PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061387

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061387

Data Center Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

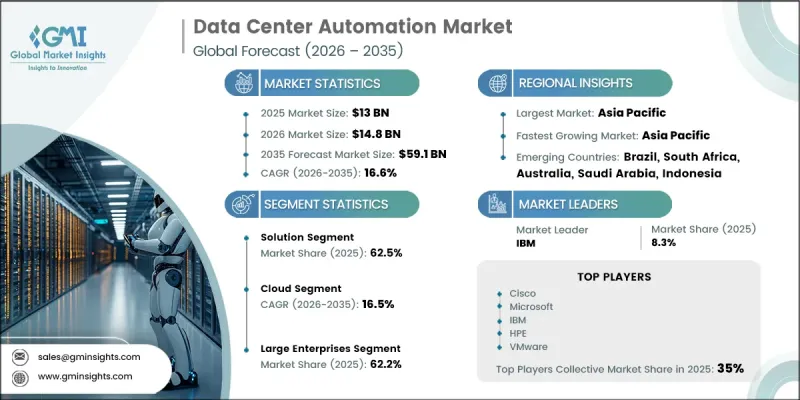

The Global Data Center Automation Market was valued at USD 13 billion in 2025 and is estimated to grow at a CAGR of 16.6% to reach USD 59.1 billion by 2035.

The market is expanding rapidly as enterprises increasingly deploy intelligent automation platforms, AI-enabled monitoring systems, and advanced analytics to improve data center performance, energy efficiency, and operational reliability. Rising demand for scalable and resilient IT infrastructure, combined with the accelerated shift toward cloud computing and hybrid IT environments, is significantly boosting market growth. Organizations are prioritizing reduced downtime, improved workload efficiency, and cost optimization, which is further driving the adoption of automation technologies. In addition, the exponential growth of digital data is increasing pressure on data center infrastructure, encouraging widespread implementation of automated management systems. AI-driven automation is enabling predictive maintenance, dynamic workload balancing, and autonomous incident handling by analyzing multiple inputs such as thermal conditions, network traffic, and power usage in real time. These advancements are transforming traditional facilities into self-optimizing environments that improve performance while lowering operational costs. Regionally, adoption trends vary, with mature markets advancing faster due to established digital ecosystems and higher investments in large-scale infrastructure transformation initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13 Billion |

| Forecast Value | $59.1 Billion |

| CAGR | 16.6% |

The solution segment held a 62.5% share and is expected to grow at a CAGR of 15.8% through 2035. This segment benefits from increasing reliance on automation platforms that manage orchestration, monitoring, and workload distribution across complex IT environments. Modern data centers are increasingly deploying centralized software systems that enable real-time visibility, policy-driven automation, and improved infrastructure control across hybrid and multi-cloud setups. AI-powered tools further enhance capabilities by enabling predictive maintenance, identifying anomalies, and automating response workflows, thereby improving efficiency and reducing operational risks.

The cloud segment accounted for a 58% share of the market in 2025 and is projected to grow at a CAGR of 16.5% from 2026 to 2035. Cloud-based automation platforms continue to drive innovation in the sector by offering scalable, flexible, and highly efficient infrastructure management capabilities. These platforms support advanced functionalities such as autonomous operations, predictive analytics, and real-time workload optimization, enabling enterprises to improve agility and reduce operational complexity. Growing enterprise reliance on cloud environments is further accelerating the deployment of automated infrastructure management solutions across industries.

Asia Pacific Data Center Automation Market held a 22.8% share in 2025 and is expected to grow at a CAGR of 17.5% during 2026-2035. The region's growth is fueled by rapid digital transformation, increasing internet penetration, and significant investments in cloud and data center infrastructure. Strong demand for automation technologies is emerging across major economies due to the expansion of digital services, artificial intelligence applications, and next-generation connectivity networks.

Key companies operating in the Global Data Center Automation Market include Microsoft, IBM, Cisco, HPE, VMware, Fujitsu, Juniper Networks, ABB, BMC Software, and NTT Communications. Companies in the data center automation market are focusing on strengthening their competitive positioning through continuous innovation in AI-driven infrastructure management and intelligent orchestration platforms. A major strategy involves heavy investment in research and development to enhance automation capabilities, improve predictive analytics accuracy, and enable real-time operational decision-making across complex IT environments. Market participants are also forming strategic partnerships with cloud providers, enterprise IT vendors, and hyperscale operators to expand ecosystem integration and accelerate solution deployment. In addition, firms are scaling up cloud-native automation offerings to meet growing demand for flexible and scalable infrastructure management. Expansion into high-growth regions, coupled with acquisitions and collaborations, is helping companies broaden their global footprint. Vendors are also prioritizing cybersecurity integration and end-to-end visibility features to enhance trust and reliability, ensuring stronger adoption across enterprise and large-scale data center environments.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Organization size

- 2.2.5 Application

- 2.2.6 Data center type

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising volumes of data.

- 3.2.1.2 The rise of cloud computing, machine learning and artificial intelligence.

- 3.2.1.3 Reduction of operational cost.

- 3.2.1.4 Resolve issues to minimize the downtime.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled professionals.

- 3.2.2.2 Complexity in implementation.

- 3.2.3 Market opportunities

- 3.2.3.1 Hybrid and Multi-Cloud Adoption Driving Automation Demand

- 3.2.3.2 Integration of AI, Machine Learning, and AIOps in Data Centers

- 3.2.3.3 Growth of Infrastructure-as-Code and DevOps Automation Practices

- 3.2.3.4 Focus on Energy Efficiency and Sustainable Data Center Operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 AI and Automation for Infrastructure Management

- 3.4.1.2 5G and IoT Integration

- 3.4.1.3 Modular and Micro Data Center Designs

- 3.4.1.4 Real-Time Monitoring and Analytics

- 3.4.2 Emerging technologies

- 3.4.2.1 AI-Driven Autonomous Edge Orchestration

- 3.4.2.2 6G-Enabled Ultra-Low Latency Edge Networks

- 3.4.2.3 Digital Twin for Edge Data Center Optimization

- 3.4.2.4 Quantum-Safe Edge Security Infrastructure

- 3.4.1 Current technological trends

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 United States driver monitoring and vehicle safety regulations (NHTSA)

- 3.6.1.2 U.S. data privacy and biometric data laws

- 3.6.1.3 Automotive cybersecurity and software compliance standards

- 3.6.1.4 Canada vehicle safety and data protection regulations (PIPEDA)

- 3.6.2 Europe

- 3.6.2.1 EU General Safety Regulation (driver monitoring mandate)

- 3.6.2.2 GDPR data privacy and biometric compliance

- 3.6.2.3 UNECE cybersecurity and software update regulations (R155, R156)

- 3.6.2.4 National vehicle homologation requirements

- 3.6.3 Asia Pacific

- 3.6.3.1 China data protection laws (PIPL, CSL, DSL)

- 3.6.3.2 China automotive data security regulations

- 3.6.3.3 India automotive safety and driver monitoring guidelines

- 3.6.3.4 Japan intelligent mobility and vehicle safety regulations

- 3.6.3.5 South Korea data protection and connected vehicle rules

- 3.6.4 Latin America

- 3.6.4.1 Brazil data protection law (LGPD) and vehicle safety standards

- 3.6.4.2 Mexico automotive safety and data privacy regulations

- 3.6.4.3 Argentina vehicle safety and data protection frameworks

- 3.6.4.4 Regional automotive certification standards

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE vehicle safety and smart mobility regulations

- 3.6.5.2 Saudi Arabia automotive safety and data governance

- 3.6.5.3 South Africa vehicle safety and data protection standards

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Cost breakdown analysis

- 3.11 Impact of AI and Generative AI on the Market

- 3.11.1 AI Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.11.3 Risks Limitations and Regulatory Considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Server automation

- 5.2.2 Network automation

- 5.2.3 Storage automation

- 5.2.4 Security automation

- 5.2.5 Others

- 5.3 Service

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization size, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Colocation

- 8.4 Energy

- 8.5 Government

- 8.6 Healthcare

- 8.7 Manufacturing

- 8.8 IT & Telecom

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Data Center Type, 2022 - 2035 (USD Mn)

- 9.1 Key trends

- 9.2 Enterprise data center

- 9.3 Colocation data center

- 9.4 Public cloud data center

- 9.5 Edge data center

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Broadcom

- 11.1.3 Cisco Systems

- 11.1.4 Hewlett Packard Enterprise (HPE)

- 11.1.5 IBM

- 11.1.6 Microsoft

- 11.1.7 Juniper Networks

- 11.1.8 Oracle

- 11.1.9 Arista Networks

- 11.2 Regional Players

- 11.2.1 BMC Software

- 11.2.2 Citrix

- 11.2.3 OpenText (Micro Focus)

- 11.2.4 NTT Communications

- 11.2.5 Fujitsu

- 11.2.6 Rockwell Automation

- 11.2.7 Huawei Technologies

- 11.2.8 Schneider Electric

- 11.2.9 Hitachi Vantara

- 11.3 Emerging Players / Disruptors

- 11.3.1 Progress Chef

- 11.3.2 Puppet

- 11.3.3 Nutanix

- 11.3.4 Datadog

- 11.3.5 Elastic

- 11.3.6 PagerDuty