PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071299

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071299

Disaster Recovery as a Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

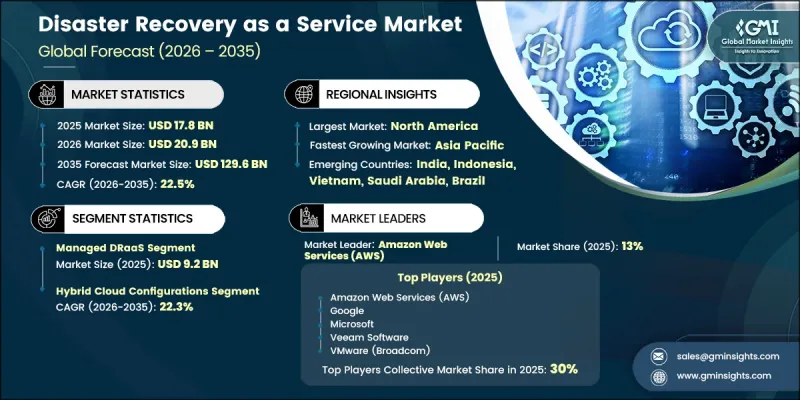

The Global Disaster Recovery as a Service Market was valued at USD 17.8 billion in 2025 and is estimated to grow at a CAGR of 22.5% to reach USD 129.6 billion by 2035.

Market growth is fueled by rising enterprise demand for cloud-based business continuity solutions and the ongoing transition away from traditional disaster recovery infrastructure. Organizations are increasingly adopting service-based recovery models as operational resilience becomes a critical business priority. Improvements in cloud technologies, greater service reliability, and the availability of scalable recovery solutions are encouraging broader adoption across organizations of all sizes. Businesses that previously delayed implementation due to operational complexity or resource limitations are now investing in advanced recovery platforms to support stricter uptime requirements and faster recovery expectations. Demand is expanding across a wide range of industries as organizations seek cost-effective methods to protect data, applications, and business operations from disruptions. The growing frequency and financial impact of cybersecurity incidents have further strengthened the importance of disaster recovery planning, making DRaaS a key component of enterprise risk management strategies. In addition, cloud-based consumption models are improving accessibility for mid-sized organizations and smaller enterprises, supporting broader market penetration and long-term industry growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.8 Billion |

| Forecast Value | $129.6 Billion |

| CAGR | 22.5% |

The managed DRaaS segment generated USD 9.2 billion in 2025 and held a 52.2% share. Its dominant position is supported by increasing demand for outsourced expertise and end-to-end disaster recovery management. Many organizations prefer managed service models because they reduce operational complexity while providing continuous monitoring, testing, maintenance, and recovery execution. As disaster recovery environments become more sophisticated, businesses are increasingly relying on specialized service providers to ensure system resilience and minimize operational risks.

The hybrid cloud deployments segment accounted for USD 8.3 billion in 2025 and representing 47.1% share. Strong adoption reflects the need for flexible recovery environments capable of supporting diverse IT infrastructures. Organizations increasingly operate across multiple technology environments and require disaster recovery solutions that can seamlessly protect workloads, applications, and data without creating management inefficiencies. The ability to integrate different computing environments within a unified recovery framework continues to drive demand for hybrid cloud-based DRaaS solutions.

North America Disaster Recovery as a Service Market generated USD 7.1 billion in 2025. Regional growth is supported by substantial enterprise technology investments, advanced cloud infrastructure, increasing focus on operational resilience, and evolving cybersecurity requirements. Organizations across the region continue to prioritize business continuity planning and data protection strategies, creating favorable conditions for long-term DRaaS adoption.

Key companies operating in the global disaster recovery as a service market include Amazon Web Services, VMware (Broadcom), IBM, Commvault Systems, Microsoft, Rubrik, Dell Technologies, NTT Communications, Google, and Veeam Software. Companies competing in the disaster recovery as a service market are focusing on strategic initiatives aimed at expanding market share and strengthening customer relationships. Product innovation remains a major priority, with providers enhancing automation capabilities, recovery speed, scalability, and security features. Vendors are investing heavily in cloud-native technologies and artificial intelligence-driven management tools to improve operational efficiency and service performance. Strategic partnerships with cloud providers, technology integrators, and enterprise software vendors are helping companies broaden their reach and strengthen solution ecosystems.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Service component

- 2.2.4 Deployment model

- 2.2.5 Organization size

- 2.2.6 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Cyberattack and ransomware surge

- 3.2.1.2 Strict compliance regulations globally

- 3.2.1.3 Rapid cloud adoption growth

- 3.2.1.4 Remote and hybrid work expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Third-party data security concerns

- 3.2.2.2 Data sovereignty restrictions globally

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven DR automation systems

- 3.2.3.2 Ransomware-focused cyber recovery services

- 3.2.3.3 SME adoption in emerging markets

- 3.2.3.4 Multi-cloud edge DR platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 SAE International

- 3.6.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.6.2 Europe

- 3.6.2.1 European Commission (EC)

- 3.6.2.2 European Committee for Standardization (CEN-CENELEC)

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology (MIIT, China)

- 3.6.3.2 Bureau of Indian Standards (BIS)

- 3.6.4 Latin America

- 3.6.4.1 National Institute of Metrology, Quality and Technology (INMETRO - Brazil)

- 3.6.4.2 Mexican Secretariat of Economy (SE)

- 3.6.5 Middle East & Africa

- 3.6.5.1 Gulf Standardization Organization (GSO)

- 3.6.5.2 South African Bureau of Standards (SABS)

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.12.1 Base Case key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Managed DRaaS

- 5.3 Assisted DRaaS

- 5.4 Self-service DRaaS

Chapter 6 Market Estimates & Forecast, By Service Component, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Backup & recovery

- 6.3 Real-time replication

- 6.4 Data protection

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Public cloud

- 7.3 Private cloud

- 7.4 Hybrid cloud

Chapter 8 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprises

- 8.3 Small & medium enterprises (SMEs)

Chapter 9 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & Telecommunications

- 9.4 Government & Public Sector

- 9.5 Healthcare

- 9.6 Retail & Consumer Goods

- 9.7 Media & Entertainment

- 9.8 Manufacturing & Logistics

- 9.9 Education

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Sweden

- 10.3.7 Switzerland

- 10.3.8 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Amazon Web Services (AWS)

- 11.1.2 Commvault Systems

- 11.1.3 Dell Technologies

- 11.1.4 Google

- 11.1.5 IBM

- 11.1.6 Microsoft

- 11.1.7 RubriK

- 11.1.8 Veeam Software

- 11.1.9 VMware (Broadcom)

- 11.2 Regional players

- 11.2.1 NTT Communications

- 11.2.2 TierPoint

- 11.2.3 Recovery Point Systems

- 11.2.4 Cohesity

- 11.2.5 Acronis International

- 11.2.6 Zerto (HPE)

- 11.2.7 11:11 Systems

- 11.3 Emerging players

- 11.3.1 Datto (Kaseya)

- 11.3.2 Druva

- 11.3.3 HYCU

- 11.3.4 Infrascale