PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061395

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061395

Progesterone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

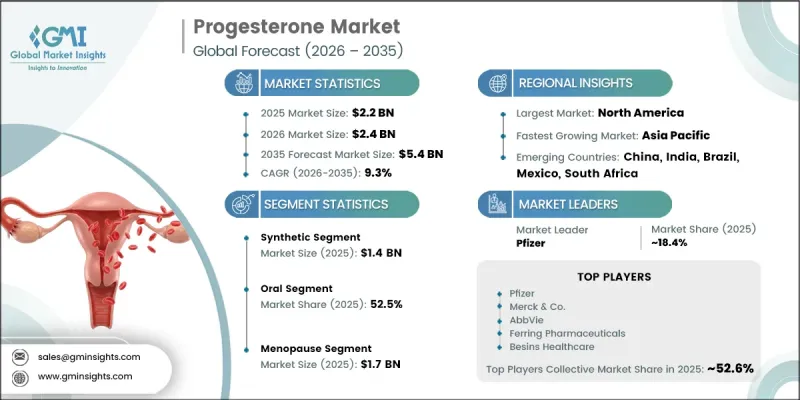

The Global Progesterone Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 5.4 billion by 2035.

Market expansion is supported by the rising incidence of hormonal imbalances, increasing uptake of hormone replacement therapy (HRT), higher infertility treatment rates worldwide, and growing awareness of women's reproductive and hormonal health. Demand is also being reinforced by the expanding role of progesterone in reproductive medicine, where it is widely used to regulate menstrual cycles, support pregnancy maintenance, reduce risks linked to miscarriage and preterm birth, and manage menopausal symptoms. The hormone continues to be extensively utilized across contraception, assisted reproductive technologies (ART), infertility care, and menopausal therapy, making it a core component of gynecological treatment protocols. Rising global infertility prevalence, affecting millions of individuals of reproductive age as highlighted by global health assessments, is further strengthening the need for hormonal support therapies. In parallel, the increasing adoption of ART procedures such as IVF and embryo transfer is significantly boosting demand for progesterone-based formulations, including capsules, gels, injections, and vaginal delivery systems across healthcare settings.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 9.3% |

The synthetic segment accounted for USD 1.4 billion in 2025 and is projected to grow at a CAGR of 9.5% through 2035. The strong performance of synthetic progesterone products is driven by their extensive use in oral contraceptives, hormone replacement therapy, infertility treatment protocols, and gynecological disorder management. These formulations are widely preferred due to their long-standing clinical usage, cost efficiency, high stability, and extended shelf life, making them suitable for large-scale healthcare deployment. Market growth is further supported by the broad availability of generic synthetic hormone therapies and their inclusion in combination treatment regimens, which enhances accessibility across both developed and emerging healthcare systems.

The oral segment held a share of 52.5% in 2025. Oral progesterone therapies are widely adopted due to their ease of use, strong physician preference, and broad application across hormone replacement therapy, infertility management, menstrual disorder treatment, and pregnancy support care. Their popularity is reinforced by improved patient adherence, simple administration, and the increasing availability of sustained-release formulations that enhance absorption and therapeutic performance. Growing use among menopausal patients receiving bioidentical hormone therapy has further strengthened demand for oral progesterone products globally.

North America Progesterone Industry held a 37.8% in 2025. The region's leadership is driven by high adoption rates of hormone replacement therapy, increasing fertility treatment procedures, and strong awareness of reproductive health management among patients and healthcare providers. The United States, in particular, benefits from a well-established fertility treatment ecosystem, where rising IVF and embryo transfer procedures continue to support strong demand for progesterone in luteal phase support. Continuous advancements in micronized oral progesterone formulations, increasing acceptance of bioidentical hormone therapies, and strong clinical awareness further reinforce market growth across the region.

Key companies operating in the Global Progesterone Market include AbbVie, Pfizer, Merck & Co., Bayer AG, Organon, Viatris (Mylan), Teva Pharmaceutical Industries, Sun Pharmaceutical Industries, Lupin Limited, Cipla, Ferring Pharmaceuticals, Gedeon Richter, Glenmark Pharmaceuticals, Alkem Laboratories, Zydus Lifesciences, Besins Healthcare, TherapeuticsMD, and Xiromed. Companies in the progesterone market are increasingly focusing on expanding their hormone therapy portfolios through the development of advanced and patient-friendly formulations that improve treatment adherence and therapeutic outcomes. A major strategy involves strengthening research and development efforts to enhance the bioavailability and stability of progesterone-based products, particularly in oral and micronized delivery systems. Firms are also investing in fertility-focused treatment innovations aligned with the rising demand for assisted reproductive technologies such as IVF and embryo transfer procedures. Strategic collaborations with fertility clinics and healthcare providers are being used to expand prescription reach and improve patient access. In addition, companies are leveraging generic product expansion strategies to strengthen market penetration across cost-sensitive regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Formulation trends

- 2.2.3 Route of administration trends

- 2.2.4 Drug type trends

- 2.2.5 Type trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of infertility and hormonal disorders

- 3.2.1.2 Growing adoption of hormone replacement therapy (HRT)

- 3.2.1.3 Expansion of women’s healthcare infrastructure and reproductive medicine

- 3.2.1.4 Advancements in drug delivery formulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Side effects and safety concerns associated with hormone therapy

- 3.2.2.2 Stringent regulatory and clinical approval requirements

- 3.2.2.3 Availability of alternative fertility and hormone therapies

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for bioidentical and personalized hormone therapies

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape (Driven by primary research)

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 MEA

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Future market trends (Driven by primary research)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical price trend analysis

- 3.8.2 Pricing strategy, by formulation

- 3.9 Pipeline analysis and clinical trial landscape

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Investment & funding analysis

- 3.12 Fertility rates, by country (births per woman)

- 3.13 Gap analysis

- 3.14 Impact of AI & Generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Formulation, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Natural

- 5.3 Synthetic

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Injectable

- 6.3 Oral

- 6.4 Transdermal

- 6.5 Other routes of administration

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Menopause

- 7.3 Contraception

- 7.4 Dysfunctional uterine bleeding

- 7.5 Hyperplastic precursor lesions

- 7.6 Endometrial cancer

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By Drug Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Branded

- 8.3 Generic

Chapter 9 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 9.1 Prescription

- 9.2 OTC

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacy

- 10.3 Retail pharmacy

- 10.4 Online pharmacy

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Alkem Laboratories

- 12.3 Bayer AG

- 12.4 Besins Healthcare

- 12.5 Cipla

- 12.6 Ferring Pharmaceuticals

- 12.7 Glenmark Pharmaceuticals

- 12.8 Gedeon Richter

- 12.9 Lupin Limited

- 12.10 Merck & Co.

- 12.11 Organon

- 12.12 Pfizer

- 12.13 Sun Pharmaceutical Industries

- 12.14 Teva Pharmaceutical Industries

- 12.15 TherapeuticsMD

- 12.16 Viatris (Mylan)

- 12.17 Xiromed

- 12.18 Zydus Lifesciences