PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071266

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071266

Vehicle Wireless Connectivity Modules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

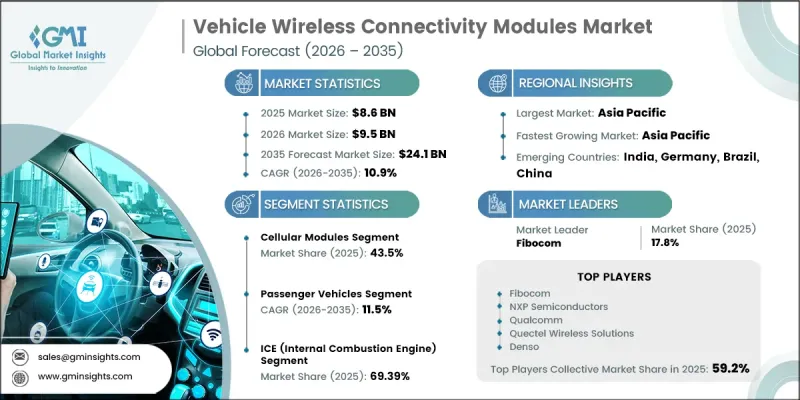

The Global Vehicle Wireless Connectivity Modules (VWCM) Market was valued at USD 8.6 billion in 2025 and is estimated to grow at a CAGR of 10.9% to reach USD 24.1 billion by 2035.

Market is experiencing rapid evolution, driven by the growing demand for intelligent, connected mobility solutions. This growth reflects a major shift in the role of connectivity modules, transitioning from basic telematics support to becoming a central communication backbone for next-generation vehicles. Modern automotive systems increasingly rely on seamless data exchange across multiple domains, supporting software-defined vehicles, advanced mobility ecosystems, and integrated transportation networks. The rising adoption of 5G connectivity, expansion of vehicle-to-everything communication technologies, and increasing integration of cloud-enabled electric vehicles are accelerating this transformation. These modules now play a critical role in enabling real-time communication, over-the-air updates, enhanced infotainment, fleet management, and advanced driver assistance systems, supporting both operational efficiency and safety applications across global automotive platforms.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.6 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 10.9% |

Regulatory frameworks and industry initiatives are playing a vital role in accelerating the deployment of VWCM technologies across key automotive regions. In Europe, evolving policy structures and compliance requirements are encouraging automakers to integrate embedded connectivity solutions more deeply into vehicle architectures. These regulatory efforts are strengthening the adoption of advanced communication systems that support vehicle safety, diagnostics, and electric vehicle interaction capabilities.

Cellular connectivity modules accounted for 43.5% share in 2025 and is expected to grow at a CAGR of 12.1% between 2026 and 2035. These modules serve as the primary communication layer within modern vehicles, enabling continuous interaction between vehicles, cloud environments, and external digital networks. Their functionality extends across telematics services, software updates, diagnostics, infotainment systems, and increasingly complex driver assistance technologies. As the automotive industry moves toward software-defined architectures, manufacturers are prioritizing the integration of high-speed 5G-enabled modules to support low-latency communication, edge processing, and high-volume data transmission.

The passenger vehicles segment held a 73.1% share in 2025 and are forecast to grow at a CAGR of 11.5% from 2026 to 2035. This segment continues to generate the highest revenue due to widespread adoption of diverse connectivity technologies, including cellular, Wi-Fi, Bluetooth, and other advanced communication modules. Modern passenger vehicles are being equipped with sophisticated digital systems that enable continuous connectivity and real-time data exchange. The rapid growth of electric vehicles further amplifies demand, as these platforms depend heavily on persistent connectivity for energy management, charging coordination, navigation, and remote monitoring functionalities.

China Vehicle Wireless Connectivity Modules (VWCM) Market generated USD 1.8 billion in 2025. The country's dominance is supported by strong government-backed initiatives aimed at advancing intelligent connected vehicle ecosystems and expanding nationwide smart mobility infrastructure. Large-scale deployment of advanced communication technologies across transportation networks has positioned China as a key market, driving innovation and adoption of next-generation vehicle connectivity solutions.

Key companies operating in the Vehicle Wireless Connectivity Modules market include Fibocom, NXP Semiconductors, Qualcomm, Quectel Wireless Solutions, Denso, Continental, Robert Bosch, ZF Friedrichshafen, Aptiv, and Harman International. Companies in the Vehicle Wireless Connectivity Modules market are focusing on strategic innovation, partnerships, and technology integration to strengthen their market position. Leading players are investing heavily in research and development to advance 5G-enabled modules, edge computing capabilities, and high-speed data communication solutions. Collaborations with automotive manufacturers and technology providers are enabling faster deployment of integrated connectivity systems. Firms are also expanding their product portfolios to support software-defined vehicle architectures and cloud-based platforms.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Connectivity Technology

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for connected vehicles

- 3.2.1.2 Growth of V2X and ADAS technologies

- 3.2.1.3 Expansion of 5G infrastructure

- 3.2.1.4 Regulatory push for vehicle safety and telematics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of integration and hardware complexity

- 3.2.2.2 Cybersecurity and data privacy risks

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of autonomous and semi-autonomous vehicles

- 3.2.3.2 Aftermarket and fleet telematics expansion

- 3.2.3.3 OEM-tech company partnerships for connectivity ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.6.1.2 Federal Communications Commission (FCC)

- 3.6.1.3 U.S. Department of Transportation (USDOT)

- 3.6.1.4 Federal Trade Commission (FTC) Data Privacy Regulations

- 3.6.1.5 ISO/SAE 21434 Cybersecurity Standard

- 3.6.2 Europe

- 3.6.2.1 UNECE WP.29 (R155 & R156)

- 3.6.2.2 General Data Protection Regulation (GDPR)

- 3.6.2.3 EU Data Act

- 3.6.2.4 European Union General Safety Regulation (GSR)

- 3.6.2.5 ISO 26262 Functional Safety Standard

- 3.6.3 Asia Pacific

- 3.6.3.1 China Cybersecurity Law

- 3.6.3.2 China Data Security Law

- 3.6.3.3 Personal Information Protection Law (PIPL)

- 3.6.3.4 Japan Automotive Cybersecurity Guidelines / Mobility Safety Frameworks

- 3.6.3.5 India Automotive Mission Plan (AMP)

- 3.6.4 Latin America

- 3.6.4.1 Brazil General Data Protection Law (LGPD)

- 3.6.4.2 Mexico Automotive Digitalization & Data Governance Regulations

- 3.6.4.3 MERCOSUR Digital Integration Framework

- 3.6.4.4 Chile Smart Mobility Policies

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE Artificial Intelligence Strategy & Data Regulations

- 3.6.5.2 Saudi Data & Artificial Intelligence Authority (SDAIA) Regulations

- 3.6.5.3 GCC Digital Economy & Smart Mobility Framework

- 3.6.5.4 African Union Digital Transformation Strategy

- 3.6.5.5 African Continental Free Trade Area (AfCFTA) Digital Protocol

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI and Generative AI on the Market

- 3.12.1 AI Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.12.3 Risks Limitations and Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Connectivity Technology, 2022 - 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Cellular Modules

- 5.2.1 4G LTE

- 5.2.2 5G NR

- 5.3 Wi-Fi Modules

- 5.3.1 Wi-Fi 5

- 5.3.2 Wi-Fi 6 & 6E

- 5.4 Bluetooth / BLE Modules

- 5.5 V2X Modules

- 5.6 UWB Modules

- 5.7 Satellite Connectivity Modules

- 5.7.1 LEO

- 5.7.2 GEO

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 ICE (Internal Combustion Engine)

- 7.3 Electric Vehicles

- 7.3.1 Battery Electric Vehicles

- 7.3.2 Plug-in Hybrid Electric Vehicles

- 7.3.3 Hybrid Electric Vehicles

- 7.3.4 Fuel Cell Electric Vehicles

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Telematics & Fleet Management

- 8.3 In-Vehicle Infotainment (IVI)

- 8.4 ADAS & Autonomous Driving Connectivity

- 8.5 Safety & Emergency Services (eCall / crash alerts)

- 8.6 OTA Software Management (updates, lifecycle control)

- 8.7 Navigation & Positioning Services

- 8.8 Vehicle Access & Smart Control

- 8.9 Energy & Battery Management (EV/BMS)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Norway

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Qualcomm

- 11.1.2 NXP Semiconductors

- 11.1.3 Intel

- 11.1.4 Broadcom

- 11.1.5 Texas Instruments

- 11.1.6 Quectel Wireless Solutions

- 11.1.7 Fibocom

- 11.1.8 Telit Cinterion

- 11.1.9 u-blox

- 11.1.10 Thales

- 11.1.11 Robert Bosch

- 11.1.12 Continental

- 11.1.13 Aptiv

- 11.1.14 Harman International

- 11.2 Regional Players

- 11.2.1 Denso

- 11.2.2 Valeo

- 11.2.3 ZF Friedrichshafen

- 11.2.4 Tesla

- 11.2.5 BMW

- 11.2.6 General Motors