PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061329

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061329

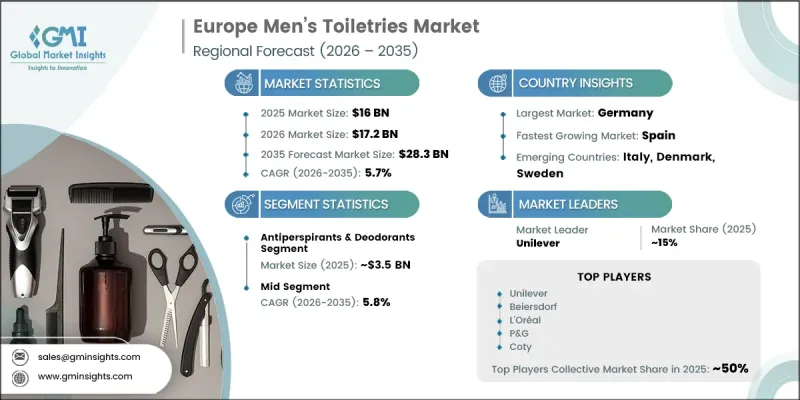

Europe Men's Toiletries Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Europe Men's Toiletries Market was valued at USD 16 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 28.3 billion by 2035.

The market is undergoing a steady transformation as male consumers across Europe increasingly adopt structured skincare, grooming, and personal care routines. Growing acceptance of male grooming, combined with rising awareness of appearance and skin health, is reshaping product demand patterns. Skincare-oriented toiletries are gaining traction as men place greater emphasis on preventive care, anti-aging solutions, and daily maintenance routines. Product categories such as moisturizers, facial creams, sun protection products, and anti-aging formulations are witnessing consistent uptake across multiple age segments. Digital commerce channels are further accelerating adoption by enabling personalized recommendations, discreet purchasing, and subscription-based replenishment models, which collectively increase repeat purchase behavior. Sustainability considerations are also becoming central to buying decisions, supported by evolving European regulatory frameworks that encourage environmentally responsible formulations, reduced packaging waste, and safer ingredient usage. Overall, the market is steadily shifting toward premiumized, wellness-oriented, and digitally enabled grooming solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 5.7% |

The antiperspirants and deodorants segment generated USD 3.5 billion in 2025 and is projected to grow at a CAGR of 5.3% from 2026 to 2035. This category remains a core pillar of the European men's toiletries industry due to its frequent usage and essential role in daily grooming routines. Antiperspirant products primarily target sweat reduction through active ingredients, while deodorants focus on controlling body odor, with many modern formulations combining both functions for enhanced performance. Consumer preference is also shifting toward convenient and sustainable formats, including refillable dispensing solutions that reduce packaging waste and improve usability.

The mid-tier segment accounted for 49.1% share in 2025 and is expected to grow at a CAGR of 5.8% from 2026 to 2035. This segment maintains strong dominance by offering a balanced value proposition between affordability and quality performance, making it highly attractive to mass-market consumers. It includes widely recognized global brands as well as private label offerings distributed through large retail chains. Leading companies such as Beiersdorf AG (NIVEA MEN), Procter & Gamble, Unilever, L'Oreal, Coty Inc, Shiseido, The Estee Lauder Companies, and Edgewell Personal Care continue to strengthen their positions through strong distribution networks, continuous innovation, and sustained brand investment. Mid-range products are designed to deliver dependable performance at competitive pricing, with variations based on product type and packaging scale.

Germany Men's Toiletries Market reached USD 4.1 billion in 2025 and is projected to grow at a CAGR of 5.3% from 2026 to 2035. The country's strong market position is supported by a large consumer base of around 84 million people and high disposable income levels, which encourage consistent spending on personal care and grooming products. Consumer behavior in Germany strongly emphasizes quality, reliability, and product efficacy, contributing to steady demand for both premium and mid-range toiletries. A highly developed retail ecosystem, including major drugstore chains, pharmacies, hypermarkets, and advanced e-commerce platforms, further strengthens product accessibility and market penetration.

Major companies operating in the Europe Men's Toiletries Market include Beiersdorf AG, Procter & Gamble, L'Oreal, Unilever, Edgewell Personal Care, Coty Inc, Shiseido, and The Estee Lauder Companies. Additional regional participants consist of Clarins, Weleda, Bulldog Skincare for Men, The Bluebeards Revenge, Muhle, Taylor of Old Bond Street, and Dr. Harris & Co. Emerging and innovative brands include Harry's, Cornerstone, Hawkins & Brimble, Baxter of California, Muc-Off, and Jack Black. Companies in the Europe men's toiletries market are increasingly focusing on premiumization strategies, product innovation, and sustainability-led formulations to strengthen their competitive position. Many brands are expanding their grooming portfolios with skincare-first product lines that address hydration, anti-aging, and skin protection needs. Digital transformation is a key priority, with firms investing in e-commerce optimization, subscription models, and personalized marketing campaigns to enhance customer engagement. Strategic partnerships with retail chains and pharmacy networks are improving shelf visibility and distribution reach. Companies are also emphasizing eco-friendly packaging, refillable formats, and clean ingredient sourcing to align with sustainability regulations and consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.3 Regional

- 2.4 Product type

- 2.5 Price

- 2.6 Age group

- 2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Male Grooming Consciousness & Social Acceptance

- 3.2.1.2 Urbanization & Rising Disposable Incomes in Emerging Markets

- 3.2.1.3 Growing Demand for Natural, Organic & Clean Label Products

- 3.2.1.4 Sustainability Movement & Zero-Waste Consumer Preferences

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Production Costs for Sustainable & Certified Products

- 3.2.2.2 Performance Gaps in Natural/Aluminum-Free Formulations

- 3.2.2.3 Intense Competition & Brand Differentiation Difficulty

- 3.2.1 Growth drivers

- 3.3 Opportunities

- 3.4 Growth potential analysis

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Impact of AI & Generative AI on the market

- 3.10.1 AI-Driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Consumer behavior analysis

- 3.11.1 Demographic trends

- 3.11.2 Factors affecting buying decision

- 3.11.3 Consumer product adoption

- 3.11.4 Preferred distribution channel

- 3.11.5 Preferred price range

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Bath and shower products

- 5.2.1 Body washes

- 5.2.2 Shower gels

- 5.2.3 Bar soaps

- 5.3 Oral care

- 5.3.1 Toothpaste

- 5.3.2 Toothbrushes

- 5.3.3 Dental floss & mouthwash

- 5.4 Skincare products

- 5.4.1 Moisturizers & face creams

- 5.4.2 Anti-aging products

- 5.4.3 Sun protection

- 5.5 Antiperspirant & deodorants

- 5.5.1 Refillable deodorants

- 5.5.2 Traditional/single-use deodorants

- 5.6 Shaving products

- 5.7 Haircare products

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 High/Premium

- 6.3 Med

- 6.4 Low

Chapter 7 Market Estimates & Forecast, By Age Group, 2022 - 2035, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Below 24 Yrs

- 7.3 25- 35 Yrs

- 7.4 36-45 Yrs

- 7.5 Above 45 Yrs

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Hypermarkets & Supermarkets

- 8.2.2 Pharmacy & Drugstores

- 8.2.3 Convenience stores

- 8.2.4 Others

- 8.3 Online

- 8.3.1 E-commerce websites

- 8.3.2 Company websites

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Netherlands

- 9.2.7 Sweden

- 9.2.8 Switzerland

- 9.2.9 Denmark

- 9.2.10 Rest of Europe

Chapter 10 Company Profiles

- 10.1 Top Global Players

- 10.1.1 Beiersdorf AG

- 10.1.2 Procter & Gamble

- 10.1.3 L'Oreal

- 10.1.4 Unilever

- 10.1.5 Edgewell Personal Care

- 10.1.6 Coty Inc

- 10.1.7 Shiseido

- 10.1.8 The Estee Lauder Companies

- 10.2 Regional Players

- 10.2.1 Clarins

- 10.2.2 Weleda

- 10.2.3 The Bluebeards Revenge

- 10.2.4 Bulldog Skincare for Men

- 10.2.5 Muhle

- 10.2.6 Taylor of Old Bond Street

- 10.2.7 Dr. Harris & Co.

- 10.3 Emerging Players & Innovators

- 10.3.1 Harry's

- 10.3.2 Cornerstone

- 10.3.3 Hawkins & Brimble

- 10.3.4 Baxter of California

- 10.3.5 Muc-Off

- 10.3.6 Jack Black