PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061419

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061419

Antifungal Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

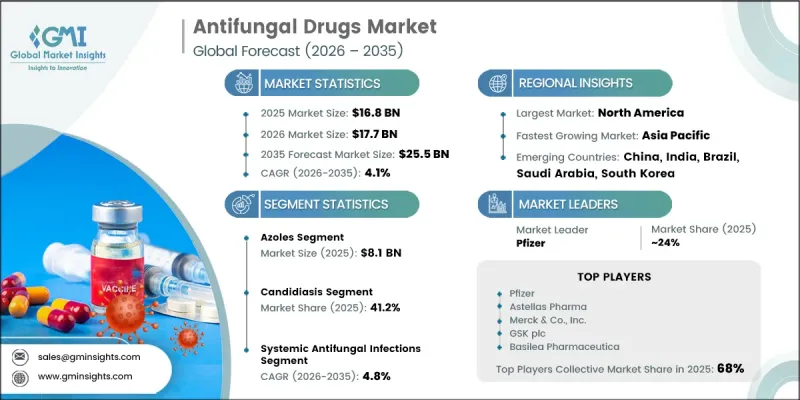

The Global Antifungal Drugs Market was valued at USD 16.8 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 25.5 billion by 2035.

The market is steadily advancing due to the growing occurrence of fungal infections across healthcare settings, coupled with the increasing population of immunocompromised patients worldwide. Rising cases of hospital-associated fungal infections and growing awareness regarding timely diagnosis and treatment of invasive fungal diseases are further supporting market expansion. In addition, concerns surrounding antifungal resistance have intensified due to the rapid spread of multidrug-resistant fungal pathogens, creating strong demand for more effective therapeutic solutions. The industry is also benefiting from ongoing advancements in pharmaceutical research, improved access to healthcare services, and expanding adoption of antifungal therapies in both developed and emerging economies. Increasing investments in infectious disease management and rising emphasis on preventive healthcare measures are further contributing to long-term market growth. As healthcare providers continue focusing on advanced treatment protocols and early intervention strategies, the demand for innovative antifungal medications is expected to remain strong throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.8 Billion |

| Forecast Value | $25.5 Billion |

| CAGR | 4.1% |

The antifungal drugs market focuses on the prevention, treatment, and management of superficial, systemic, and invasive fungal infections through multiple therapeutic drug categories. These medications are widely prescribed for a broad range of fungal conditions affecting different parts of the body. Growing concern regarding resistant fungal strains is significantly transforming the competitive landscape of the industry. The rapid spread of highly resistant fungal organisms across healthcare facilities has increased the urgency for effective treatment approaches and advanced antifungal formulations. In addition, rising healthcare awareness and improvements in diagnostic technologies are supporting earlier detection and faster treatment initiation. The market is also witnessing increased clinical demand for therapies that offer enhanced efficacy, improved safety profiles, and broader antifungal coverage, which continues to drive product innovation and commercialization activities globally.

The azoles segment generated USD 8.1 billion in 2025 owing to its broad-spectrum antifungal activity and strong clinical acceptance across healthcare settings. Azole-based antifungal therapies continue to be widely utilized because of their flexibility in treatment applications and availability in multiple formulations. Their extensive use in hospital environments, outpatient care facilities, and preventive treatment programs has further strengthened segment growth. In addition, physician familiarity, favorable absorption characteristics, and established therapeutic effectiveness continue to support the widespread adoption of azole antifungal medications. The segment is also benefiting from continued use in first-line treatment approaches for multiple fungal conditions, reinforcing its dominance in the global antifungal drugs market.

The candidiasis segment accounted for 41.2% share in 2025. Candidiasis remains one of the most diagnosed fungal infections worldwide, contributing significantly to the demand for antifungal therapies. The growing prevalence and increasing severity of fungal diseases have improved awareness regarding early diagnosis and treatment, resulting in greater utilization of antifungal medications. Rising healthcare initiatives focused on infection management and increasing clinical attention toward fungal disease complications are also supporting segment expansion. Furthermore, the increasing burden of fungal infections among vulnerable patient populations continues to accelerate the demand for effective treatment solutions targeting candidiasis.

North America Antifungal Drugs Market held 38.6% share in 2025. The region continues to dominate the industry due to its advanced healthcare infrastructure, high diagnosis and treatment rates, and the strong presence of major pharmaceutical companies engaged in antifungal drug development and commercialization. The growing number of fungal infection cases among immunocompromised individuals, aging populations, oncology patients, and organ transplant recipients is significantly contributing to market demand across the region. In addition, favorable reimbursement systems, increasing healthcare expenditure, and ongoing investments in infectious disease research are supporting continued market expansion throughout North America.

Key companies operating in the Antifungal Drugs Market include Pfizer, Merck & Co., Gilead Sciences, Novartis AG, Sanofi, Astellas Pharma, Bayer AG, GlaxoSmithKline, Cipla, Hikma Pharmaceuticals, Glenmark Pharmaceuticals, Sun Pharmaceutical Industries, and Scynexis. Companies active in the antifungal drugs market are implementing several strategic initiatives to strengthen their market position and expand their global footprint. Leading pharmaceutical manufacturers are increasing investments in research and development activities to introduce advanced antifungal therapies capable of addressing resistant fungal strains and improving treatment outcomes. Strategic collaborations, licensing agreements, and partnerships with research institutions are also helping companies accelerate product innovation and clinical development programs. In addition, businesses are focusing on expanding their product portfolios through new drug approvals, formulation enhancements, and geographic expansion into high-growth healthcare markets. Manufacturers are also prioritizing the development of therapies with improved efficacy, broader antifungal coverage, and enhanced patient safety profiles.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug class trends

- 2.2.3 Indication trends

- 2.2.4 Infection type trends

- 2.2.5 Route of administration trends

- 2.2.6 Medication trends

- 2.2.7 Type trends

- 2.2.8 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of invasive and opportunistic fungal infections

- 3.2.1.2 Growing immunocompromised patient population

- 3.2.1.3 Advancements in antifungal drug development

- 3.2.1.4 Expansion of rapid fungal diagnostic technologies

- 3.2.1.5 Growing awareness regarding antifungal resistance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising antifungal resistance

- 3.2.2.2 High treatment costs for advanced antifungal therapies

- 3.2.2.3 Limited awareness and delayed diagnosis

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of novel antifungal pipelines

- 3.2.3.2 Increasing healthcare investments in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies (Driven by Primary Research)

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy, by drug class

- 3.7 Pipeline analysis and clinical trial landscape

- 3.8 Impact of AI & Generative AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Azoles

- 5.3 Echinocandins

- 5.4 Polyenes

- 5.5 Allylamines

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Indication, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dermatophytosis

- 6.3 Aspergillosis

- 6.4 Candidiasis

- 6.5 Mucormycosis

- 6.6 Other indications

Chapter 7 Market Estimates and Forecast, By Infection Type, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Systemic antifungal infections

- 7.3 Superficial antifungal infections

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Topical

- 8.4 Injectable

Chapter 9 Market Estimates and Forecast, By Medication, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Prescription

- 9.3 OTC

Chapter 10 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 Branded

- 10.3 Generic

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 11.1 Key trends

- 11.2 Hospital pharmacies

- 11.3 Retail pharmacies

- 11.4 Online pharmacies

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Astellas Pharma

- 13.2 Bayer AG

- 13.3 Cipla

- 13.4 Gilead Sciences

- 13.5 Glenmark Pharmaceuticals

- 13.6 GlaxoSmithKline

- 13.7 Hikma Pharmaceuticals

- 13.8 Merck & Co.

- 13.9 Novartis AG

- 13.10 Pfizer

- 13.11 Scynexis

- 13.12 Sun Pharmaceutical Industries

- 13.13 Sanofi