PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071306

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071306

Parking Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

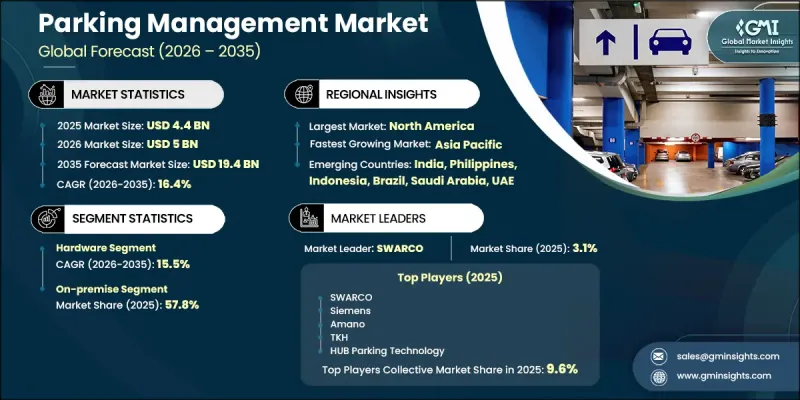

The Global Parking Management Market was valued at USD 4.4 billion in 2025 and is estimated to grow at a CAGR of 16.4% to reach USD 19.4 billion by 2035.

Market growth is driven by the widening gap between rising vehicle ownership and the limited availability of urban parking space. As cities face mounting congestion and land constraints, stakeholders are increasingly adopting intelligent parking technologies to maximize utilization of existing assets rather than investing in new physical infrastructure. Advanced parking management solutions incorporating occupancy monitoring, automated access control, digital payment systems, cloud connectivity, and data-driven analytics are enabling operators to improve operational efficiency, increase revenue generation, and enhance user experiences. The transition toward smart urban mobility frameworks is further accelerating market development as municipalities prioritize digital transportation infrastructure to support sustainable city planning. Growing emphasis on traffic optimization, reduced vehicle idle times, improved parking guidance, and enhanced regulatory compliance is transforming parking management from a standalone operational function into a critical component of broader urban mobility ecosystems. As a result, demand for intelligent parking technologies continues to increase across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.4 Billion |

| Forecast Value | $19.4 Billion |

| CAGR | 16.4% |

The hardware segment reached USD 2,384.7 million in 2025 accounting for 54% share. Hardware solutions remain fundamental to parking infrastructure modernization, supporting vehicle access management, occupancy detection, payment processing, monitoring, and traffic flow optimization. Demand continues to be fueled by both new parking facility developments and the modernization of legacy parking systems. As operators seek to improve automation and operational efficiency, investments in advanced hardware technologies remain a major contributor to overall market growth.

The cloud-based segment is expected to register a CAGR of 20.9% through 2035. Organizations are increasingly transitioning toward cloud-enabled platforms due to their scalability, centralized management capabilities, and ability to integrate multiple operational functions into a single ecosystem. Cloud infrastructure allows operators to manage occupancy information, transaction records, enforcement activities, analytics, and user engagement tools through unified digital platforms. The growing preference for centralized management, combined with rising adoption of intelligent monitoring technologies, continues to strengthen demand for cloud-based parking solutions worldwide.

Germany Parking Management Market generated USD 372.2 million in 2025 growing at a CAGR of 15.3% through 2035. Growth is being supported by increasing investments in smart infrastructure initiatives, urban mobility modernization programs, and digital transportation systems. Regulatory requirements surrounding data protection and privacy continue to influence procurement decisions, encouraging the adoption of secure and compliant parking management technologies. The country's commitment to intelligent mobility solutions, combined with ongoing digital transformation efforts, is expected to support sustained market expansion over the coming years.

Major companies operating in the global parking management market include SpotHero, Flowbird, TIBA Parking Systems, SKIDATA, Amano, Verra Mobility, Cleverciti Systems, HUB Parking Technology, Hectronic, Arrive, Swarco, Genetec, Designa Verkehrsleittechnik, ParkHelp Technologies, Nedap, IPS, Flash, Frogparking, CAME Parkare, and T2 Systems. Companies operating in the parking management market are focusing on technology innovation, strategic partnerships, and platform integration to strengthen their market position. Businesses are investing heavily in cloud-based solutions, artificial intelligence, predictive analytics, and real-time occupancy monitoring to improve operational efficiency and customer experience. Many vendors are expanding software capabilities to support centralized management, dynamic pricing, automated enforcement, and seamless payment processing. Strategic collaborations with municipalities, transportation authorities, and smart city developers are helping companies secure long-term projects and expand their customer base. Organizations are also prioritizing data security, regulatory compliance, and interoperability to meet evolving market requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Parking Site

- 2.2.5 Solution

- 2.2.6 End User

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Urbanization and Vehicle Ownership Growth

- 3.2.1.2 Smart City Initiatives and Digital Infrastructure Investments

- 3.2.1.3 Growing Adoption of Mobile and Contactless Payments

- 3.2.1.4 Demand for Real-Time Parking Availability Solutions

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Initial Infrastructure and Deployment Costs

- 3.2.2.2 Data Security and Privacy Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Cloud-Based Parking Platform Migration

- 3.2.3.2 AI-Assisted Occupancy Forecasting

- 3.2.3.3 Mobile Reservation and Contactless Payment Expansion

- 3.2.3.4 Smart Mobility Integration and Data Sharing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 United States Department of Transportation (USDOT) - Intelligent Transportation Systems (ITS) Programs

- 3.5.1.2 Federal Highway Administration (FHWA) - Smart Parking and Urban Mobility Initiatives

- 3.5.1.3 National Highway Traffic Safety Administration (NHTSA) - Connected Vehicle and Transportation Infrastructure Guidelines

- 3.5.1.4 Transport Canada - Smart Transportation and Urban Mobility Regulations

- 3.5.2 Europe

- 3.5.2.1 European Commission - Urban Mobility Framework and Smart City Initiatives

- 3.5.2.2 Intelligent Transport Systems (ITS) Directive (EU)

- 3.5.2.3 General Data Protection Regulation (GDPR) for Parking Data Management

- 3.5.2.4 European Committee for Standardization (CEN) Smart Parking Standards

- 3.5.3 Asia-Pacific

- 3.5.3.1 China Ministry of Transport - Smart Transportation and Intelligent Parking Policies

- 3.5.3.2 Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

- 3.5.3.3 India Ministry of Housing and Urban Affairs (MoHUA) - Smart Cities Mission

- 3.5.3.4 Australia National Smart Cities and Transport Infrastructure Framework

- 3.5.4 Latin America

- 3.5.4.1 Brazil National Traffic Secretariat (SENATRAN) - Urban Mobility and Parking Regulations

- 3.5.4.2 Mexico Ministry of Infrastructure, Communications and Transport (SICT) - Smart Mobility Programs

- 3.5.5 Middle East & Africa

- 3.5.5.1 GCC Smart City and Intelligent Transportation Infrastructure Initiatives

- 3.5.5.2 South Africa National Land Transport Act (NLTA)

- 3.5.5.3 UAE Smart Dubai and Intelligent Mobility Regulations

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - key macro & industry variables driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors & Detectors

- 5.2.2 Barriers & Gates

- 5.2.3 Payment Kiosks & Terminals

- 5.2.4 LPR Cameras

- 5.2.5 Guidance Displays & Signage

- 5.3 Software

- 5.3.1 Access & Revenue Control Software

- 5.3.2 Parking Guidance Software

- 5.3.3 Reservation Management Software

- 5.3.4 Enforcement Management Software

- 5.3.5 Security & Surveillance Software

- 5.3.6 Valet Management Software

- 5.4 Services

- 5.4.1 Consulting Services

- 5.4.2 System Integration & Deployment Services

- 5.4.3 Support & Maintenance Services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 On-Premise

- 6.3 Cloud-Based

Chapter 7 Market Estimates & Forecast, By Parking Site, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Off-Street Parking

- 7.3 On-Street Parking

Chapter 8 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Parking Access and Revenue Control Systems

- 8.3 Parking Guidance Systems

- 8.4 Parking Reservation and Payment Solutions

- 8.5 Parking Analytics and Monitoring Solutions

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End User, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Government & Municipalities

- 9.3 Commercial Establishments

- 9.4 Residential

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 SKIDATA

- 11.1.2 Amano

- 11.1.3 Arrive

- 11.1.4 Genetec

- 11.1.5 Swarco

- 11.1.6 Nedap

- 11.1.7 Verra Mobility

- 11.1.8 Designa Verkehrsleittechnik

- 11.1.9 HUB Parking Technology

- 11.1.10 ParkHelp Technologies

- 11.2 Regional Players

- 11.2.1 T2 Systems

- 11.2.2 IPS

- 11.2.3 SpotHero

- 11.2.4 Flash

- 11.2.5 TIBA Parking Systems

- 11.2.6 Hectronic

- 11.2.7 CAME Parkare

- 11.2.8 Cleverciti Systems

- 11.2.9 Flowbird

- 11.2.10 Frogparking