PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071335

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071335

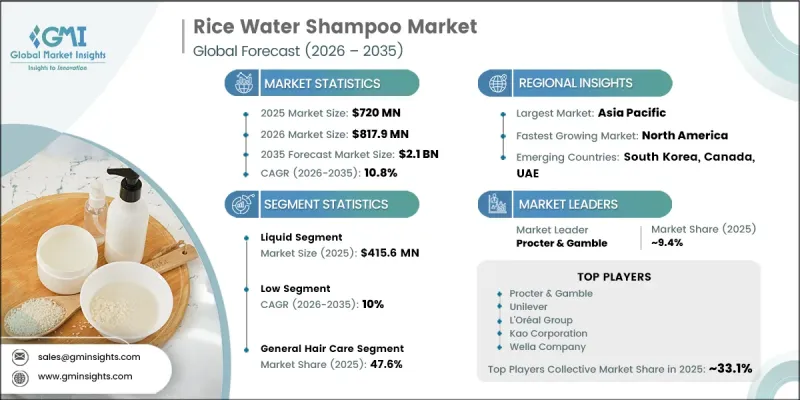

Rice Water Shampoo Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Rice Water Shampoo Market was valued at USD 720 million in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 2.1 billion by 2035.

Growth in this market is driven by increasing consumer inclination toward natural, herbal, and traditional hair care solutions that emphasize scalp health and hair strengthening benefits. Consumers are progressively shifting toward rice water-based shampoos due to their perceived effectiveness in supporting hair repair, improving texture, and enhancing overall scalp nourishment. Rising awareness regarding chemical-free and plant-derived personal care formulations is further boosting the adoption of products enriched with fermented rice water, botanical extracts, and naturally derived conditioning agents. The clean beauty movement is also influencing manufacturers to develop sulfate-free and silicone-free formulations that align with evolving consumer expectations. Additionally, expanding demand for premium hair care solutions targeting specific concerns such as hair damage, dryness, and growth enhancement is supporting product diversification. Digital platforms and social media-driven beauty trends are significantly improving product visibility and accelerating adoption among younger demographics. Overall, the market is advancing steadily due to rising wellness awareness, ingredient transparency, and growing preference for nature-inspired personal care products across global consumer segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $720 Million |

| Forecast Value | $2.1 Billion |

| CAGR | 10.8% |

The liquid formulation segment generated USD 415.6 million in 2025. Its leadership is supported by widespread consumer familiarity, ease of use, and compatibility with diverse hair care routines. Liquid shampoos offer effective cleansing performance, broad scalp coverage, and convenience, making them highly suitable for everyday use. Strong adoption across both mass and premium categories further reinforces segment strength.

The general hair care application segment accounted for a 47.6% share in 2025 and is expected to grow at a CAGR of 10.1% through 2035. This segment maintains dominance due to the strong demand for routine hair cleansing and maintenance solutions. Consumers widely prefer rice water-based shampoos for everyday use, supported by their perceived benefits in improving softness, shine, and overall scalp condition. Broad applicability across different hair types and age groups continues to strengthen its market penetration.

China Rice Water Shampoo Market generated USD 109.3 million in 2025 and is projected to grow at a CAGR of 9.1% through 2035. The country's leadership is driven by strong consumer interest in traditional and herbal hair care products, along with rising awareness of scalp wellness and natural beauty solutions. Increasing disposable incomes and growing preference for plant-based personal care products are further supporting market expansion. Domestic brands are actively promoting rice water-based shampoos through online retail channels and influencer-led digital campaigns. Continuous innovation involving fermented rice water and botanical blends is also gaining strong traction among urban consumers.

Major companies operating in the Global Rice Water Shampoo Market include Procter & Gamble, L'Oreal Group, Unilever, Kao Corporation, Wella Company, As I Am, Daeng Gi Meo Ri, Mamaearth, The Face Shop, Pilgrim, Deyga Organics, Luseta Beauty, Trunish Lifescience, Nuskhe by Paras, Mielle Organics, WOW Skin Science, Viori, Kitsch, Oriza Hair, First Botany, and Nature Republic. Companies in the rice water shampoo market are strengthening their competitive position through continuous product innovation, clean-label formulation development, and targeted marketing strategies. A key focus is placed on launching sulfate-free, silicone-free, and naturally derived shampoos that align with the rising demand for clean beauty solutions. Manufacturers are increasingly incorporating functional ingredients such as fermented rice water, herbal extracts, and vitamins to enhance product efficacy and consumer appeal. Expansion of digital marketing channels, influencer collaborations, and social media engagement is helping brands improve visibility and attract younger consumers. Companies are also investing in premium product lines that address specific concerns such as hair damage, scalp nourishment, and hair growth support. Strengthening distribution networks through e-commerce platforms and direct-to-consumer models is further improving accessibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Price range

- 2.2.4 Application

- 2.2.5 Consumer group

- 2.2.6 Material type

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer preference for natural and traditional hair care solutions

- 3.2.1.2 Expansion of premium hair care and scalp treatment product categories

- 3.2.1.3 Growing influence of K-beauty and Asian beauty traditions globally

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Availability of counterfeit and low-quality herbal hair care products

- 3.2.2.2 High competition from conventional and multifunctional shampoos

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for clean-label and sulfate-free personal care products

- 3.2.3.2 Growth of e-commerce and influencer-driven beauty marketing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Trade data analysis (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Personalized product recommendations

- 3.11.4 Virtual hair analysis and diagnostic tools

- 3.11.5 AI-powered formulation optimization

- 3.11.6 Content generation for marketing and e-commerce

- 3.11.7 Risks, limitations, and regulatory considerations

- 3.12 Distribution infrastructure and channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region and format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps and emerging channel shifts (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Liquid

- 5.3 Gel

- 5.4 Foam

- 5.5 Bar/Solid

- 5.6 Cream/Paste

Chapter 6 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 General hair care

- 7.3 Hair growth promotion

- 7.4 Damage repair

- 7.5 Scalp treatment

Chapter 8 Market Estimates & Forecast, By Consumer Group, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Women

- 8.3 Men

- 8.4 Unisex

- 8.5 Children

Chapter 9 Market Estimates & Forecast, By Material Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Organic

- 9.3 Inorganic

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 Company websites

- 10.2.2 E-commerce

- 10.3 Offline

- 10.3.1 Hypermarket/supermarket

- 10.3.2 Specialty stores

- 10.3.3 Retail stores

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 Procter & Gamble

- 12.1.2 Unilever

- 12.1.3 L'Oreal Group

- 12.1.4 Kao Corporation

- 12.1.5 Wella Company

- 12.1.6 Daeng Gi Meo Ri

- 12.1.7 As I Am

- 12.2 Regional Champions

- 12.2.1 The Face Shop

- 12.2.2 Mamaearth

- 12.2.3 Deyga Organics

- 12.2.4 Pilgrim

- 12.2.5 Luseta Beauty

- 12.2.6 Trunish Lifescience

- 12.2.7 Nuskhe by Paras

- 12.3 Emerging & Specialized Players

- 12.3.1 Viori

- 12.3.2 Kitsch

- 12.3.3 Oriza Hair

- 12.3.4 First Botany

- 12.3.5 Mielle Organics

- 12.3.6 WOW Skin Science

- 12.3.7 Nature Republic