PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071278

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071278

Anime Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

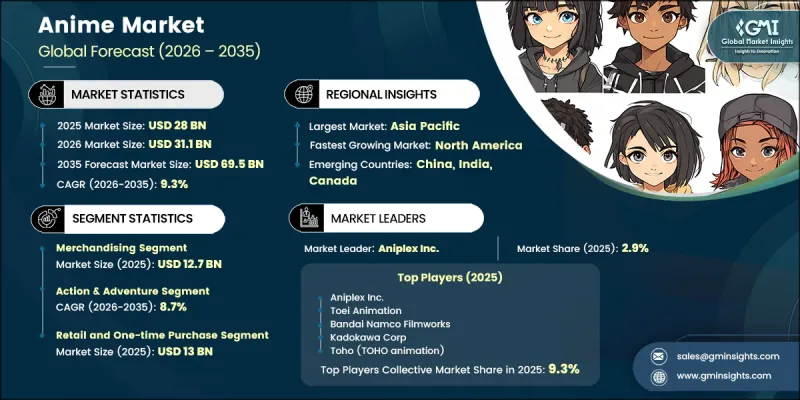

The Global Anime Market was valued at USD 28 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 69.5 billion by 2035.

Strong global demand for animated entertainment content, combined with increasing accessibility through streaming services, continues to drive market expansion. The Anime Market is benefiting from a broader international audience base, greater content availability, and the increasing commercialization of intellectual property across multiple revenue channels. Digital platforms have transformed content consumption patterns by improving accessibility and reducing barriers to entry for viewers worldwide. At the same time, the growing monetization of franchise-based intellectual property through licensing agreements, consumer products, and cross-media initiatives is strengthening revenue generation opportunities across the industry. Market growth is also being supported by ongoing investments in content production, expanding international distribution strategies, and rising consumer engagement with anime-related entertainment. As digital ecosystems continue to evolve and global demand remains strong, the Anime Market is expected to maintain robust growth momentum throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $28 Billion |

| Forecast Value | $69.5 Billion |

| CAGR | 9.3% |

Subscription-based video streaming services have emerged as one of the most influential growth drivers within the Anime Market. Streaming platforms continue to expand their anime offerings, enabling broader global access and significantly improving content availability across international markets. The industry is also witnessing a shift toward platform-supported original content development, allowing distributors to play a more active role in financing productions and accelerating content releases. This evolving business model has strengthened the long-term commitment of streaming providers to anime programming while enhancing production capacity and audience reach. At the same time, the continued decline of physical media consumption has further reinforced digital platforms as the primary distribution channel for anime content worldwide. In addition, the growing convergence between interactive entertainment and animated intellectual property is enhancing franchise value, creating new opportunities for audience engagement and long-term brand expansion through integrated content ecosystems.

The merchandising segment generated USD 12.7 billion in 2025, accounting for 45.4% share. Its leadership position reflects the enduring commercial strength of anime intellectual property, which supports licensing opportunities across numerous consumer product categories. Merchandise sales continue to generate substantial revenue streams regardless of content release schedules, while the increasing global visibility of anime content through digital channels is accelerating consumer adoption of licensed products and expanding the commercial lifespan of franchise brands.

The Action & Adventure segment generated USD 9.8 billion in 2025 holding 35% share. The segment is expected to grow at a CAGR of 8.7% through 2035. Its market dominance is driven by broad audience appeal across multiple demographic groups and its strong presence across both streaming and theatrical distribution channels. The genre also benefits from extensive monetization opportunities through licensing agreements, consumer products, digital entertainment, live experiences, and other complementary revenue streams that enhance long-term franchise value.

Asia Pacific Anime Market reached USD 16.16 billion in 2025, holding 57.7% share. Japan contributed an estimated USD 12.58 billion, reflecting its unique position as both the leading production center for anime content and the largest individual national market for anime consumption. The region continues to benefit from a highly developed production ecosystem, strong consumer demand, established distribution networks, and deep cultural engagement with animated entertainment, all of which support sustained market growth and industry leadership.

Key companies operating in the Global Anime Market include Aniplex Inc., Toei Animation Co. Ltd., Bandai Namco Filmworks Inc., Kadokawa Corporation, and Toho Co. Ltd. Companies operating in the Anime Market are strengthening their competitive position through content expansion, intellectual property development, strategic partnerships, and global distribution initiatives. Leading organizations are increasing investments in original productions and franchise development to build long-term revenue streams across multiple platforms. Collaboration with streaming providers, licensing partners, and international distributors is helping companies broaden audience reach and accelerate market penetration. Businesses are also focusing on expanding merchandise portfolios, enhancing brand visibility, and creating integrated entertainment ecosystems that support sustained consumer engagement.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service type

- 2.2.3 Genre

- 2.2.4 Payment model

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing streaming platforms increase global anime content accessibility

- 3.6.1.2 Rising popularity among younger audiences boosts anime consumption

- 3.6.1.3 Expanding gaming collaborations strengthen anime franchise visibility

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs pressure anime studio profit margins

- 3.6.2.2 Piracy issues negatively affect legitimate anime revenue generation

- 3.6.3 Opportunities

- 3.6.3.1 AI-assisted animation technologies improve production efficiency significantly

- 3.6.3.2 Expanding international licensing creates global revenue opportunities

- 3.6.1 Growth drivers

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.8.1 Pricing analysis (driven by primary research)

- 3.8.2 Historical price trend analysis licensing fees, streaming rights & merchandise retail pricing (driven by primary research)

- 3.8.3 Pricing strategy by player type (premium studio / mid-tier / independent / platform-native) (driven by primary research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models (production cost reduction, studio consolidation risk)

- 3.9.2 GenAI use cases & adoption roadmap by segment (in-betweening, background art, voice synthesis, subtitling)

- 3.9.3 Risks, limitations & regulatory considerations (artistic authenticity, IP ownership of AI output, animator displacement)

- 3.10 Infrastructure & deployment landscape (driven by primary research)

- 3.10.1 Deployment penetration by region & buyer segment (SVOD/AVOD anime platform reach across Asia Pacific, North America & Europe) (driven by primary research)

- 3.10.2 Scalability constraints & infrastructure investment trends (CDN capacity, localization infrastructure, simulcast delivery bottlenecks) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Service Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 T.V.

- 5.3 Movie

- 5.4 Video

- 5.5 Internet distribution

- 5.6 Merchandising

- 5.7 Music

- 5.8 Pachinko

- 5.9 Live entertainment

Chapter 6 Market Estimates & Forecast, By Genre, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Action & adventure

- 6.3 Sci-Fi, fantasy & Isekai

- 6.4 Romance & drama

- 6.5 Slice of life & comedy

- 6.6 Sports

- 6.7 Horror & thriller

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Payment Model, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Retail / One-time purchase

- 7.3 B2B licensing

- 7.4 Subscription (SVOD)

- 7.5 Transactional (TVOD)

- 7.6 Others

Chapter 8 & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 U.K.

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Toei Animation Co., Ltd.

- 9.1.2 Bandai Namco Filmworks Inc. (Sunrise)

- 9.1.3 Aniplex Inc.

- 9.1.4 Toho Co., Ltd. (TOHO animation)

- 9.1.5 TMS Entertainment Co., Ltd.

- 9.1.6 OLM, Inc.

- 9.1.7 Bones Inc.

- 9.2 Regional players

- 9.2.1 Kyoto Animation Co., Ltd.

- 9.2.2 Production I.G, Inc.

- 9.2.3 MADHOUSE Inc.

- 9.2.4 Pierrot Co., Ltd.

- 9.2.5 Studio Ghibli Inc.

- 9.2.6 Kadokawa Corporation

- 9.2.7 J.C.Staff Co., Ltd.

- 9.3 Emerging players

- 9.3.1 MAPPA Co., Ltd.

- 9.3.2 Ufotable Co., Ltd.

- 9.3.3 WIT Studio Co., Ltd.

- 9.3.4 Studio Trigger Inc.

- 9.3.5 Science SARU Inc.

- 9.3.6 David Production Inc.

- 9.3.7 CloverWorks Inc.