PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061396

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061396

Cargo Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

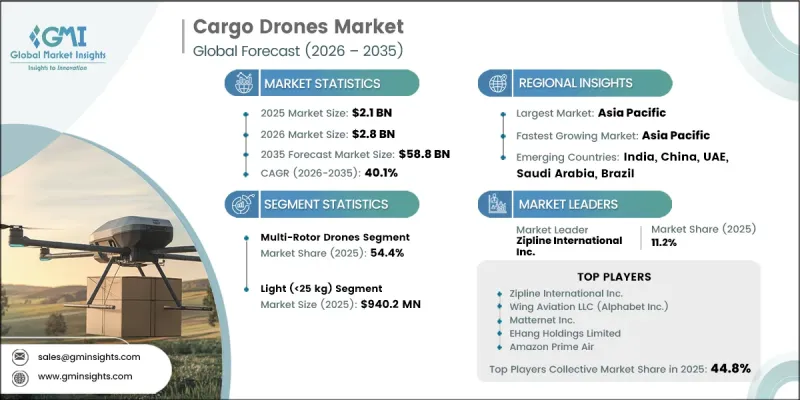

The Global Cargo Drones Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 40.1% to reach USD 58.8 billion by 2035.

The market is witnessing rapid growth due to the increasing development of regulatory frameworks supporting long-distance drone operations and the rising adoption of unmanned aerial delivery systems across multiple industries. Cargo drones are gaining strong momentum in healthcare logistics, where fast and efficient transportation of essential supplies is becoming increasingly important. In addition, defense organizations are expanding the use of cargo drones for transporting materials and equipment in difficult and remote environments, strengthening market demand. The growing transition toward automated logistics ecosystems, combined with continuous improvements in payload capabilities and flight efficiency, is further increasing the commercial viability of cargo drone deployment. Expanding investments in advanced air mobility infrastructure and autonomous transportation technologies are also supporting large-scale market development. Furthermore, the integration of intelligent navigation systems, AI-driven route optimization, and enhanced battery technologies is improving operational efficiency and reliability, making cargo drones an increasingly attractive solution for modern logistics and transportation networks worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $58.8 Billion |

| CAGR | 40.1% |

The cargo drones market is further supported by the increasing advancement of Beyond Visual Line of Sight (BVLOS) operations, which enable drones to perform long-distance missions without direct visual supervision. These capabilities significantly improve the scalability and efficiency of drone-based logistics networks. In addition, the development of dedicated urban drone infrastructure, including air corridors and drone landing facilities, is improving operational coordination and reducing congestion within urban airspaces. Growing investments by governments and private organizations in integrated air mobility systems are expected to accelerate commercial deployment across metropolitan and regional logistics networks through the coming decade.

The hybrid VTOL drones segment is expected to grow at a CAGR of 41.3% during 2026-2035. This growth is attributed to the capability of hybrid VTOL platforms to combine vertical takeoff functionality with extended flight range and higher payload performance. These systems are increasingly being adopted for intercity transportation and remote-area logistics operations where long-distance delivery efficiency is critical. Rising demand for operational flexibility and cost-efficient logistics solutions continues to strengthen adoption across commercial sectors.

The light payload segment, consisting of drones carrying less than 25 kg reached USD 940.2 million in 2025. The segment maintains strong market leadership due to its suitability for short-range delivery applications and lower operational and regulatory complexities. These drones are comparatively easier to manufacture, deploy, and maintain, making them highly attractive for last-mile delivery and commercial logistics operations. Their affordability and ease of integration into urban delivery systems continue to support widespread market adoption.

North America Cargo Drones Market accounted for 43.4% share in 2025. The regional market is expanding rapidly due to supportive regulatory developments and the implementation of structured airspace integration programs that facilitate commercial drone operations. Government agencies are increasingly supporting advanced air mobility initiatives and BVLOS deployment programs, which are accelerating cargo drone adoption across logistics and public service sectors. The strong presence of aerospace manufacturers and drone technology providers in the region further supports commercialization and large-scale deployment activities.

Major companies operating in the Global Cargo Drones Market include Zipline International Inc., Wing Aviation LLC (Alphabet Inc.), Matternet Inc., Volocopter GmbH, EHang Holdings Limited, Dronamics Ltd., Amazon Prime Air, Elroy Air Inc., VastArrive, Skyports Infrastructure, Swoop Aero, Wingcopter GmbH, Natilus Inc., Pipistrel VTOL, Valqari, Manna Aero, Volans-i, Airspace Link, Skyward (Verizon), and Flyte Systems. Companies operating in the cargo drones market are focusing on expanding their technological capabilities through continuous investments in autonomous flight systems, advanced navigation technologies, and AI-powered fleet management platforms. Strategic collaborations with logistics providers, healthcare organizations, and government agencies are helping companies accelerate commercial deployment and strengthen operational networks. Manufacturers are also prioritizing the development of hybrid VTOL systems and long-range drones to improve payload efficiency and operational flexibility. Investments in urban air mobility infrastructure, including drone ports and air traffic integration systems, are further supporting scalability. In addition, companies are working on enhancing battery performance, flight safety systems, and real-time communication technologies to improve reliability and reduce operational risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Payload capacity trends

- 2.2.3 Range trends

- 2.2.4 Propulsion type trends

- 2.2.5 Autonomy level trends

- 2.2.6 End-use industry trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of beyond visual line of sight (BVLOS) operations enabling long range cargo delivery

- 3.2.1.2 Integration into healthcare supply chains for critical medical deliveries

- 3.2.1.3 Growing deployment in defense and tactical logistics operations

- 3.2.1.4 Shift toward autonomous and digitized connected logistics networks

- 3.2.1.5 Development of high-payload and long-endurance cargo drone platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory fragmentation across regions

- 3.2.2.2 High operational cost of large-scale drone logistics deployment

- 3.2.3 Market opportunities

- 3.2.3.1 Development of dedicated drone logistics hubs and infrastructure

- 3.2.3.2 Expansion into commercial middle-mile and intercity logistics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Multi-rotor drones

- 5.3 Fixed-wing drones

- 5.4 Hybrid VTOL drones

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Light (<25 kg)

- 6.3 Medium (25-100 kg)

- 6.4 Heavy (>100 kg)

Chapter 7 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Close-range (<50 km)

- 7.3 Short-range (50-149 km)

- 7.4 Mid-range (150-650 km)

- 7.5 Long-range (>650 km)

Chapter 8 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Battery-electric

- 8.3 Hydrogen/fuel cell

- 8.4 Hybrid

Chapter 9 Market Estimates and Forecast, By Autonomy Level, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Fully autonomous

- 9.3 Semi-autonomous

- 9.4 Remotely piloted

Chapter 10 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 Healthcare and emergency services

- 10.2.1 Medical supply delivery

- 10.2.2 Blood and organ transport

- 10.2.3 Emergency response and disaster relief

- 10.2.4 Others

- 10.3 Retail and e-commerce

- 10.3.1 Last-mile delivery

- 10.3.2 Inter-hub cargo transport

- 10.3.3 Warehouse transfer operations

- 10.3.4 Others

- 10.4 Defense and security

- 10.4.1 Field resupply

- 10.4.2 Border patrol logistics

- 10.4.3 Disaster evacuation support

- 10.4.4 Others

- 10.5 Agriculture

- 10.6 Infrastructure and construction

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Zipline International Inc.

- 12.1.2 Wing Aviation LLC (Alphabet Inc.)

- 12.1.3 Matternet Inc.

- 12.1.4 EHang Holdings Limited

- 12.1.5 Amazon Prime Air

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 Elroy Air Inc.

- 12.2.1.2 Natilus Inc.

- 12.2.1.3 Valqari

- 12.2.1.4 Airspace Link

- 12.2.1.5 Skyward (Verizon)

- 12.2.1.6 Flyte Systems

- 12.2.2 Asia Pacific

- 12.2.2.1 VastArrive

- 12.2.3 Europe

- 12.2.3.1 Volocopter GmbH

- 12.2.3.2 Dronamics Ltd.

- 12.2.3.3 Wingcopter GmbH

- 12.2.3.4 Skyports Infrastructure

- 12.2.3.5 Pipistrel VTOL

- 12.2.3.6 Manna Aero

- 12.2.4 Middle East & Africa

- 12.2.4.1 Swoop Aero

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Volans-i.