PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061332

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061332

Aerospace Microcontroller (MCU) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

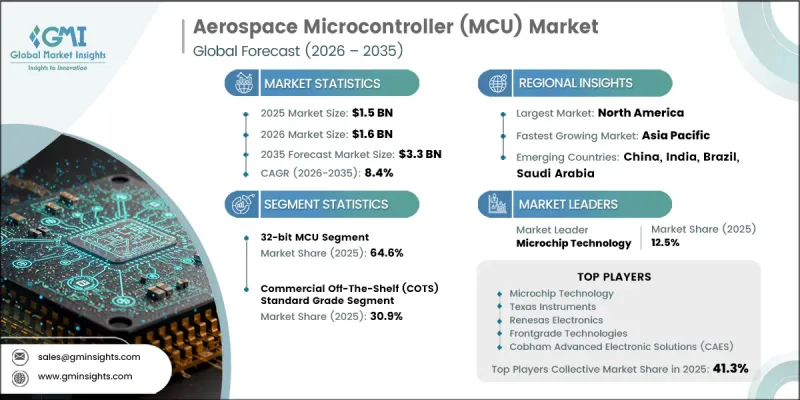

The Global Aerospace Microcontroller Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 3.3 billion by 2035.

Growth across the aerospace microcontroller industry is fueled by rising aircraft manufacturing activity, increasing deployment of satellite constellations, and continuous upgrades of defense avionics systems throughout NATO countries and major Indo-Pacific economies. The market is also benefiting from the growing use of advanced electronic architectures in aerospace systems that require faster processing, higher reliability, and enhanced real-time operational capabilities. Aerospace manufacturers are increasingly integrating microcontroller units into navigation systems, environmental monitoring systems, power management platforms, and flight control technologies, significantly increasing MCU demand per aircraft. In parallel, the industry is adopting AI-enabled aerospace microcontrollers that support onboard data analysis, intelligent fault monitoring, autonomous operational functions, and enhanced sensor processing. Demand for higher computing efficiency is also accelerating the transition toward multicore microcontroller architectures, particularly as avionics systems become more software-driven and data-intensive. These developments continue to position aerospace microcontrollers as a critical component across commercial aviation, defense platforms, satellite electronics, and unmanned aerial systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 8.4% |

The 32-bit MCU segment accounted for 64.6% share in 2025. Its strong market position is supported by widespread adoption across commercial aviation electronics, military embedded systems, and satellite processing applications that require highly reliable real-time computing performance beyond the capabilities of lower-bit architectures. The segment continues to gain momentum due to its combination of advanced processing power, energy efficiency, and broad compatibility with certified software ecosystems, real-time operating environments, and aerospace-grade development frameworks. As aerospace systems become increasingly connected and software-dependent, 32-bit microcontrollers remain the preferred architecture for next-generation avionics development programs.

The commercial off-the-shelf standard grade segment held a 30.9% share in 2025 due to its extensive use in cost-sensitive aerospace applications where radiation-hardened specifications are not essential. These microcontrollers are widely adopted in non-critical aerospace electronics because they offer faster availability, competitive pricing, and flexible sourcing options. Their ability to meet extended environmental and operational requirements while maintaining lower procurement costs continues to support their growing adoption across multiple aerospace applications. Increased reliance on scalable and commercially available semiconductor solutions is further strengthening demand for COTS-grade aerospace microcontrollers worldwide.

North America Aerospace Microcontroller Market captured 46.6% share in 2025, supported by the region's strong concentration of aircraft manufacturers, defense contractors, and satellite technology companies. Market expansion in the region is also driven by strict aerospace electronics certification requirements and continued investments in advanced avionics modernization programs. Regulatory standards introduced by the Federal Aviation Administration continue to reinforce compliance requirements for airborne electronic hardware, sustaining demand for certified aerospace microcontroller solutions across new aircraft programs and electronic system upgrades. Canada also contributes significantly to regional market growth through its expanding domestic space electronics capabilities and participation in commercial and government-supported satellite initiatives.

Major companies operating in the Global Aerospace Microcontroller Market include AMD, Analog Devices, BAE Systems, Cobham Advanced Electronic Solutions (CAES), Frontgrade Technologies, Honeywell Aerospace, Infineon Technologies, Intel, Microchip Technology, NanoXplore, NXP Semiconductors, onsemi, Renesas Electronics, STMicroelectronics, Teledyne e2v, Texas Instruments, and VORAGO Technologies. Companies active in the aerospace microcontroller market are adopting several strategic initiatives to strengthen their market position and expand their competitive advantage. Leading players are increasing investments in research and development to introduce high-performance aerospace-grade microcontrollers with improved processing efficiency, AI capabilities, and enhanced reliability for harsh operating environments. Many manufacturers are also focusing on multicore architecture development to address the growing complexity of avionics and autonomous aerospace systems. Strategic partnerships with aircraft manufacturers, defense contractors, and satellite developers remain a key growth strategy to secure long-term supply agreements and accelerate product integration into next-generation aerospace platforms. In addition, companies are expanding production capabilities, strengthening semiconductor supply chains, and pursuing regulatory certifications to improve product acceptance across commercial aviation, defense, and space applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Radiation hardness level trends

- 2.2.3 Platform trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expanding commercial aircraft production increasing demand for advanced avionics microcontrollers.

- 3.2.1.2 Rising defense modernization programs accelerating aerospace embedded electronics deployment globally

- 3.2.1.3 Growing satellite launches driving demand for radiation-tolerant aerospace microcontrollers worldwide

- 3.2.1.4 Increasing UAV adoption boosting requirement for compact high-performance aerospace MCUs

- 3.2.1.5 Stringent aircraft safety regulations encouraging reliable aerospace electronic system upgrades

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High aerospace certification requirements extending product development and commercialization timelines

- 3.2.2.2 Limited semiconductor supply creating procurement challenges for aerospace-grade microcontrollers globally

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging space exploration missions creating demand for advanced radiation-hardened microcontrollers

- 3.2.3.2 Increasing electric aircraft development opening opportunities for energy-efficient aerospace MCUs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 8-bit MCUs

- 5.3 16-bit MCUs

- 5.4 32-bit MCUs

- 5.5 64-bit MCUs

Chapter 6 Market Estimates and Forecast, By Radiation Hardness Level, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Radiation-hardened (TID >100 krad)

- 6.3 Radiation-tolerant (TID >30 to 100 krad)

- 6.4 Non-rad ruggedized (0 krad/ extended temp)

- 6.5 Commercial off-the-shelf (COTS) (standard grade)

Chapter 7 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.3 Military & defense aircrafts

- 7.4 Satellites

- 7.5 Spacecraft & launch vehicles

- 7.6 UAVs & drones

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Microchip Technology

- 9.1.2 Texas Instruments

- 9.1.3 Renesas Electronics

- 9.1.4 STMicroelectronics

- 9.1.5 NXP Semiconductors

- 9.1.6 Infineon Technologies

- 9.1.7 Intel

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 Honeywell Aerospace

- 9.2.1.2 AMD

- 9.2.1.3 Analog Devices

- 9.2.1.4 onsemi

- 9.2.1.5 VORAGO Technologies

- 9.2.2 Asia Pacific

- 9.2.2.1 NanoXplore

- 9.2.3 Europe

- 9.2.3.1 BAE Systems

- 9.2.3.2 Cobham Advanced Electronic Solutions (CAES)

- 9.2.3.3 Teledyne e2v

- 9.2.1 North America

- 9.3 Niche Players/Disruptors

- 9.3.1 Frontgrade Technologies