PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061451

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061451

Brake Caliper Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

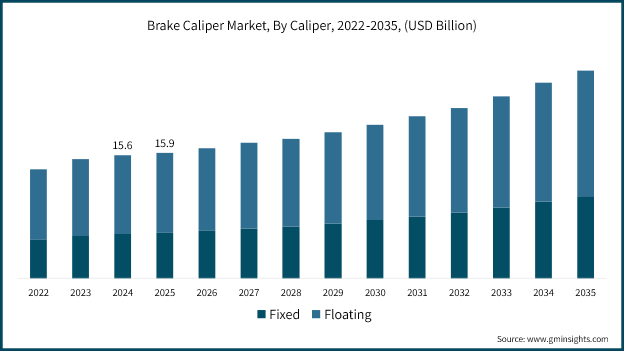

The Global Brake Caliper Market was valued at USD 15.9 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 26.4 billion by 2035.

Growth is driven by expanding global automotive production, rising penetration of electric vehicles that require advanced braking system compatibility, and increasingly stringent vehicle safety regulations mandating integrated braking technologies. The market is also benefiting from structural expansion in vehicle manufacturing across emerging economies, where Asia Pacific continues to evolve into a major production hub for automotive components. Rising vehicle ownership levels in developing regions are further strengthening long-term aftermarket replacement demand, creating a dual-channel growth structure spanning both OEM supply and aftermarket servicing. At the same time, evolving mobility trends and increasing adoption of safety-critical systems are reinforcing the importance of high-performance braking components across vehicle categories. The combination of regulatory compliance requirements, electrification trends, and expanding global vehicle fleets is positioning brake calipers as a critical component category within the broader automotive ecosystem, supporting consistent demand growth across multiple regions and vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.9 Billion |

| Forecast Value | $26.4 Billion |

| CAGR | 5.4% |

The floating brake calipers segment accounted for 63.8% share in 2025, owing to cost efficiency, simplified design architecture, and broad compatibility with high-volume vehicle segments. This configuration is widely used in mass-market passenger cars and light commercial vehicles, where manufacturing scalability and affordability are key priorities. Floating designs operate through a sliding mechanism that enables effective braking force distribution using a single piston system, reducing overall complexity compared to fixed alternatives. Their widespread adoption is supported by ease of production, lower material requirements, and suitability for standard braking performance applications across diverse vehicle platforms.

The passenger car segment represented 66.2% share in 2025 and is projected to grow at a CAGR of 5.8% through 2035. Growth in this segment is supported by rising global passenger vehicle production, particularly across Asia Pacific, along with increasing integration of advanced braking technologies in response to electrification trends. Passenger vehicles range from economy models equipped with cost-effective iron-based floating calipers to premium and performance-oriented vehicles utilizing advanced multi-piston systems and lightweight material configurations. This diversity in design requirements continues to drive innovation and expand application scope within the segment.

North America Brake Caliper Market accounted for 22% share in 2025, supported by a large automotive manufacturing base and a substantial in-use vehicle fleet. The United States maintains annual vehicle production levels of around 10 million units, contributing significantly to both OEM demand and aftermarket replacement cycles. Regulatory frameworks governing braking performance and safety standards further reinforce demand for high-quality, certified brake caliper systems. The regional market is also influenced by a strong preference for light trucks, SUVs, and pickup vehicles, which typically require higher braking capacity and more durable caliper systems compared to smaller passenger vehicles, resulting in increased component value per unit.

Key companies operating in the Global Brake Caliper Market include Bosch, Brembo, Continental, ZF, Akebono, Hitachi Astemo, Aisin, Mando, and Knorr-Bremse. Companies in the brake caliper market are focusing on technological advancement, lightweight material innovation, and integration of high-performance braking solutions to strengthen their market position. Manufacturers are investing in aluminum and composite-based caliper designs to improve efficiency, reduce vehicle weight, and enhance thermal performance. Strategic partnerships with automotive OEMs are enabling the co-development of vehicle-specific braking systems tailored for electric and hybrid platforms. Companies are also expanding production capabilities in emerging automotive manufacturing hubs to optimize supply chain efficiency and reduce operational costs. Increasing investment in research and development is supporting the introduction of advanced multi-piston and electronically controlled braking systems. Additionally, firms are strengthening aftermarket distribution networks and enhancing product availability to capture replacement demand driven by aging vehicle fleets. Focus on regulatory compliance, safety certification, and performance validation continues to play a key role in maintaining long-term competitiveness and market credibility.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Caliper

- 2.2.3 Vehicle

- 2.2.4 Sales Channel

- 2.2.5 Fuel

- 2.2.6 Material

- 2.2.7 Manufacturing Process

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid growth in electric vehicle production & EV-specific caliper requirements

- 3.2.1.2 Increasing vehicle safety standards & regulatory mandates

- 3.2.1.3 Rising consumer demand for high-performance & luxury vehicles

- 3.2.1.4 Expansion of aftermarket due to aging vehicle fleet

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rising raw material costs (aluminum, steel, titanium)

- 3.2.2.2 Presence of low-cost counterfeit products in aftermarket

- 3.2.2.3 Quality & reliability issues with non-OEM components

- 3.2.2.4 High tooling & manufacturing capital requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Development of aluminum metal matrix composites (Al-MMC) for lightweight applications

- 3.2.3.2 Integration of smart sensors & IoT for predictive maintenance

- 3.2.3.3 Adoption of additive manufacturing for performance calipers

- 3.2.3.4 Expansion in emerging markets with growing vehicle production

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Motor Vehicle Safety Standards (FMVSS)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA) Regulations

- 3.4.1.3 Environmental Protection Agency (EPA) Emission & Material Compliance Norms

- 3.4.1.4 Occupational Safety and Health Administration (OSHA) Manufacturing Safety Standards

- 3.4.1.5 U.S. Department of Transportation (DOT) Vehicle Safety & Compliance Standards

- 3.4.2 Europe

- 3.4.2.1 European Union Brake Systems Regulation (UNECE R13 / R13H)

- 3.4.2.2 EU Type Approval Framework for Automotive Components

- 3.4.2.3 REACH Chemical Safety Compliance for Automotive Materials

- 3.4.2.4 EU General Safety Regulation (GSR) for Vehicle Safety Systems

- 3.4.2.5 CE Marking Requirements for Automotive Components

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC) for Automotive Components

- 3.4.3.2 China National Standards (GB Standards) for Brake Systems

- 3.4.3.3 Japan Industrial Standards (JIS) for Automotive Braking Components

- 3.4.3.4 Indian Central Motor Vehicle Rules (CMVR) for Vehicle Safety

- 3.4.3.5 ASEAN Automotive Mutual Recognition Arrangement (ASEAN MRA)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN) Vehicle Safety Regulations

- 3.4.4.2 National Institute of Metrology, Quality and Technology (INMETRO) Certification

- 3.4.4.3 Mexican NOM Vehicle Safety Standards for Brake Systems

- 3.4.4.4 Mercosur Automotive Technical Regulations

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council (GCC) Standardization Organization Automotive Standards

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO) Vehicle Regulations

- 3.4.5.3 South African Bureau of Standards (SABS) Automotive Safety Standards

- 3.4.5.4 National Road Traffic Act (NRTA) Vehicle Compliance Requirements

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Caliper, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Floating

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light-duty

- 6.3.2 Medium-duty

- 6.3.3 Heavy-duty

- 6.4 Two-wheeler

- 6.4.1 Motorcycle

- 6.4.2 Scooters

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 All-electric

- 8.5 PHEV

- 8.6 HEV

- 8.7 FCEV

Chapter 9 Market Estimates & Forecast, By Material, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Aluminum

- 9.3 Steel

- 9.4 Titanium

- 9.5 Phenolics

Chapter 10 Market Estimates & Forecast, By Manufacturing Process, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 High pressure die casting

- 10.3 Gravity die casting

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Southeast Asia

- 11.4.6 ANZ

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Argentina

- 11.5.3 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Aisin

- 12.1.2 Akebono

- 12.1.3 Bosch

- 12.1.4 Brembo

- 12.1.5 Continental

- 12.1.6 Hitachi Astemo

- 12.1.7 Knorr-Bremse

- 12.1.8 Mando

- 12.1.9 ZF

- 12.2 Regional Players

- 12.2.1 Alcon

- 12.2.2 AP Racing

- 12.2.3 Apec Braking

- 12.2.4 ATL Industries

- 12.2.5 Brakes International

- 12.2.6 EBC Brakes

- 12.2.7 Haldex

- 12.2.8 Wilwood

- 12.3 Emerging Players

- 12.3.1 PowerStop

- 12.3.2 Tungaloy Corporation