PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061318

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061318

Edge AI Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

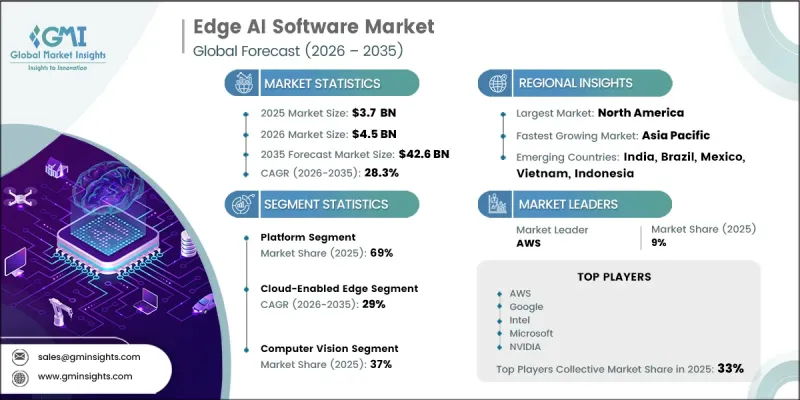

The Global Edge AI Software Market was valued at USD 3.7 billion in 2025 and is estimated to grow at a CAGR of 28.3% to reach USD 42.6 billion by 2035.

The market is experiencing strong momentum due to the increasing integration of artificial intelligence with industrial automation systems. Organizations across multiple industries are deploying edge AI solutions to support real-time decision-making processes, including automated quality inspection, defect identification, predictive maintenance, and intelligent robotics control. The rising emphasis on low-latency processing, enhanced data security, and localized computation is accelerating the adoption of edge-based AI systems across enterprises. In addition, the rapid expansion of IoT ecosystems is generating large volumes of real-time data that require efficient on-device processing, further strengthening market demand. Advancements in generative AI are also contributing to growth, as optimized and compact models are now being deployed on edge infrastructure for real-time text, image, and speech-based applications. Computer vision remains one of the most widely adopted application areas, with extensive usage across manufacturing environments, retail analytics, and security monitoring systems where real-time insights are essential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.7 Billion |

| Forecast Value | $42.6 Billion |

| CAGR | 28.3% |

The platform segment accounted for 69% share in 2025 and is anticipated to grow at a CAGR of 29.3% from 2026 to 2035. Growth in this segment is driven by increasing enterprise preference for integrated platforms that support the complete AI lifecycle, including model development, deployment, monitoring, and governance within a unified environment.

The cloud-enabled edge segment held a 58.8% share in 2025 and is projected to grow at a CAGR of 29% through 2035. This segment is gaining traction due to its ability to support seamless coordination between distributed edge devices and centralized cloud infrastructure, enabling efficient AI model management and scalable deployment across networks.

United States Edge AI Software Market reached USD 1.1 billion in 2025 and is expected to grow at a CAGR of 28.4% between 2026 and 2035. The country leads market development due to strong investments from major technology providers such as Amazon Web Services (AWS), Microsoft, and Google. Enterprises across the United States are increasingly adopting cloud-connected edge platforms across industries including manufacturing, healthcare, defense, and logistics, supporting the deployment of advanced inference systems, orchestration tools, and edge MLOps capabilities.

The Edge AI Software Industry includes several players such as Amazon Web Services (AWS), Alibaba Cloud, Google, IBM, Microsoft, NVIDIA, Intel, Arm, Qualcomm, SAP, Schneider Electric, and Siemens. Companies operating in the edge AI software market are focusing on several strategic initiatives to strengthen their competitive position and expand global reach. A key strategy involves continuous investment in research and development to enhance AI model efficiency, reduce latency, and improve edge deployment capabilities. Organizations are increasingly prioritizing the development of scalable and interoperable platforms that support seamless integration across cloud and edge environments. Strategic partnerships and collaborations with cloud providers, semiconductor manufacturers, and industrial enterprises are also playing a crucial role in accelerating solution deployment and expanding ecosystem capabilities. In addition, companies are focusing on strengthening their edge AI portfolios through acquisitions and technology integrations to gain access to advanced analytics and machine learning capabilities. Expansion of cloud-edge hybrid infrastructures is another major focus area, enabling improved performance and centralized control of distributed systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Deployment mode

- 2.2.4 Technology

- 2.2.5 Data Modality

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of industrial automation and smart manufacturing

- 3.2.1.2 Rising demand for low-latency and privacy-preserving AI

- 3.2.1.3 Expansion of IoT devices and connected sensors

- 3.2.1.4 Emergence of compact generative AI models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Hardware fragmentation and software portability challenges

- 3.2.2.2 Shortage of skilled edge AI developers

- 3.2.3 Market opportunities

- 3.2.3.1 Edge AI MLOps and lifecycle management platforms

- 3.2.3.2 On-device generative AI assistants

- 3.2.3.3 Expansion in healthcare and medical devices

- 3.2.3.4 Growth in emerging markets and smart infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Cost breakdown analysis

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.1.1 National Institute of Standards and Technology

- 3.7.1.2 Innovation, Science and Economic Development Canada

- 3.7.2 Europe

- 3.7.2.1 European Commission

- 3.7.2.2 European Telecommunications Standards Institute

- 3.7.3 Asia Pacific

- 3.7.3.1 Ministry of Industry and Information Technology

- 3.7.3.2 Ministry of Economy, Trade and Industry

- 3.7.4 Latin America

- 3.7.4.1 Ministry of Science, Technology and Innovation

- 3.7.4.2 National Institute of Statistics and Geography

- 3.7.5 Middle East & Africa

- 3.7.5.1 Saudi Data and Artificial Intelligence Authority

- 3.7.5.2 Department of Communications and Digital Technologies

- 3.7.1 North America

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates and Forecast, By Offering, 2022 - 2035 ($ Million)

- 5.1 Key trends

- 5.2 Platform

- 5.3 Frameworks & Toolkits

Chapter 6 Market Estimates and Forecast, By Deployment mode, 2022 - 2035 ($ Million)

- 6.1 Key trends

- 6.2 On-Premises Edge

- 6.3 Cloud-Enabled Edge

Chapter 7 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Million)

- 7.1 Key trends

- 7.2 Generative AI

- 7.3 Machine Learning (ML)

- 7.4 Natural Language Processing (NLP)

- 7.5 Computer Vision

Chapter 8 Market Estimates and Forecast, By Data Modality, 2022 - 2035 ($ Million)

- 8.1 Key trends

- 8.2 Spatial Data

- 8.3 Temporal Data

- 8.4 Visual Data (Video & Image)

- 8.5 Textual Data

- 8.6 Multimodal Data

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Million)

- 9.1 Key trends

- 9.2 Manufacturing & Industrial

- 9.3 Healthcare & Life Sciences

- 9.4 Automotive & Transportation

- 9.5 Retail & Consumer

- 9.6 Smart Cities & Infrastructure

- 9.7 Energy & Utilities

- 9.8 IT & Telecommunications

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Arm

- 11.1.3 Google

- 11.1.4 IBM

- 11.1.5 Intel

- 11.1.6 Microsoft

- 11.1.7 NVIDIA

- 11.1.8 Qualcomm

- 11.2 Regional players

- 11.2.1 Alibaba Cloud

- 11.2.2 AMD

- 11.2.3 MediaTek

- 11.2.4 NXP Semiconductors

- 11.2.5 PTC

- 11.2.6 SAP

- 11.2.7 Schneider Electric

- 11.2.8 Siemens

- 11.3 Emerging players

- 11.3.1 Axelera AI

- 11.3.2 Edge Impulse

- 11.3.3 Hailo

- 11.3.4 SiMa.ai