PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071408

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071408

North America Contact Lenses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

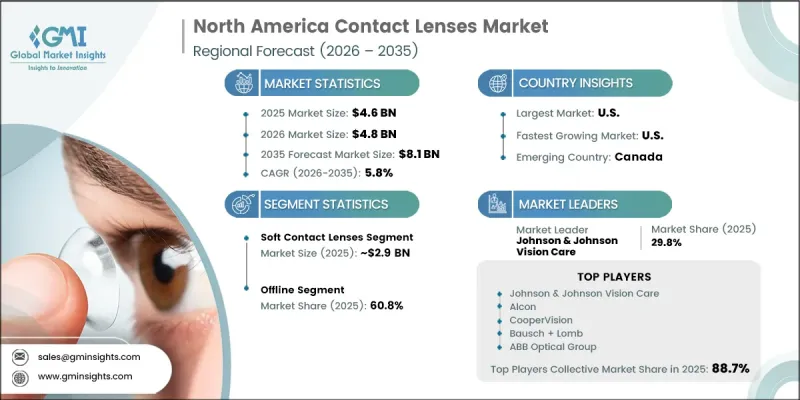

North America Contact Lenses Market was valued at USD 4.6 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 8.1 billion by 2035.

Growth is driven by the increasing incidence of refractive errors such as myopia, astigmatism, and presbyopia, which are becoming more common across both younger and aging populations. Contact lenses are increasingly regarded as essential medical devices rather than discretionary optical accessories, reinforcing stable demand across the region. The expanding aging population is further boosting demand for multifocal and presbyopia-correcting lenses, while younger consumers are increasingly adopting lenses due to lifestyle convenience and visual comfort. High screen exposure in daily life is also contributing to growing vision correction requirements. Additionally, strong healthcare infrastructure, high disposable income levels, and widespread vision insurance coverage continue to support consistent product adoption across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 5.8% |

Soft contact lenses generated USD 2.9 billion in 2025 and is projected to reach USD 5.1 billion by 2035. This segment continues to lead due to its superior comfort, ease of use, and strong compatibility with the human eye. Manufactured using flexible, moisture-retaining materials, these lenses naturally adapt to corneal shape, reducing irritation and improving wearer experience. Their quick adaptation period makes them a preferred option for first-time users, significantly improving retention rates among new consumers entering the contact lens market.

The offline distribution channel accounted for 60.8% share in 2025, maintaining its leading position. This dominance is attributed to the clinical nature of contact lenses, which require professional fitting and prescription validation. Consumers rely on in-person eye examinations, lens fitting services, and ongoing ocular health assessments conducted by optometrists. Optical retail outlets, clinics, and specialty stores remain essential for ensuring proper lens selection, safety compliance, and long-term eye care management, which cannot be fully replicated through digital-only platforms.

United States Contact Lenses Market held a 91.4% share in 2025. Market growth in the country is supported by a large population base experiencing increasing rates of vision disorders, along with heightened awareness of eye health and routine vision care. Rising digital screen exposure is further intensifying demand for corrective lenses across younger demographics. The presence of a well-established distribution ecosystem, combined with strong participation from leading manufacturers and optical service providers, continues to reinforce the country's dominant position in the regional market.

Key companies operating in the North America contact lenses market include Bausch + Lomb, Johnson & Johnson Vision Care, CooperVision, Alcon, Hoya Corporation, ABB Optical Group, Menicon Co., Ltd., Euclid Vision Group, Clearlab International, AccuLens, Art Optical Contact Lens, Metro Optics of Austin, Optik K&R Inc., Pegavision Corporation, Precision Technology Services (PTS Optics), St.Shine Optical Co., Ltd., TruForm Optics, Visioneering Technologies, Inc., Visco Vision Inc., Viscon Contact Lens Manufacturing Ltd., and X-Cel Specialty Contacts. Market participants are focusing on strengthening their position through continuous innovation in lens materials, design, and comfort-enhancing technologies. Companies are investing in advanced silicone hydrogel and moisture-retention technologies to improve wearability and eye health outcomes. Expansion of product portfolios, including daily disposable, multifocal, and specialty lenses, is helping manufacturers cater to diverse consumer needs. Strategic partnerships with optical retailers and healthcare professionals are enhancing distribution reach and customer engagement. Firms are also leveraging digital platforms for subscription-based lens delivery models to improve convenience and retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Design

- 2.2.5 Usage

- 2.2.6 Pricing

- 2.2.7 Application

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of refractive errors

- 3.2.1.2 Shift towards daily disposable lenses

- 3.2.1.3 Cosmetic and lifestyle appeal

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced lenses

- 3.2.2.2 Competition from surgical alternatives

- 3.2.3 Opportunities

- 3.2.3.1 Smart contact lens innovation

- 3.2.3.2 AI-driven customization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 FDA Device Classification - Class II vs. Class III Contact Lenses

- 3.6.2 510(k) Premarket Notification Requirements

- 3.6.3 Premarket Approval (PMA) Pathway for Class III Devices

- 3.6.4 FTC Contact Lens Rule & Prescription Portability Regulations

- 3.7 Trade data analysis (HS Code: 90013000) (Driven by paid database)

- 3.7.1 Import/export volume & value trends (driven by primary research)

- 3.7.2 Key trade corridors & tariff impact (driven by primary research)

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis (2022-2025)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Raw material analysis

- 3.13 Consumer behavior analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Soft contact lenses

- 5.3 Rigid gas permeable lenses

- 5.4 Hybrid contact lenses

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Hydrogel

- 6.2.1 Silicone hydrogel

- 6.2.2 HEMA hydrogel

- 6.3 Rigid gas permeable

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Design, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Spherical

- 7.3 Toric

- 7.4 Multifocal

- 7.5 Other

Chapter 8 Market Estimates and Forecast, By Usage, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Daily disposable

- 8.3 Frequently disposable

- 8.4 Disposable

- 8.5 Reusable

Chapter 9 Market Estimates and Forecast, By Pricing, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Low

- 9.3 Medium

- 9.4 High

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Vision correction

- 10.3 Therapeutic lenses

- 10.4 Cosmetic lenses

- 10.5 Prosthetic lenses

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Offline

- 11.2.1 Specialty stores

- 11.2.2 Supermarkets & hypermarkets

- 11.2.3 Pharmacy stores

- 11.3 Online

- 11.3.1 E-commerce

- 11.3.2 Brand websites

Chapter 12 Market Estimates & Forecast, By Country, 2022-2035 (USD Billion) (Million units)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

Chapter 13 Company Profiles

- 13.1 Global Companies

- 13.1.1 Alcon

- 13.1.1.1 Business Overview

- 13.1.1.2 Financial Data

- 13.1.1.3 Product Landscape

- 13.1.1.4 Strategic Outlook

- 13.1.1.5 SWOT Analysis

- 13.1.2 Bausch + Lomb

- 13.1.3 Clearlab International

- 13.1.4 CooperVision

- 13.1.5 Hoya Corporation

- 13.1.6 Johnson & Johnson Vision Care

- 13.1.7 Menicon Co., Ltd.

- 13.1.8 Pegavision Corporation

- 13.1.9 St.Shine Optical Co., Ltd.

- 13.1.1 Alcon

- 13.2 Regional Companies

- 13.2.1 ABB Optical Group

- 13.2.2 AccuLens

- 13.2.3 Art Optical Contact Lens

- 13.2.4 Metro Optics of Austin

- 13.2.5 Optik K&R Inc.

- 13.2.6 Precision Technology Services (PTS Optics)

- 13.2.7 TruForm Optics

- 13.2.8 Visco Vision Inc.

- 13.2.9 Viscon Contact Lens Manufacturing Ltd.

- 13.2.10 X-Cel Specialty Contacts

- 13.3 Emerging Companies

- 13.3.1 Euclid Vision Group

- 13.3.2 Visioneering Technologies, Inc.