PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061479

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061479

Fuel Cell UAV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

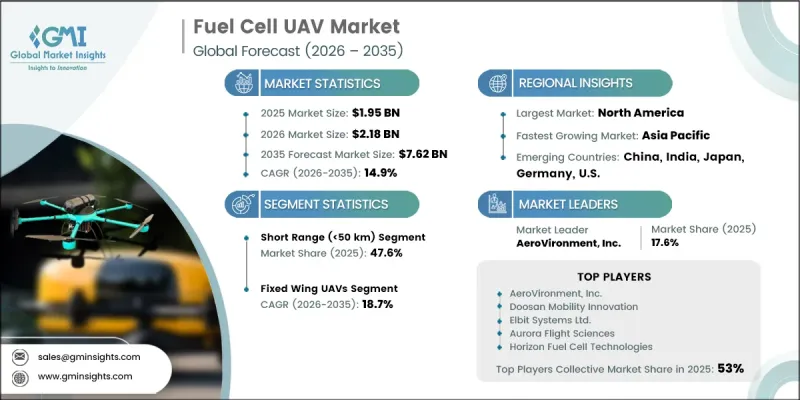

The Global Fuel Cell UAV Market was valued at USD 1.95 billion in 2025 and is estimated to grow at a CAGR of 14.9% to reach USD 7.62 billion by 2035.

Growth in this market is driven by rising demand for long-endurance unmanned aerial systems, increasing defense spending across major economies, continuous advancements in hydrogen fuel cell technologies, and the widening scope of commercial UAV applications. Fuel cell powered drones are gaining strong traction across surveillance, mapping, inspection, reconnaissance, and logistics-related missions due to their ability to deliver significantly longer flight durations compared to conventional battery powered systems. The shift toward more efficient and persistent aerial platforms is also being reinforced by the need for reduced operational downtime and improved mission efficiency. In addition, governments and defense organizations are increasingly investing in next-generation unmanned systems to enhance situational awareness, border monitoring, and intelligence capabilities. Ongoing technological innovation in hydrogen storage, energy density improvement, and lightweight system integration is further strengthening adoption. The growing integration of UAVs into industrial workflows, combined with the demand for high-performance aerial systems capable of sustained operations, continues to accelerate market expansion globally. These combined factors are positioning fuel cell UAVs as a critical technology within the evolving unmanned aerial ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.95 Billion |

| Forecast Value | $7.62 Billion |

| CAGR | 14.9% |

The fuel cell UAV market is also witnessing strong momentum due to the superior endurance, operational efficiency, and energy advantages offered by hydrogen-based propulsion systems. These platforms significantly reduce downtime by enabling faster refueling compared to battery charging cycles, which improves mission continuity and operational readiness. As organizations increasingly prioritize long-range, high-persistence aerial capabilities, fuel cell UAVs are becoming a preferred solution for both defense and commercial applications. Continuous improvements in system integration and energy optimization are further enhancing performance and reliability, strengthening long-term adoption prospects across multiple sectors.

The short-range (below 50 km) segment accounted for 47.6% share in 2025, driven by strong utilization across inspection activities, agricultural monitoring, infrastructure assessment, and localized surveillance missions. These UAVs are widely preferred due to their cost efficiency, simplified operational requirements, and suitability for short-distance missions. Their expanding use across commercial and industrial applications continues to support steady demand growth within this segment.

The fixed wing UAV segment held a 48.6% share and is projected to grow at a CAGR of 18.7% during 2026-2035. This dominance is supported by increasing demand for long-duration aerial operations, including surveillance, reconnaissance, mapping, and security monitoring activities. Fixed-wing platforms offer extended flight endurance, enhanced energy efficiency, and broader coverage capabilities compared to other UAV types. Growing defense modernization initiatives and the expanding use of UAVs in industrial operations are further reinforcing segment growth.

North America Fuel Cell UAV Market held a 35% share in 2025. Market expansion in the region is driven by rising investments in defense modernization programs, increased adoption of advanced unmanned aerial systems across industrial sectors, and strong demand for long-endurance drone capabilities. The presence of a well-established aerospace ecosystem, combined with continuous technological innovation and rapid integration of autonomous UAV solutions, is further supporting regional market growth.

Key companies operating in the Global Fuel Cell UAV Industry include AeroVironment, Inc., Doosan Mobility Innovation, Elbit Systems Ltd., Aurora Flight Sciences, Horizon Fuel Cell Technologies, ISS Aerospace, Israel Aerospace Industries (IAI), Lockheed Martin Corporation, The Boeing Company, Northrop Grumman Corporation, Textron Inc., General Dynamics Corporation, Plug Power Inc., Ballard Power Systems Inc., and H3 Dynamics Holdings Pte. Ltd. Companies operating in the fuel cell UAV market are adopting several strategic initiatives to strengthen their market position and expand their technological capabilities. A major focus is placed on research and development to improve hydrogen fuel efficiency, extend flight endurance, and enhance payload capacity. Firms are also investing in lightweight materials and advanced propulsion systems to improve overall UAV performance. Strategic collaborations with defense agencies, aerospace manufacturers, and energy technology providers are helping accelerate commercialization and expand application areas. Many players are also scaling production capabilities and strengthening supply chains to support growing demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Range trends

- 2.2.2 UAV type trends

- 2.2.3 Power System Type trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for long-endurance UAV operations

- 3.2.1.2 Rising defense and military investments in advanced UAV technologies

- 3.2.1.3 Technological advancements in hydrogen fuel cell systems

- 3.2.1.4 Growing adoption of sustainable and zero-emission aviation solutions

- 3.2.1.5 Expansion of commercial UAV applications across industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and hydrogen storage costs

- 3.2.2.2 Technical and regulatory challenges in hydrogen-powered UAV deployment

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of UAVs in logistics and cargo delivery

- 3.2.3.2 Expansion of hydrogen economy and clean energy investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By UAV Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Fixed Wing UAVs

- 5.2.1 Micro UAVs (<5 kg payload)

- 5.2.2 Small UAVs (5-25 kg payload)

- 5.2.3 Medium UAVs (25-150 kg payload)

- 5.3 Rotary Wing UAVs

- 5.3.1 Quadcopter/Multirotor (<15 kg payload)

- 5.3.2 Single Rotor (15-50 kg payload)

- 5.3.3 Heavy Lift (>50 kg payload)

- 5.4 Hybrid VTOL UAVs

- 5.4.1 Light VTOL (<10 kg payload)

- 5.4.2 Heavy VTOL (>10 kg payload)

Chapter 6 Market Estimates and Forecast, By Range, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Short Range (<50 km)

- 6.3 Medium Range (50-200 km)

- 6.4 Long Range (>200 km)

Chapter 7 Market Estimates and Forecast, By Power System Type, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Hydrogen Fuel Cell Systems

- 7.2.1 PEM Fuel Cell

- 7.2.2 SOFC

- 7.2.3 Hybrid (Fuel Cell + Battery)

- 7.3 Battery-Electric Systems

- 7.3.1 Lithium-Ion (Li-ion)

- 7.3.2 Lithium-Polymer (LiPo)

- 7.3.3 Others

Chapter 8 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Military & Defense

- 8.2.1 Intelligence, Surveillance & Reconnaissance (ISR)

- 8.2.2 Training & Target Practice

- 8.2.3 Electronic Warfare & Communications Relay

- 8.2.4 Search & Rescue (SAR) Operations

- 8.2.5 Others

- 8.3 Commercial & Industrial

- 8.3.1 Security & Perimeter Surveillance

- 8.3.1.1 Critical Infrastructure Security

- 8.3.1.2 Industrial Site Perimeter Monitoring

- 8.3.1.3 Event & Crowd Surveillance

- 8.3.1.4 Others

- 8.3.2 Aerial Mapping & Surveying

- 8.3.2.1 Topographic & Cadastral Mapping

- 8.3.2.2 Mining & Quarrying Site Mapping

- 8.3.2.3 Urban Planning & Smart City Applications

- 8.3.2.4 Others

- 8.3.3 Asset Inspection & Maintenance

- 8.3.3.1 Oil & Gas Infrastructure

- 8.3.3.2 Renewable Energy Assets

- 8.3.3.3 Telecom Infrastructure

- 8.3.3.4 Others

- 8.3.4 Delivery & Logistics

- 8.3.4.1 Medical & Pharmaceutical Delivery

- 8.3.4.2 E-commerce Last-Mile Delivery

- 8.3.4.3 Industrial Parts & Tools Delivery

- 8.3.4.4 Others

- 8.3.5 Agricultural Applications

- 8.3.5.1 Pesticide & Fertilizer Spraying

- 8.3.5.2 Crop Health Monitoring & Disease Detection

- 8.3.5.3 Precision Agriculture & Soil Analysis

- 8.3.5.4 Others

- 8.3.6 Environmental Monitoring

- 8.3.6.1 Air Quality & Pollution Monitoring

- 8.3.6.2 Disaster Response & Damage Assessment

- 8.3.6.3 Others

- 8.3.7 Others

- 8.3.1 Security & Perimeter Surveillance

- 8.4 Civil/Government

- 8.4.1 Public Safety & Emergency Response

- 8.4.2 Traffic Monitoring & Management

- 8.4.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 AeroVironment, Inc.

- 10.1.2 Doosan Mobility Innovation

- 10.1.3 Elbit Systems Ltd.

- 10.1.4 Aurora Flight Sciences

- 10.1.5 Horizon Fuel Cell Technologies

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 Lockheed Martin Corporation

- 10.2.1.2 The Boeing Company

- 10.2.1.3 Northrop Grumman Corporation

- 10.2.1.4 Textron Inc.

- 10.2.2 Asia Pacific

- 10.2.2.1 Doosan Mobility Innovation

- 10.2.2.2 H3 Dynamics Holdings Pte. Ltd.

- 10.2.2.3 Horizon Fuel Cell Technologies

- 10.2.3 Europe

- 10.2.3.1 ISS Aerospace

- 10.2.3.2 Elbit Systems Ltd.

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 Plug Power Inc.

- 10.3.2 Ballard Power Systems Inc.