PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061478

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061478

Armored Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

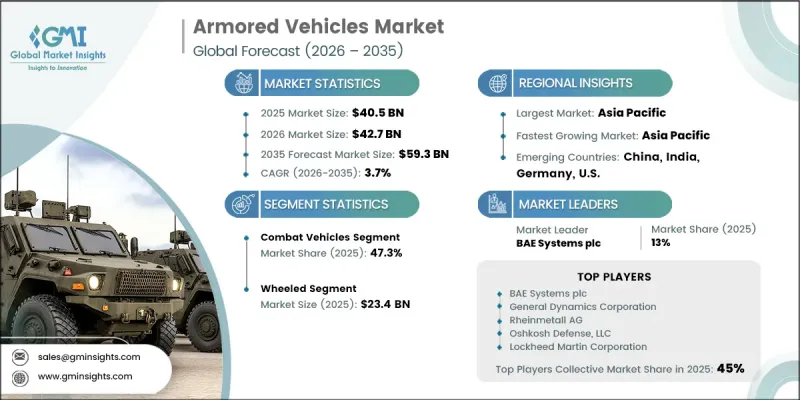

The Global Armored Vehicles Market was valued at USD 40.5 billion in 2025 and is estimated to grow at a CAGR of 3.7% to reach USD 59.3 billion by 2035.

Market expansion is being supported by rising defense preparedness amid geopolitical uncertainties, increasing investment in capability enhancement programs, and a stronger focus on internal security operations and asymmetric warfare threats. Demand is also strengthening as armored platforms are increasingly deployed beyond traditional military roles into internal protection and specialized security missions. Additionally, the need for highly protected mobility solutions in challenging and hostile terrains continues to reinforce procurement activity across defense forces globally. Ongoing fleet replacement programs, combined with modernization initiatives, are further accelerating the adoption of next-generation armored platforms designed for improved survivability, mobility, and mission versatility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $40.5 Billion |

| Forecast Value | $59.3 Billion |

| CAGR | 3.7% |

The armored vehicles market is fueled by rising conflict intensity and persistent security threats, which are prompting governments to significantly raise defense allocations to safeguard ground forces. As regional conflicts intensify across multiple geographies, defense agencies are channeling higher investments into land-based combat systems to enhance troop protection and battlefield effectiveness. At the same time, government-led modernization initiatives are reshaping procurement priorities, with increased focus on replacing aging fleets and upgrading operational capabilities. These modernization programs emphasize improved protection systems, enhanced maneuverability, and higher combat readiness standards. Rising threat perceptions are further compelling governments to allocate larger capital budgets toward strengthening armored mobility infrastructure. As a result, sustained investment in fleet renewal and defense upgrades is playing a central role in driving long-term market expansion.

The unmanned armored ground vehicles segment is projected to grow at a CAGR of 10.1% during 2026 to 2035. Rising efforts to reduce battlefield risk for personnel and improve mission efficiency are accelerating the adoption of autonomous and remotely operated ground systems. Continuous advancements in artificial intelligence, sensor technologies, and command and control architectures are further strengthening the development and deployment of these unmanned platforms.

The tracked segment is expected to grow at a CAGR of 2.7% through 2035. Demand for these platforms is supported by their ability to operate effectively in difficult terrain and high-intensity combat environments. Their superior load-bearing capacity, enhanced protection levels, and strong battlefield stability make them highly suitable for frontline combat missions, thereby sustaining steady adoption across defense forces.

North America Armored Vehicles Market accounted for a 33.5% share in 2025. The region's growth is driven by continuous investment in modernization programs, capability upgrades, and readiness enhancement across land-based defense systems. Strong emphasis on operational mobility, survivability, and interoperability is sustaining demand for advanced armored platforms across multiple mission categories. Growth is further reinforced by a well-established defense manufacturing base and ongoing efforts to integrate advanced technologies into next-generation military vehicles.

Key companies operating in the Global Armored Vehicles Industry include Rheinmetall AG, General Dynamics Corporation, BAE Systems plc, Oshkosh Defense, LLC, Lockheed Martin Corporation, Hyundai Rotem Company, Hanwha Defense, KNDS (Krauss-Maffei Wegmann & Nexter Group), Iveco Defense Vehicles, Tata Advanced Systems Limited, Denel Vehicle Systems, NIMR Automotive LLC, Milrem Robotics, Arquus, Paramount Group, and ST Engineering Land Systems. Companies in the armored vehicles market are actively focusing on technological modernization, integrating advanced protection systems, AI-enabled situational awareness tools, and next-generation mobility platforms to enhance battlefield performance. They are strengthening partnerships with defense agencies to align product development with evolving military requirements and procurement standards. Manufacturers are also investing in unmanned and hybrid vehicle technologies to reduce troop exposure and improve operational efficiency. Expansion of domestic production capabilities and localization strategies is helping firms meet sovereign defense requirements while reducing supply chain risks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform trends

- 2.2.2 Mobility trends

- 2.2.3 Propulsion trends

- 2.2.4 Solution type trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Escalating security threats and geopolitical conflicts

- 3.2.1.2 Rising government investments in defense modernization programs

- 3.2.1.3 Expansion of counter-terrorism and internal security operations

- 3.2.1.4 Growing need for commercial armored vehicles

- 3.2.1.5 Rising Urban Combat and Security Operations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High acquisition and lifecycle costs of armored vehicles

- 3.2.2.2 Complex procurement and long development cycles

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of autonomous and optionally manned armored vehicle technologies

- 3.2.3.2 Increasing focus on lightweight materials and mobility optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Combat vehicles

- 5.3 Combat support vehicles

- 5.4 Unmanned armored ground vehicles

- 5.5 Civilian/commercial armored vehicles

Chapter 6 Market Estimates and Forecast, By Mobility, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Wheeled

- 6.3 Tracked

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Propulsion, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Hybrid

- 7.4 Electric

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Solution Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Line Fit/OEM

- 8.3 Retrofit

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 BAE Systems plc

- 10.1.2 General Dynamics Corporation

- 10.1.3 Rheinmetall AG

- 10.1.4 Oshkosh Defense, LLC

- 10.1.5 Lockheed Martin Corporation

- 10.2 Regional key players

- 10.2.1 Asia Pacific

- 10.2.1.1 Hanwha Defense

- 10.2.1.2 Hyundai Rotem Company

- 10.2.1.3 Tata Advanced Systems Limited

- 10.2.1.4 ST Engineering Land Systems

- 10.2.2 Europe

- 10.2.2.1 KNDS (Krauss-Maffei Wegmann & Nexter Group)

- 10.2.2.2 Iveco Defense Vehicles

- 10.2.2.3 Arquus

- 10.2.3 Middle East & Africa

- 10.2.3.1 NIMR Automotive LLC

- 10.2.3.2 Denel Vehicle Systems

- 10.2.3.3 Paramount Group

- 10.2.1 Asia Pacific

- 10.3 Niche Players/Disruptors

- 10.3.1 Milrem Robotics