chapter 8 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Plastic

- 8.2.1 Traditional plastic

- 8.2.2 Bio-based & recycled plastic

- 8.3 Wooden

- 8.3.1 Solid wood

- 8.3.2 Engineered wood

- 8.3.3 FSC-certified & sustainable wood

- 8.4 Metal

- 8.5 Fabric

- 8.6 Others (rubber, foam, etc.)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Individual

- 9.3 Educational institutions

- 9.3.1 Preschools & daycare centers

- 9.3.2 Kindergartens

- 9.3.3 Early learning centers

- 9.3.4 Special education facilities

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Online

- 10.1.1 E-commerce platforms

- 10.1.2 Company owned websites

- 10.2 Offline

- 10.2.1 Hypermarket/supermarket

- 10.2.2 Departmental stores

- 10.2.3 Specialized stores

- 10.2.4 Franchised outlets

- 10.2.5 Other retail stores

Chapter 11 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 LEGO Group

- 12.1.2 Mattel (Fisher-Price)

- 12.1.3 Hasbro

- 12.1.4 VTech Holdings

- 12.1.5 Spin Master

- 12.1.6 MGA Entertainment

- 12.1.7 Tomy Company

- 12.2 Regional Players

- 12.2.1 Little Tikes

- 12.2.2 Step2 Company

- 12.2.3 Jakks Pacific

- 12.2.4 Radio Flyer

- 12.2.5 Crayola (Hallmark)

- 12.2.6 Ravensburger Group

- 12.2.7 Chicco (Artsana Group)

- 12.3 Emerging Brands

- 12.3.1 PlanToys

- 12.3.2 Hape International

- 12.3.3 Green Toys

- 12.3.4 Plus-Plus

- 12.3.5 Learning Resources

- 12.3.6 Edushape

- 12.3.7 B. toys (Battat)