PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071294

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071294

Home Audio Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

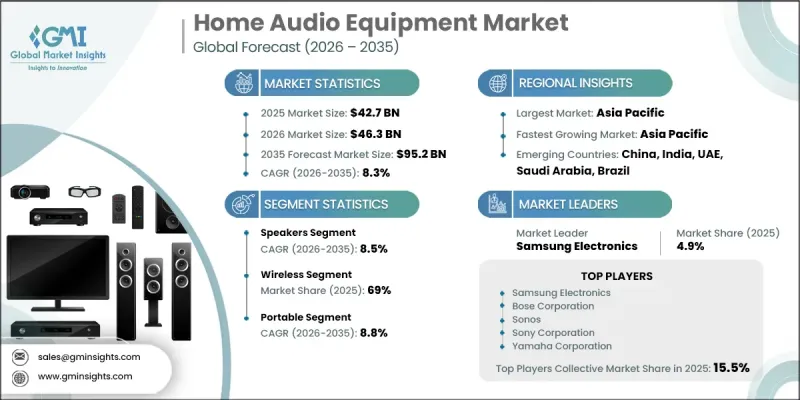

The Global Home Audio Equipment Market was valued at USD 42.7 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 95.2 billion by 2035.

The market is driven by rapid advancements in audio technology, rising consumer expectations for high-fidelity sound systems, and increasing adoption of smart home ecosystems. Growing integration of wireless connectivity standards such as Bluetooth and Wi-Fi has significantly improved device interoperability and user convenience. The expansion of digital streaming platforms and the rising penetration of smart speakers are further accelerating demand for modern audio solutions. Consumers are increasingly prioritizing immersive listening experiences, which is strengthening the adoption of advanced home entertainment systems. Rising disposable incomes, evolving lifestyles, and growing preference for premium electronics are also contributing to market expansion. Manufacturers are continuously launching innovative products, including soundbars, subwoofers, and multiroom audio systems, to enhance user experience. However, intense competition among global players and the presence of counterfeit products may restrain market potential to some extent, even though ongoing innovation and strategic collaborations are expected to sustain long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.7 Billion |

| Forecast Value | $95.2 Billion |

| CAGR | 8.3% |

The speakers segment accounted for USD 20.5 billion in 2025 and is projected to grow at a CAGR of 8.5% through 2035. This segment leads the market due to increasing consumer demand for superior sound quality and enhanced listening experiences. The rising popularity of wireless and smart speakers integrated with voice assistant technologies is further supporting segment growth. Continuous improvements in compact design and acoustic performance are helping manufacturers attract a broader consumer base.

The portable segment is expected to grow at a CAGR of 8.8% from 2026 to 2035. Growth in this segment is driven by rising demand for compact, wireless audio devices that support mobility and convenience. Expanding adoption of Bluetooth-enabled products, along with improvements in battery performance, is further boosting demand. Increasing preference for on-the-go entertainment and the growing use of smart portable audio devices are also strengthening segment expansion.

United States Home Audio Equipment Market held an 84% share, generating USD 11 billion in 2025. Market growth in the country is supported by continuous technological innovation and strong consumer demand for advanced audio systems. High adoption levels are particularly evident in densely populated and urbanized states where disposable incomes are higher. Rising demand for integrated smart home audio solutions, including speakers, soundbars, and home theater systems, continues to drive market expansion across residential applications.

The major companies operating in the Global Home Audio Equipment Industry include Sony Corporation, Samsung Electronics, LG Corporation, Yamaha Corporation, Bose Corporation, Sonos, Audio-Technica, Bang & Olufsen, Cambridge Audio, DALI, Dynaudio, KEF, Monitor Audio, Focal (Barco), Anker Soundcore, Edifier Technology, JVCKENWOOD Corporation, Panasonic Corporation, Paradigm Electronics, SVS, and Xiaomi. Companies in the home audio equipment market are actively focusing on strengthening their competitive position through continuous product innovation and integration of advanced technologies such as wireless connectivity, AI-driven sound optimization, and smart home compatibility. Many players are expanding their product portfolios with high-performance speakers, portable audio devices, and multiroom systems designed to enhance immersive listening experiences. Strategic partnerships with streaming platforms and smart home ecosystem providers are enabling better device integration and user engagement. Firms are also investing in research and development to improve acoustic performance, energy efficiency, and compact product design. Expansion into e-commerce channels and direct-to-consumer sales models is helping brands improve market reach and customer accessibility.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Technology

- 2.2.4 Installation

- 2.2.5 Price range

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Price trends

- 3.4.1 Historical price trend analysis

- 3.4.2 Pricing strategy by player type

- 3.5 Regulatory framework

- 3.5.1 Consumer Electronics Safety & EMC Standards (FCC, CE, VCCI)

- 3.5.2 Wireless Spectrum & Connectivity Regulations by Region

- 3.5.3 Energy Efficiency & Environmental Compliance Standards

- 3.6 Porter's five forces analysis

- 3.7 PESTEL analysis

- 3.8 Trade data analysis (based on paid database) (HS Code: 85182100)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional business models

- 3.9.2 GenAI use cases & adoption roadmap by customer segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Future market trends

- 3.11 Technology and innovation landscape

- 3.11.1 Current technological trends

- 3.11.2 Emerging technologies

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Speakers

- 5.2.1 Bookshelf speakers

- 5.2.2 Floor-standing speakers

- 5.2.3 In-wall/in-ceiling speakers

- 5.2.4 Portable/Bluetooth speakers

- 5.2.5 Smart speakers

- 5.2.6 Conference/communication speakers

- 5.3 Soundbars

- 5.3.1 Basic soundbars (2.0, 2.1)

- 5.3.2 Advanced soundbars (3.1, 5.1)

- 5.3.3 Dolby Atmos/DTS:X soundbars

- 5.4 Home theater systems

- 5.4.1 Home theater in a box (HTiB)

- 5.4.2 Component-based systems

- 5.4.3 Premium dedicated home theater systems

- 5.5 AV receivers & amplifiers

- 5.5.1 AV receivers (5.1, 7.1, 9.2, 11.4 channel)

- 5.5.2 Integrated amplifiers

- 5.5.3 Power amplifiers

- 5.5.4 Pre-amplifiers

- 5.5.5 Headphone amplifiers

- 5.6 Multi-room audio systems

- 5.6.1 Networked whole-home systems

- 5.6.2 Zone-based distribution systems

- 5.7 Turntables

- 5.7.1 Belt-drive turntables

- 5.7.2 Direct-drive turntables

- 5.7.3 DJ turntables

- 5.7.4 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Wired

- 6.2.1 Analog wired (RCA, XLR)

- 6.2.2 Digital wired (Optical, Coaxial, HDMI)

- 6.3 Wireless

- 6.3.1 Bluetooth

- 6.3.2 Wi-Fi

- 6.3.3 Multi-protocol

Chapter 7 Market Estimates & Forecast, By Installation, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Portable

- 7.3 Fixed

Chapter 8 Market Estimates & Forecast, By Price Range, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Low (under USD 200)

- 8.3 Medium (USD 200 - USD 499)

- 8.4 High (USD 500 and above)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Supermarkets/hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Others (individual stores, department stores, etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Audio-Technica

- 11.1.2 Bose Corporation

- 11.1.3 LG Corporation

- 11.1.4 Samsung Electronics

- 11.1.5 Sonos

- 11.1.6 Sony Corporation

- 11.1.7 Yamaha Corporation

- 11.2 Regional Key Players

- 11.2.1 Bang & Olufsen

- 11.2.2 Cambridge Audio

- 11.2.3 DALI

- 11.2.4 Dynaudio

- 11.2.5 Focal (Barco)

- 11.2.6 KEF

- 11.2.7 Monitor Audio

- 11.3 Emerging and Specialized Players

- 11.3.1 Anker Soundcore

- 11.3.2 Edifier Technology

- 11.3.3 JVCKENWOOD Corporation

- 11.3.4 Panasonic Corporation

- 11.3.5 Paradigm Electronics

- 11.3.6 SVS

- 11.3.7 Xiaomi