PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071174

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071174

Railway Traction Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

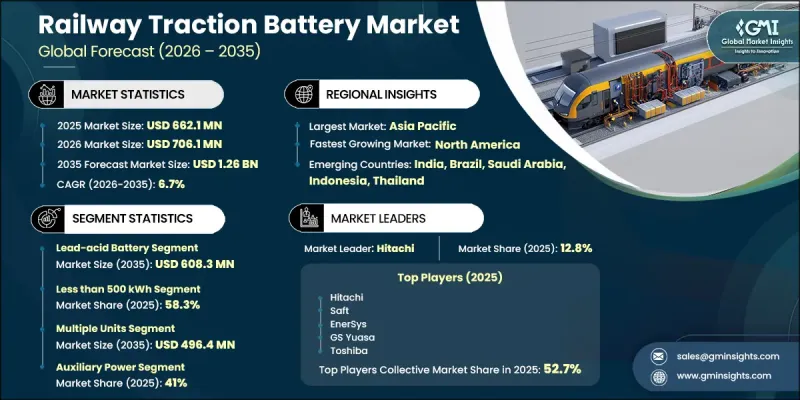

The Global Railway Traction Battery Market was valued at USD 662.1 million in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 1.26 billion by 2035.

Market growth is driven by the increasing adoption of advanced energy storage technologies across modern rail transportation systems. Demand is expanding beyond traditional battery applications as railway operators increasingly utilize onboard energy storage solutions for traction support, regenerative energy recovery, backup propulsion, and energy efficiency optimization. One of the most significant developments shaping the industry is the gradual transition from conventional low-cost battery technologies toward higher-value lithium-ion systems that offer improved performance, longer operational life, and enhanced energy density. Regulatory initiatives focused on reducing transportation emissions and improving sustainability are encouraging rail operators to modernize existing fleets and invest in cleaner propulsion technologies. Battery-assisted rail systems provide a practical solution for enhancing operational efficiency while reducing environmental impact. In addition, energy storage systems capable of recovering and reusing braking energy are helping operators lower overall power consumption, creating long-term demand for advanced railway traction battery solutions across passenger rail, urban transit networks, and locomotive applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $662.1 Million |

| Forecast Value | $1.26 Billion |

| CAGR | 6.7% |

The lead-acid battery segment accounted for USD 358.9 million in 2025, representing 54.2% share. Despite the increasing adoption of newer battery technologies, lead-acid batteries continue to maintain a significant market share due to their cost-effectiveness, established supply chains, proven operational reliability, and widespread recycling infrastructure. Many rail operators continue to rely on these systems for auxiliary power requirements and replacement applications because of their familiarity with maintenance practices and predictable performance characteristics.

The less than 500 kWh capacity segment generated USD 386.2 million in 2025 and accounted for 58.3% share. This segment serves a broad range of railway applications that require battery systems for auxiliary functions, safety systems, and operational support. The extensive deployment across multiple rolling stock categories continues to provide a strong and stable demand base. The widespread need for battery-powered support systems throughout rail operations remains a key factor supporting segment growth.

North America Railway Traction Battery Market generated USD 123 million in 2025 and is forecast to reach USD 309.5 million by 2035, expanding at a CAGR of 9.6%. Growth in the region is supported by increasing investments in railway modernization, transportation electrification, and sustainable mobility infrastructure. Ongoing upgrades to rail networks, fleet replacement programs, and the adoption of energy-efficient transportation technologies are creating favorable opportunities for advanced battery systems. Rising emphasis on reducing emissions and improving operational performance continues to strengthen demand for traction battery solutions throughout the North American rail sector.

Major companies operating in the global railway traction battery market include Hitachi, Saft Groupe, ABB, EnerSys, HOPPECKE Batterien, Toshiba, Leclanche, GS Yuasa, BorgWarner AKASOL, and Forsee Power. Companies operating in the railway traction battery market are implementing a variety of strategies to strengthen their market position and enhance long-term growth prospects. Leading manufacturers are increasing investments in research and development to improve battery performance, energy density, safety, and lifecycle efficiency. Product innovation remains a primary focus, particularly in advanced lithium-ion technologies and next-generation energy storage solutions. Strategic collaborations with railway operators, transportation authorities, and system integrators are helping companies expand their customer base and accelerate technology adoption. Many market participants are also investing in manufacturing capacity expansion and supply chain optimization to meet growing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Chemistry

- 2.2.3 Application

- 2.2.4 Rolling Stock

- 2.2.5 Battery Capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising government investments in railway electrification and sustainable transportation

- 3.2.1.2 Stringent environmental regulations and decarbonization targets

- 3.2.1.3 Expansion of metro, regional, and high-speed rail networks

- 3.2.1.4 Growing focus on operational efficiency and regenerative braking

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront costs of batteries, retrofitting, and charging infrastructure

- 3.2.2.2 Limited battery range and performance for long-distance and heavy-haul operations

- 3.2.3 Market opportunities

- 3.2.3.1 Accelerated deployment of battery-electric multiple units on non-electrified routes

- 3.2.3.2 Integration of wayside energy storage systems with on-board batteries

- 3.2.3.3 Predictive maintenance and AI-driven battery health monitoring

- 3.2.3.4 Circular economy and second-life battery programs for railway applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 United States Environmental Protection Agency (EPA) - Battery Recycling and Hazardous Waste Management Regulations

- 3.5.1.2 United States Department of Energy (DOE) - Battery Lifecycle Management and Circular Economy Initiatives

- 3.5.1.3 United States Department of Transportation (USDOT) - Transportation and Handling Standards for Lithium-Ion Batteries

- 3.5.1.4 Environment and Climate Change Canada (ECCC) - Battery Recycling and Extended Producer Responsibility (EPR) Programs

- 3.5.2 Europe

- 3.5.2.1 Germany - Federal Battery Act (BattG) and Extended Producer Responsibility (EPR) Requirements

- 3.5.2.2 France - Anti-Waste and Circular Economy Law (AGEC) and Battery Collection Regulations

- 3.5.2.3 United Kingdom - Waste Batteries and Accumulators Regulations and Producer Compliance Schemes

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Ministry of Industry and Information Technology (MIIT) - New Energy Vehicle Battery Recycling Regulations

- 3.5.3.2 Japan Ministry of Economy, Trade and Industry (METI) - Battery Resource Circulation and Recycling Policies

- 3.5.3.3 India Ministry of Environment, Forest and Climate Change (MoEFCC) - Battery Waste Management Rules, 2022

- 3.5.3.4 Australia Department of Climate Change, Energy, the Environment and Water (DCCEEW) - Battery Stewardship and Recycling Framework

- 3.5.4 Latin America

- 3.5.4.1 Brazil National Solid Waste Policy (PNRS) - Battery Collection and Reverse Logistics Requirements

- 3.5.4.2 Mexico Ministry of Environment and Natural Resources (SEMARNAT) - Hazardous Battery Waste Management Regulations

- 3.5.5 Middle East & Africa

- 3.5.5.1 GCC Environmental Regulatory Frameworks for Battery Disposal, Recycling, and Circular Economy Development

- 3.5.5.2 South Africa National Environmental Management: Waste Act (NEMWA) - Battery Waste and Recycling Regulations

- 3.5.5.3 UAE Circular Economy Policy and Waste Management Regulations for Battery Reuse and Recycling Industries

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade data analysis (Driven by Paid Research)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Capacity & production landscape (Driven by Primary Research)

- 3.11.1 Installed capacity by region & key producer

- 3.11.2 Capacity utilization rates & expansion pipelines

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 Automated design optimization

- 3.12.3 Supply chain AI for demand forecasting

- 3.12.4 GenAI use cases & adoption roadmap by segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Battery Chemistry, 2022 - 2035 ($Mn, Unit)

- 5.1 Key trends

- 5.2 Lead-Acid Battery

- 5.3 Lithium-Ion Battery

- 5.4 Nickel-Cadmium (Ni-Cd) Battery

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Traction & Propulsion

- 6.3 Starter & Cranking

- 6.4 Auxiliary Power

Chapter 7 Market Estimates & Forecast, By Rolling Stock, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Locomotives

- 7.3 Multiple Units (MUs)

- 7.4 Metro / Light Rail / Tram

- 7.5 Passenger Coaches & Freight Wagons

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Less than 500 kWh

- 8.3 500 kWh - 1 MWh

- 8.4 1 MWh - 5 MWh

- 8.5 Above 5 MWh

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 9.1 North America

- 9.1.1 US

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Belgium

- 9.2.7 Netherlands

- 9.2.8 Sweden

- 9.2.9 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 Singapore

- 9.3.6 South Korea

- 9.3.7 Vietnam

- 9.3.8 Indonesia

- 9.3.9 Thailand

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Saft Groupe

- 10.1.2 ABB

- 10.1.3 EnerSys

- 10.1.4 HOPPECKE

- 10.1.5 Toshiba

- 10.1.6 Hitachi

- 10.1.7 Leclanche

- 10.1.8 GS Yuasa

- 10.1.9 BorgWarner AKASOL

- 10.1.10 Forsee Power

- 10.2 Regional Players

- 10.2.1 Exide

- 10.2.2 Amara Raja

- 10.2.3 HBL Engineering

- 10.2.4 Shuangdeng

- 10.2.5 East Penn

- 10.2.6 SEC Battery

- 10.2.7 Turntide

- 10.2.8 BYD

- 10.2.9 CATL

- 10.2.10 Kokam