PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061435

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061435

Electric Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

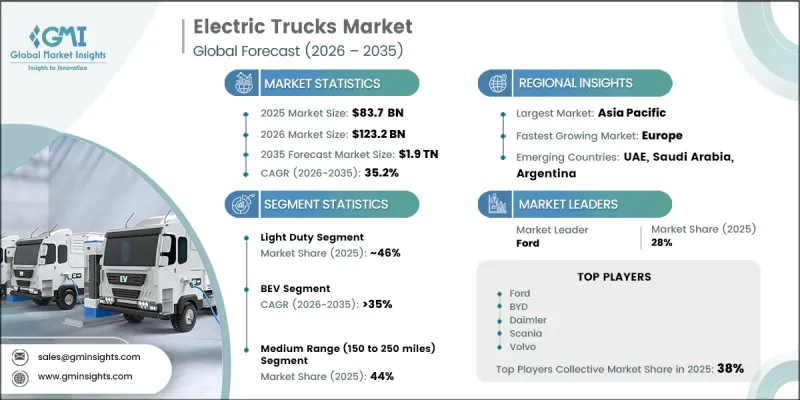

The Global Electric Trucks Market was valued at USD 83.7 billion in 2025 and is estimated to grow at a CAGR of 35.2% to reach USD 1.9 trillion by 2035.

Rapid growth in e-commerce activities and urban delivery operations is significantly accelerating the adoption of electric trucks across global transportation networks. Fleet operators are increasingly transitioning toward battery-electric commercial vehicles to lower fuel expenses, improve delivery efficiency, and comply with tightening emission regulations in urban areas. Electric trucks are gaining strong traction among logistics companies due to their reduced operating and maintenance costs, especially in high-frequency delivery applications across urban and regional transport routes. Continuous advancements in battery technology are also supporting market growth by improving vehicle range, charging speed, and overall reliability. The development of advanced lithium-ion and next-generation solid-state batteries is enabling heavy-duty electric trucks to operate more efficiently over longer distances. In addition, localized manufacturing and economies of scale are helping reduce production costs, making electric commercial vehicles increasingly cost-competitive with conventional diesel-powered alternatives. Strong government incentives, supportive regulatory frameworks, and zero-emission transportation policies across major economies are further accelerating the global adoption of electric trucks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $83.7 Billion |

| Forecast Value | $1.9 Trillion |

| CAGR | 35.2% |

The light-duty segment accounted for 46% share in 2025 and is projected to grow at a CAGR of 34% from 2026 to 2035. Rising demand for fast delivery services and expanding urban logistics operations are driving strong adoption of light-duty electric trucks worldwide. Logistics providers and commercial fleet operators are increasingly deploying compact electric commercial vehicles to improve operational efficiency within urban transportation networks. These vehicles are well-suited for short-distance distribution activities and last-mile delivery operations due to their low emissions, reduced operating expenses, and quieter performance. Growing emphasis on sustainable urban transportation solutions is further supporting segment expansion.

The battery electric vehicle segment held a 75% share in 2025 and is expected to witness growth at a CAGR of 35% through 2035. Increasing regulatory pressure to reduce transportation emissions is significantly accelerating the deployment of battery electric trucks across freight and logistics operations. Governments worldwide are implementing stricter diesel emission regulations while introducing financial incentives and low-emission transportation initiatives to encourage fleet electrification. Battery electric trucks are becoming increasingly attractive for regional freight and city-based transportation applications where sustainability, environmental compliance, and operational efficiency have become critical business priorities.

China Electric Trucks Market held a 56% share and generated USD 25.6 billion in 2025. Strong government support for new energy commercial vehicles continues to drive rapid adoption of electric trucks across the country's logistics and freight transportation sectors. National and regional authorities are introducing purchase incentives, tax benefits, infrastructure funding, and supportive regulatory measures to encourage fleet electrification. In addition, increasingly strict emission standards for diesel-powered commercial vehicles are motivating logistics operators and transportation fleets to transition toward battery-electric trucks across major industrial and urban transport corridors throughout China.

Major companies operating in the Global Electric Trucks Industry include Ford, BYD, Daimler, Volvo, Scania, MAN, PACCAR, Tesla, Foton, and Isuzu. Companies operating in the electric trucks market are adopting several strategic initiatives to strengthen their competitive position and expand their market presence. Industry participants are heavily investing in advanced battery technologies, vehicle electrification platforms, and charging infrastructure development to improve vehicle performance and operational efficiency. Many manufacturers are expanding production capacities and focusing on localized manufacturing strategies to reduce costs and meet rising global demand. Strategic collaborations with logistics providers, battery suppliers, and charging network operators are also helping companies strengthen their distribution capabilities and accelerate commercial adoption. In addition, businesses are introducing connected vehicle technologies, fleet management systems, and energy-efficient powertrain solutions to enhance customer value and operational reliability. Investments in research and development, sustainability initiatives, and expansion into emerging electric mobility markets continue to support long-term growth and stronger market foothold across the global electric trucks industry.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Body

- 2.2.6 End use

- 2.2.7 Battery capacity

- 2.2.8 Range capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent emission regulations and zero-emission mandates

- 3.2.1.2 Rapid expansion of e-commerce and urban logistics

- 3.2.1.3 Advancements in battery technology

- 3.2.1.4 Fleet electrification initiatives by logistics companies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront vehicle costs

- 3.2.2.2 Limited public and depot charging infrastructure

- 3.2.2.3 Battery weight and payload limitations

- 3.2.2.4 Supply chain volatility for battery materials

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of long-haul electric trucking

- 3.2.3.2 Growth in Asia Pacific commercial EV adoption

- 3.2.3.3 Vehicle-to-grid (V2G) integration

- 3.2.3.4 Autonomous and connected fleet technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration

- 3.4.1.3 U.S. Department of Transportation

- 3.4.1.4 California Advanced Clean Trucks (ACT) Regulation

- 3.4.1.5 Canadian Motor Vehicle Safety Standards

- 3.4.2 Europe

- 3.4.2.1 European Union CO2 Emission Standards for Heavy-Duty Vehicles

- 3.4.2.2 EU Battery Regulation

- 3.4.2.3 Alternative Fuels Infrastructure Regulation (AFIR)

- 3.4.2.4 UNECE Vehicle Type Approval Regulations for Electric Commercial Vehicles

- 3.4.2.5 EU General Safety Regulation (GSR)

- 3.4.3 Asia Pacific

- 3.4.3.1 China New Energy Vehicle (NEV) Mandate

- 3.4.3.2 China Compulsory Certification (CCC) for Electric Vehicles

- 3.4.3.3 Indian Central Motor Vehicle Rules (CMVR) for Electric Commercial Vehicles

- 3.4.3.4 Japanese Road Vehicle Act and EV Safety Standards

- 3.4.3.5 Australian Design Rules (ADR) for Electric Heavy Vehicles

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) Electric Vehicle Regulations

- 3.4.4.2 Brazilian National Institute of Metrology (INMETRO) Certification Standards

- 3.4.4.3 Mexican NOM Standards for Electric Commercial Vehicles

- 3.4.4.4 Regional EV Import and Homologation Regulations

- 3.4.4.5 Chile National Electromobility Strategy Regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) Electric Vehicle Standards

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO) EV Regulations

- 3.4.5.3 UAE Federal EV Charging Infrastructure Guidelines

- 3.4.5.4 South African National Road Traffic Act (NRTA) EV Compliance Standards

- 3.4.5.5 African Regional Transport and Emission Compliance Regulations

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Class, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Class 2

- 5.3 Class 3

- 5.4 Class 4

- 5.5 Class 5

- 5.6 Class 6

- 5.7 Class 7

- 5.8 Class 8

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Light duty

- 6.3 Medium duty

- 6.4 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 BEV

- 7.3 PHEV

- 7.4 HEV

- 7.5 FCEV

Chapter 8 Market Estimates & Forecast, By Body, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Pickup

- 8.3 Box / cargo

- 8.4 Flatbed

- 8.5 Dump

- 8.6 Refrigerated

- 8.7 Tanker

- 8.8 Concrete mixer

- 8.9 Refuse

- 8.10 Tow truck

- 8.11 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Construction

- 9.3 Logistics & transportation

- 9.4 Mining

- 9.5 Oil & gas

- 9.6 Municipal services

- 9.7 Agriculture

- 9.8 Defense

- 9.9 Retail & e-commerce

Chapter 10 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 Below 100 kWh

- 10.3 100-300 kWh

- 10.4 Above 300 kWh

Chapter 11 Market Estimates & Forecast, By Range Capacity, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 Short range (Up to 150 miles)

- 11.3 Medium range (150 to 250 miles)

- 11.4 Long range (Over Range 250 miles)

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Southeast Asia

- 12.4.6 ANZ

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Argentina

- 12.5.3 Mexico

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 BYD

- 13.1.2 Daimler Truck

- 13.1.3 Ford

- 13.1.4 Foton

- 13.1.5 Fuso

- 13.1.6 Hyundai Motor

- 13.1.7 Isuzu

- 13.1.8 Nikola

- 13.1.9 PACCAR

- 13.1.10 Volvo Trucks

- 13.2 Regional Players

- 13.2.1 DAF Trucks

- 13.2.2 Einride

- 13.2.3 Iveco

- 13.2.4 MAN Truck

- 13.2.5 Quantron

- 13.2.6 Renault Trucks

- 13.2.7 Scania

- 13.2.8 TATA

- 13.3 Emerging Players

- 13.3.1 Tevva Motors

- 13.3.2 Tesla