PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061475

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061475

Robotics actuators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

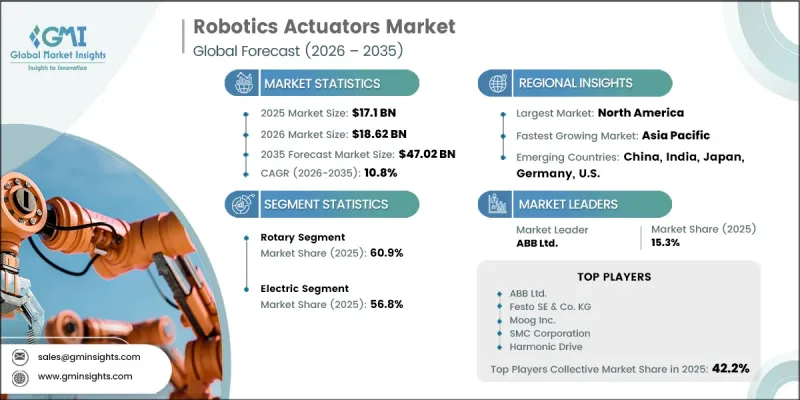

The Global Robotics Actuators Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 47.02 billion by 2035.

The robotics actuators market is witnessing strong expansion due to the accelerating adoption of industrial automation, increasing deployment of collaborative robotic systems, continuous advancements in intelligent actuator technologies, and rising implementation of robotics across healthcare, logistics, and manufacturing environments. Actuators serve as critical components within robotic systems by enabling controlled movement, positioning accuracy, and precise motion execution. As organizations continue to prioritize efficiency, productivity, and operational consistency, demand for advanced robotic motion technologies continues to rise. The growing transition toward automated production facilities, digital manufacturing ecosystems, and connected industrial operations is creating significant opportunities for actuator manufacturers. Furthermore, the increasing need for highly responsive robotic systems capable of performing complex tasks with precision is strengthening market demand. Continuous technological innovation, coupled with expanding investment in next-generation robotics infrastructure, is expected to support sustained growth across the global robotics actuators market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $47.02 Billion |

| CAGR | 10.8% |

The robotics actuators market is driven by the rapid implementation of automation technologies across multiple industrial sectors seeking enhanced productivity, improved operational performance, and reduced dependence on manual labor. Advanced robotic systems have become essential to modern manufacturing environments where precision, repeatability, and reliability are critical requirements. The ongoing evolution of smart factories and digitally connected production facilities is creating a favorable environment for increased adoption of robotics actuators. In addition, growing deployment of collaborative robotic systems and advanced humanoid robotics is generating new growth opportunities across a variety of end-use industries. As businesses continue investing in intelligent automation platforms capable of supporting increasingly sophisticated operational requirements, demand for high-performance actuator technologies is expected to remain strong. The shift toward Industry 4.0 manufacturing models is further accelerating the integration of advanced robotic motion control systems throughout industrial operations.

The rotary segment accounted for 60.9% share in 2025. Its strong market position is supported by widespread adoption across robotic systems requiring rotational motion and high-torque performance. Rotary actuators are extensively utilized in automated manufacturing processes due to their ability to provide precise angular movement, operational durability, and enhanced motion efficiency. Their importance within robotic motion control applications continues to increase as manufacturers pursue greater automation and production optimization. The expanding use of industrial robotics and automated production systems is expected to further strengthen growth within this segment over the coming years.

The electric segment held a share of 56.8% in 2025. Electric actuators have become a preferred solution across robotic platforms due to their superior motion accuracy, energy-efficient operation, and seamless compatibility with digital control architectures. These actuators offer significant advantages, including smooth operational performance, reduced maintenance requirements, and greater adaptability within automated environments. Their suitability for advanced manufacturing facilities and connected production systems continues to support widespread adoption. Growing implementation of robotic technologies across industrial sectors is expected to further accelerate demand for electric actuator solutions throughout the forecast period.

North America Robotics Actuators Market accounted for 32.1% share in 2025. The region continues to experience strong market growth supported by increasing automation investments, advanced manufacturing capabilities, and expanding deployment of robotic technologies across industrial applications. The presence of well-established industrial infrastructure and the ongoing adoption of smart manufacturing initiatives are creating favorable conditions for market expansion. Demand for advanced robotic motion control systems remains strong as organizations focus on improving efficiency, productivity, and operational flexibility. Continuous investments in automated production environments and next-generation robotics technologies are expected to reinforce North America's position as a leading market for robotics actuators throughout the forecast period.

Key companies operating in the Global Robotics Actuators Market include Yaskawa Electric Corporation, ABB Ltd., FANUC Corporation, Harmonic Drive Systems Inc., Nabtesco Corporation, Maxon Motor AG, Sumitomo Heavy Industries, Ltd., Parker Hannifin Corporation, Schaeffler Group, Moog Inc., Festo SE & Co. KG, Oriental Motor Co., Ltd., Technosoft SA, Actuonix Motion Devices Inc., and Firgelli Technologies Inc. Companies participating in the robotics actuators market are adopting a variety of strategic initiatives to strengthen their competitive position and expand market reach. Major industry participants are investing heavily in research and development to improve actuator performance, energy efficiency, precision control, and integration capabilities for advanced robotic systems. Strategic collaborations with robotics manufacturers, automation solution providers, and industrial technology companies are helping organizations broaden their customer base and accelerate product innovation. Companies are also focusing on expanding production capacity, enhancing supply chain resilience, and developing smart actuator technologies that support connected manufacturing environments. Additionally, acquisitions, partnerships, and regional expansion strategies are being utilized to strengthen global presence, improve market penetration, and capture emerging opportunities in rapidly growing automation sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Actuation Type trends

- 2.2.2 Motion Type trends

- 2.2.3 Robot Type trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of industrial automation and smart manufacturing systems

- 3.2.1.2 Growing demand for collaborative robots and humanoid robots

- 3.2.1.3 Technological advancements in smart and AI-enabled actuator systems

- 3.2.1.4 Expansion of healthcare robotics and surgical automation

- 3.2.1.5 Rising warehouse automation and e-commerce logistics applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and integration costs

- 3.2.2.2 Technical complexity and power efficiency limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of robotics in electric vehicle (EV) manufacturing

- 3.2.3.2 Integration with Industry 4.0 and intelligent factory ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Actuation Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Electric

- 5.2.1 Servo Motors

- 5.2.2 Stepper Motors

- 5.2.3 Linear Motors

- 5.2.4 DC Motors

- 5.3 Hydraulic

- 5.3.1 Single-Acting Hydraulic Actuators

- 5.3.2 Double-Acting Hydraulic Actuators

- 5.4 Pneumatic

- 5.4.1 Single-Acting Pneumatic Actuators

- 5.4.2 Double-Acting Pneumatic Actuators

- 5.5 Mechanical

- 5.5.1 Piezoelectric Actuators

- 5.5.2 Shape-Memory Alloy Actuators

- 5.5.3 Magnetic Actuators

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Motion Type, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Rotary

- 6.2.1 Single-Axis Rotary Actuators

- 6.2.2 Multi-Axis Rotary Actuators

- 6.2.3 Others

- 6.3 Linear

- 6.3.1 Electromechanical Linear Actuators

- 6.3.2 Rodless Linear Actuators

- 6.3.3 Belt-Driven Linear Actuators

- 6.3.4 Others

Chapter 7 Market Estimates and Forecast, By Robot Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Industrial Robots

- 7.2.1 Articulated Robots

- 7.2.2 SCARA Robots

- 7.2.3 Delta Robots

- 7.2.4 Cartesian/Gantry Robots

- 7.2.5 Others

- 7.3 Collaborative Robots (Cobots)

- 7.3.1 Professional Service Robots

- 7.3.2 Personal/Domestic Service Robots

- 7.3.3 Medical & Healthcare Robots

- 7.3.4 Others

- 7.4 Humanoid Robots

- 7.4.1 Research & Development Humanoids

- 7.4.2 Commercial & Entertainment Humanoids

- 7.4.3 Others

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Automotive

- 8.2.1 Assembly & Fabrication

- 8.2.2 Welding & Joining

- 8.2.3 Painting & Coating

- 8.2.4 Others

- 8.3 Packaging

- 8.3.1 Food & Beverages

- 8.3.2 Processing & Sorting

- 8.3.3 Packaging & Palletizing

- 8.3.4 Others

- 8.4 Metal & Machinery

- 8.4.1 Machining & Cutting

- 8.4.2 Casting & Forging

- 8.4.3 Others

- 8.5 Healthcare & Medical

- 8.5.1 Surgical Robotics

- 8.5.2 Rehabilitation & Prosthetics

- 8.5.3 Laboratory Automation

- 8.5.4 Others

- 8.6 Chemicals & Materials

- 8.6.1 Batch Processing

- 8.6.2 Material Handling & Mixing

- 8.6.3 Others

- 8.7 Logistics & Warehousing

- 8.7.1 Automated Guided Vehicles (AGVs)

- 8.7.2 Sorting & Distribution Systems

- 8.7.3 Pick & Place Operations

- 8.7.4 Others

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 ABB Ltd

- 10.1.2 Festo SE & Co. KG

- 10.1.3 Moog Inc.

- 10.1.4 SMC Corporation

- 10.1.5 Harmonic Drive Systems Inc.

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Parker Hannifin Corporation

- 10.2.1.2 Actuonix Motion Devices Inc.

- 10.2.1.3 Firgelli Technologies Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Nabtesco Corporation

- 10.2.2.2 Yaskawa Electric Corporation

- 10.2.3 Europe

- 10.2.3.1 Schaeffler Group

- 10.2.3.2 Technosoft SA

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Technosoft SA

- 10.3.2 Oriental Motor Co, Ltd.