PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061381

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061381

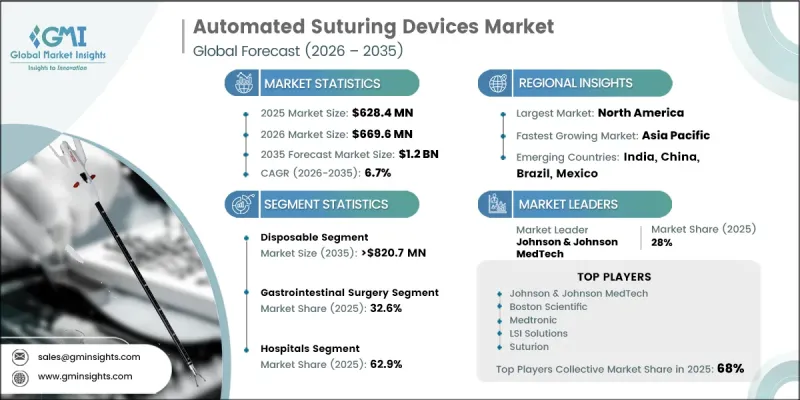

Automated Suturing Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Automated Suturing Devices Market was valued at USD 628.4 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 1.2 billion by 2035.

Market expansion is driven by the rising number of surgical interventions globally, increasing incidence of trauma and accident-related cases, and continuous advancements in robotic-assisted surgical technologies. The growing burden of chronic illnesses, an aging global population, and a steady rise in elective procedures are collectively pushing surgical volumes higher, strengthening demand for efficient wound closure solutions. Automated suturing devices are increasingly being adopted by healthcare providers to streamline surgical workflows, reduce operating time, and enhance procedural accuracy while minimizing surgeon fatigue. Their ability to deliver consistent suturing outcomes is improving patient recovery rates and reducing complication risks. Adoption is especially strong in high-volume specialties such as orthopedic, cardiovascular, and gastrointestinal surgeries. In parallel, integration with robotic surgical platforms is enhancing precision, dexterity, and visualization during complex procedures, supporting minimally invasive approaches and further accelerating market uptake across modern healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $628.4 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.7% |

The disposable segment accounted for 64.5% share in 2025, supported by a strong preference for single-use surgical tools that help minimize infection risks and comply with strict clinical hygiene standards. Demand for disposable automated suturing devices continues to rise due to their operational simplicity, elimination of reprocessing requirements, and suitability for fast-paced surgical environments. These devices reduce the possibility of cross-contamination and support safer surgical practices, particularly in facilities handling high patient turnover. Their convenience and reliability are reinforcing widespread clinical adoption across healthcare systems focused on improving efficiency and safety outcomes.

The gastrointestinal surgery segment captured a share of 32.6% in 2025. Automated suturing devices are widely utilized in gastrointestinal procedures where precision, speed, and secure tissue closure are critical, particularly in minimally invasive laparoscopic interventions. Their use enables surgeons to perform accurate suturing in confined anatomical spaces while reducing procedure time and improving postoperative recovery outcomes. They also help lower the risk of complications such as leakage and improper wound closure. The increasing incidence of gastrointestinal conditions, along with growing adoption of advanced surgical techniques, continues to drive sustained demand for these devices in this segment.

North America Automated Suturing Devices Market held a 33.4% share in 2025. The region benefits from a highly developed healthcare infrastructure, early adoption of robotic-assisted surgical systems, and a strong preference for minimally invasive procedures. A high surgical caseload driven by chronic diseases and an aging population further supports consistent demand for automated suturing technologies. The presence of leading medical device manufacturers, advanced reimbursement frameworks, and ongoing investments in clinical training and surgical innovation continue to strengthen regional market growth. Widespread integration of next-generation surgical platforms is also enhancing adoption rates across hospitals and surgical centers.

Major companies operating in the Global Automated Suturing Devices Market include Boston Scientific, Johnson & Johnson MedTech, Medtronic, Anchora Medical, ErgoSuture, LSI Solutions, Mellon Medical, and Suturion. Companies in the automated suturing devices market are focusing on continuous product innovation, through integration with robotic-assisted surgical systems to improve precision and procedural control. Many players are expanding their product portfolios with advanced disposable and reusable suturing solutions tailored for different surgical specialties. Strategic collaborations with hospitals, research institutions, and surgical centers are being used to accelerate clinical adoption and expand application areas. Firms are also investing in surgeon training programs to improve device proficiency and adoption rates. Geographic expansion into emerging healthcare markets is strengthening revenue streams.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of surgical procedures

- 3.2.1.2 Technological advancements in robotic-assisted surgery

- 3.2.1.3 Growing number of accidents and trauma cases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of automated suturing devices

- 3.2.2.2 Limited adoption in developing and low-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for outpatient and same-day surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing trend analysis, 2025

- 3.10 Start-up scenarios (Driven by primary research)

- 3.11 Impact of AI & generative AI on the market

- 3.12 Investment & funding analysis

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Disposable

- 5.3 Reusable

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Gastrointestinal surgery

- 6.3 Cardiovascular surgery

- 6.4 Gynecological surgery

- 6.5 Orthopedic surgery

- 6.6 Ophthalmic surgery

- 6.7 Other surgical applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anchora Medical

- 9.2 Boston Scientific

- 9.3 ErgoSuture

- 9.4 Johnson & Johnson MedTech

- 9.5 LSI Solutions

- 9.6 Medtronic

- 9.7 Mellon Medical

- 9.8 Suturion