PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071296

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071296

Software-Defined Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

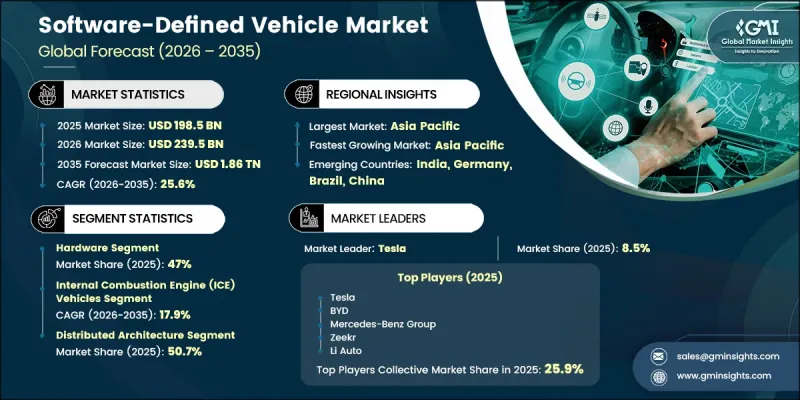

The Global Software-Defined Vehicle Market was valued at USD 198.5 billion in 2025 and is estimated to grow at a CAGR of 25.6% to reach USD 1,864.1 billion by 2035.

Market growth is being driven by the rapid digital transformation of the automotive industry and increasing adoption of software-centric vehicle architectures. Regulatory developments and evolving industry standards are encouraging automakers to enhance cybersecurity, software lifecycle management, and vehicle connectivity capabilities. Across major automotive markets, governments and industry stakeholders are supporting initiatives that accelerate the deployment of intelligent transportation systems, connected mobility platforms, advanced safety technologies, and next-generation automotive software frameworks. As vehicles become increasingly dependent on digital functionality, manufacturers are investing in scalable software ecosystems capable of supporting continuous updates, enhanced user experiences, and advanced vehicle intelligence. The shift toward centralized computing architectures is also enabling more efficient management of vehicle functions while creating opportunities for new digital services and revenue streams. Growing demand for connected vehicles, advanced driver assistance technologies, cloud-based vehicle management, and software-enabled mobility solutions continues to strengthen the long-term outlook for the software-defined vehicle market across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $198.5 Billion |

| Forecast Value | $1,864.1 Billion |

| CAGR | 25.6% |

The practical implementation of software-defined vehicle technologies continues to accelerate across the global automotive sector as manufacturers increasingly adopt centralized software architectures to improve vehicle performance and functionality. Automotive companies are focusing on integrated software platforms that support continuous feature enhancements, remote software delivery, real-time vehicle data processing, advanced analytics, and intelligent system management. This transition is reshaping vehicle development strategies and enabling manufacturers to deliver more adaptable and digitally connected driving experiences throughout a vehicle's lifecycle.

The hardware segment accounted for 47% share in 2025 and is anticipated to grow at a CAGR of 26.3% from 2026 to 2035. Hardware remains a critical component of software-defined vehicle ecosystems by providing the infrastructure required to support computing, sensing, communication, and control functions. The segment encompasses technologies that enable perception, processing, connectivity, and vehicle intelligence. As automotive architectures evolve, hardware is increasingly designed to support centralized computing environments and software-driven operations rather than functioning as isolated mechanical systems. This transition is reinforcing demand for advanced vehicle hardware capable of supporting increasingly sophisticated digital capabilities.

The internal combustion engine (ICE) vehicles segment held a 37.6% share in 2025 and is projected to grow at a CAGR of 17.9% through 2035. Although these vehicles are traditionally associated with hardware-focused designs, manufacturers are increasingly incorporating software-enabled functionalities to enhance performance, connectivity, diagnostics, and user experience. The integration of digital technologies into existing vehicle platforms is enabling broader adoption of software-driven capabilities while helping manufacturers address evolving consumer expectations and regulatory requirements. As a result, software integration within ICE vehicles continues to represent an important component of overall market growth.

China Software-Defined Vehicle Market accounted for 57% share, generating USD 41.4 billion in 2025. Market expansion in the country is supported by its strong automotive manufacturing ecosystem, increasing adoption of connected vehicle technologies, and growing deployment of intelligent mobility solutions. Vehicle manufacturers are accelerating the implementation of software-centric architectures that support remote functionality, advanced safety systems, autonomous features, and real-time operational intelligence. This trend is driving demand for scalable software development, deployment, and lifecycle management platforms capable of supporting large networks of connected vehicles and increasingly complex automotive software environments.

Key participants operating in the global software-defined vehicle market include Mercedes-Benz, Li Auto, Hyundai Motor Company, Tesla, NIO, Volkswagen, Baidu, XPeng, BYD, and Zeekr. Companies operating in the software-defined vehicle market are pursuing a variety of strategies to strengthen their competitive position and expand market share. Investments in software development capabilities, cloud-based automotive platforms, and artificial intelligence technologies remain key priorities across the industry. Market participants are focusing on building centralized vehicle architectures that support continuous software updates, enhanced cybersecurity, and advanced digital services. Strategic collaborations with technology providers, semiconductor companies, and software developers are helping manufacturers accelerate innovation and reduce development timelines. Companies are also expanding research and development activities to improve autonomous driving functions, vehicle connectivity, and intelligent mobility solutions.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 E/E Architecture

- 2.2.4 SDV Maturity Level

- 2.2.5 Application

- 2.2.6 Propulsion

- 2.2.7 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging EV Adoption Accelerating Demand for Software-First Vehicle Architectures

- 3.2.1.2 Proliferation of OTA Software Updates Reducing Recall Costs & Enabling Continuous Feature Delivery

- 3.2.1.3 Regulatory Mandates for Cybersecurity (UN R155/R156) & Autonomous Driving Safety Standards

- 3.2.1.4 Rising Consumer Demand for Connected, Personalized In-Vehicle Digital Experiences

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Complexity & Cost of Transitioning Legacy ECU-Based Architectures to Centralized Platforms

- 3.2.2.2 Expanding Cybersecurity Attack Surface as Vehicles Become Increasingly Software-Connected

- 3.2.2.3 Critical Shortage of Automotive Software Engineers & Cross-Domain Technical Talent

- 3.2.3 Market opportunities

- 3.2.3.1 Subscription-Based Feature Monetization & In-Vehicle App Store Ecosystems as New Revenue Streams

- 3.2.3.2 GenAI Integration in Digital Cockpit & ADAS Creating New High-Margin Software Layers

- 3.2.3.3 Underpenetrated Commercial Vehicle & Fleet Management SDV Segment as a High-Growth Frontier

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by primary research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.6.1.2 Federal Communications Commission (FCC)

- 3.6.1.3 U.S. Department of Transportation (USDOT)

- 3.6.1.4 Federal Trade Commission (FTC) Data Privacy Framework

- 3.6.1.5 ISO/SAE 21434 Cybersecurity Standard

- 3.6.2 Europe

- 3.6.2.1 UNECE WP.29 (R155 & R156)

- 3.6.2.2 General Data Protection Regulation (GDPR)

- 3.6.2.3 EU Data Act

- 3.6.2.4 EU General Safety Regulation (GSR)

- 3.6.2.5 ISO 26262 Functional Safety Standard

- 3.6.3 Asia Pacific

- 3.6.3.1 China Cybersecurity Law

- 3.6.3.2 China Data Security Law

- 3.6.3.3 Personal Information Protection Law (PIPL)

- 3.6.3.4 Japan Automotive Safety & Autonomous Driving Regulations

- 3.6.3.5 India Automotive Mission Plan (AMP)

- 3.6.4 Latin America

- 3.6.4.1 Brazil General Data Protection Law (LGPD)

- 3.6.4.2 Mexico Automotive Digital & Mobility Regulations

- 3.6.4.3 MERCOSUR Digital Integration Framework

- 3.6.4.4 Chile Smart Mobility Policy Framework

- 3.6.5 Middle East & Africa

- 3.6.5.1 UAE Artificial Intelligence Strategy & Data Regulations

- 3.6.5.2 Saudi Data & Artificial Intelligence Authority (SDAIA) Regulations

- 3.6.5.3 GCC Smart Mobility & Digital Economy Framework

- 3.6.5.4 African Union Digital Transformation Strategy

- 3.6.5.5 African Continental Free Trade Area (AfCFTA) Digital Protocol

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by primary research)

- 3.10 Trade Data Analysis (Driven by paid database)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Cost breakdown analysis

- 3.12 Impact of AI and Generative AI on the Market

- 3.12.1 AI Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases and Adoption Roadmap by Segment

- 3.12.3 Risks Limitations and Regulatory Considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.15.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 (USD Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Infotainment & telematics software

- 5.2.2 Advanced Driver Assistance Systems (ADAS) software

- 5.2.3 Autonomous driving software

- 5.2.4 Over-the-Air (OTA) software update platforms

- 5.2.5 Cybersecurity software

- 5.2.6 Connectivity solutions

- 5.2.7 Others

- 5.3 Hardware

- 5.3.1 Sensors

- 5.3.2 Computing hardware

- 5.3.3 Connectivity modules

- 5.3.4 Others

- 5.4 Services

- 5.4.1 Professional Services

- 5.4.2 Managed Services

Chapter 6 Market Estimates & Forecast, By E/E Architecture, 2022 - 2035 (USD Bn, Units)

- 6.1 Key trends

- 6.2 Distributed Architecture

- 6.3 Domain Centralized Architecture

- 6.4 Zonal Architecture

- 6.5 Hybrid Architecture

Chapter 7 Market Estimates & Forecast, By SDV Maturity Level, 2022 - 2035 (USD Bn, Units)

- 7.1 Key trends

- 7.2 Semi-SDV

- 7.3 Full SDV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Bn)

- 8.1 Key trends

- 8.2 Advanced Driver Assistance Systems (ADAS) & Autonomous Driving

- 8.3 Infotainment Systems / Digital Cockpit

- 8.4 Telematics & Connectivity

- 8.5 Powertrain Management

- 8.6 Body Control & Comfort Systems

- 8.7 Fleet Management

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Bn, Units)

- 9.1 Internal Combustion Engine (ICE) Vehicles

- 9.2 Electric Vehicles (EVs)

- 9.3 Hybrid Vehicles

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Bn, Units)

- 10.1 Key trends

- 10.2 Passenger Vehicles

- 10.2.1 Hatchback

- 10.2.2 Sedan

- 10.2.3 SUV

- 10.3 Commercial Vehicles

- 10.3.1 LCV (Light Commercial Vehicles)

- 10.3.2 MCV (Medium Commercial Vehicles)

- 10.3.3 HCV (Heavy Commercial Vehicles)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Norway

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Turkey

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Tesla

- 12.1.2 NVIDIA

- 12.1.3 Qualcomm

- 12.1.4 Mercedes-Benz

- 12.1.5 BMW

- 12.1.6 Volkswagen

- 12.1.7 General Motors

- 12.1.8 Robert Bosch

- 12.1.9 Aptiv

- 12.1.10 Continental

- 12.2 Regional Players

- 12.2.1 XPeng

- 12.2.2 NIO

- 12.2.3 Li Auto

- 12.2.4 Zeekr

- 12.2.5 BYD

- 12.2.6 Huawei (Intelligent Automotive BU)

- 12.2.7 Baidu

- 12.2.8 SAIC Motor

- 12.2.9 Hyundai Motor Company

- 12.2.10 Changan Automobile