PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061372

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061372

Automotive Cockpit Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

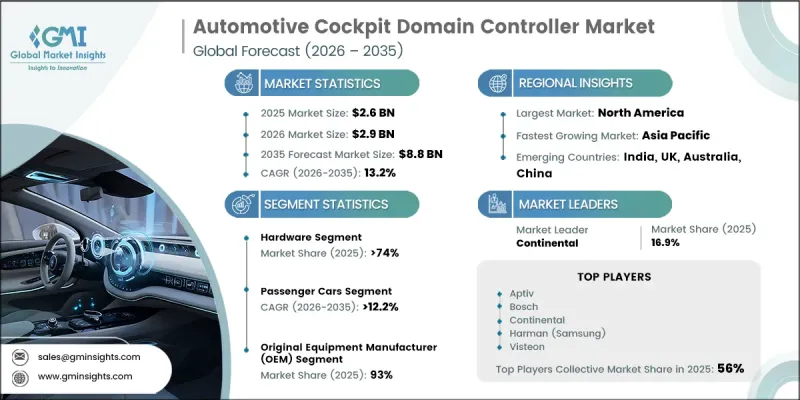

The Global Automotive Cockpit Domain Controller Market was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 13.2% to reach USD 8.8 billion by 2035.

Growth across the automotive cockpit domain controller industry is driven by the increasing demand for integrated vehicle electronics, advanced human-machine interface (HMI) technologies, and the transition toward software-defined vehicle architectures. Automakers and Tier-1 suppliers are making substantial investments in centralized and flexible domain controller platforms to create more connected, intelligent, and personalized in-vehicle experiences. As vehicle interiors evolve into digital environments, the need for high-performance computing platforms capable of managing multiple functions through a single architecture continues to increase. The growing integration of digital displays, connected services, intelligent software platforms, and advanced user interfaces is accelerating adoption across the automotive sector. Furthermore, rising consumer expectations for seamless connectivity, intuitive controls, and enhanced digital experiences are encouraging manufacturers to deploy sophisticated cockpit domain controller solutions. As modern vehicles become increasingly software-centric, centralized computing architectures are emerging as a critical component for improving operational efficiency, reducing system complexity, and enabling future mobility innovations. These trends are expected to support sustained market growth throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.6 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 13.2% |

The automotive cockpit domain controller market is also benefiting from increasing demand for advanced computing capabilities within vehicle cabins. The integration of intelligent cockpit functions, immersive digital experiences, and enhanced connectivity features requires significantly higher processing power, greater bandwidth capacity, and faster communication speeds. Continuous advancements in processor technologies and computing architectures are enabling more sophisticated in-vehicle functions while supporting real-time data processing and seamless system integration. In addition, the rapid adoption of electric vehicles and ongoing advancements in autonomous driving technologies are increasing the need for centralized data processing platforms that can efficiently manage multiple vehicle systems. Automotive cockpit domain controllers are becoming essential for supporting artificial intelligence-enabled applications, customizable user interfaces, predictive functionality, and enhanced driver assistance capabilities, further driving market demand.

The hardware segment accounted for 74% share in 2025, making it the leading segment within the industry. Growth in this segment is driven by the critical role of hardware components in supporting cockpit domain controller functionality. These systems depend on advanced processors, memory technologies, display management solutions, connectivity modules, and power management systems to deliver high-performance computing capabilities. The increasing consolidation of electronic control functions into centralized architectures is helping improve vehicle efficiency, reduce system complexity, and support scalable vehicle designs, particularly as electrification continues to expand across the automotive industry.

The passenger cars segment held 12.2% share during 2026 to 2035. Strong demand for advanced infotainment systems, digital instrument clusters, and intelligent human-machine interfaces continues to drive adoption within this segment. Vehicle manufacturers are increasingly implementing centralized and zonal cockpit architectures to support multiple displays, personalized user experiences, and enhanced driver assistance functionalities. The growing popularity of electric passenger vehicles and increasing demand for connected mobility solutions are further contributing to rising requirements for advanced data processing capabilities and next-generation connectivity technologies.

North America Automotive Cockpit Domain Controller Market generated USD 913.9 million in 2025. The region benefits from a well-established automotive ecosystem, advanced research and development capabilities, and strong adoption of software-driven vehicle technologies. Growing consumer interest in intelligent, connected, and digitally enhanced vehicle experiences is encouraging broader integration of cockpit domain controller solutions across both passenger and commercial vehicle categories. Continuous innovation in vehicle electronics and increasing investments in electric and autonomous mobility technologies are further supporting market expansion throughout North America.

Major companies operating in the Global Automotive Cockpit Domain Controller Industry include Aptiv, Continental, Denso, Faurecia, HARMAN, Intel, NVIDIA, Qualcomm Technologies, Robert Bosch, and Visteon. Companies operating in the automotive cockpit domain controller market are implementing several strategic initiatives to strengthen their competitive position and expand market share. Significant investments in research and development are focused on enhancing computing performance, artificial intelligence capabilities, software integration, and connectivity features. Strategic collaborations between automakers, semiconductor manufacturers, and technology providers are accelerating innovation and enabling the development of next-generation cockpit platforms. Market participants are also emphasizing centralized computing architectures that support multiple vehicle functions through a unified system. In addition, companies are expanding their software capabilities, developing scalable product portfolios, and integrating advanced digital experiences to meet evolving customer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Sources, by region

- 1.6.1 Base estimates and calculations

- 1.7 Base year calculation

- 1.8 Forecast

- 1.8.1 Quantified market impact analysis

- 1.8.2 Mathematical impact of growth parameters on forecast

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Connected and Software-Defined Vehicles

- 3.2.1.2 Transition Toward Centralized E/E Vehicle Architecture

- 3.2.1.3 Increasing Consumer Demand for Advanced Infotainment & Digital Cockpit Experiences

- 3.2.1.4 Growth of EVs and Autonomous Vehicles

- 3.2.1.5 OEM-Tier 1 Collaborations with Semiconductor & Software Players

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Integration & Software Validation Costs

- 3.2.2.2 Cybersecurity and Data Privacy Risks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Cloud-Enabled and OTA Update Ecosystems

- 3.2.3.2 Growing Penetration in Emerging Markets (APAC, LATAM, MEA)

- 3.2.3.3 Advanced HMI & Multimodal Interaction Systems

- 3.2.3.4 Integration with Mobility Services and Fleet Applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S. - NHTSA Vehicle Safety Standards & Automotive Cybersecurity Regulations

- 3.5.1.2 Canada - Transport Canada Vehicle Electronics & Connected Car Regulations

- 3.5.2 Europe

- 3.5.2.1 Germany - UNECE WP.29 Cybersecurity & German Automotive Functional Safety Standards

- 3.5.2.2 United Kingdom - UK Vehicle Type Approval & Connected Vehicle Cybersecurity Framework

- 3.5.2.3 France - EU Automotive Software Compliance & Functional Safety Regulations

- 3.5.3 Asia Pacific

- 3.5.3.1 China - China Intelligent Connected Vehicle & Automotive Data Security Regulations

- 3.5.3.2 India - AIS Standards & Automotive Electronics Safety Regulations

- 3.5.3.3 Japan - Japan Automotive Cybersecurity & Autonomous Vehicle Safety Regulations

- 3.5.4 Latin America

- 3.5.4.1 Brazil Vehicle Connectivity & Automotive Electronics Compliance Standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 Saudi Arabia - SASO Automotive Electronics & Smart Mobility Regulations

- 3.5.1 North America

- 3.6 Porter's analysis

- 3.7 Pestel analysis

- 3.8 Technology & innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI & Generative AI on the Market (Driven by Primary Research)

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 System on Chip (SoC)

- 5.2.2 Modules

- 5.2.3 Memory

- 5.2.4 Connectivity

- 5.2.5 Display Interfaces

- 5.2.6 Camera & Sensors

- 5.2.7 Power Management IC

- 5.2.8 Others

- 5.3 Software

- 5.3.1 Middleware

- 5.3.2 Hypervisor / Virtualization

- 5.3.3 OTA Update Software

- 5.3.4 Cybersecurity Software

- 5.3.5 Others

- 5.4 Services

- 5.4.1 Professional Services

- 5.4.2 Managed Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Centralized architecture

- 7.3 Distributed architecture

- 7.4 Zonal architecture

- 7.5 Hybrid architecture

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Original equipment manufacturer (OEM) channel

- 8.3 Aftermarket channel

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Infotainment Systems

- 9.3 Digital Instrument Cluster

- 9.4 V2X Communication Interface

- 9.5 OTA Update Management

- 9.6 Driver Monitoring Systems

- 9.7 Other

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Denso

- 11.1.4 HARMAN

- 11.1.5 Intel

- 11.1.6 NVIDIA

- 11.1.7 Qualcomm Technologies

- 11.1.8 Robert Bosch

- 11.1.9 STMicroelectronics

- 11.1.10 Texas Instruments

- 11.1.11 Visteon

- 11.1.12 Valeo

- 11.2 Regional Players

- 11.2.1 Hyundai Mobis

- 11.2.2 Infineon Technologies

- 11.2.3 Magna International

- 11.2.4 NXP Semiconductors

- 11.2.5 Panasonic

- 11.2.6 Sony

- 11.2.7 BYD Company

- 11.2.8 Huawei Technologies

- 11.2.9 Tesla