PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071417

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071417

Large Scale Variable Frequency Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

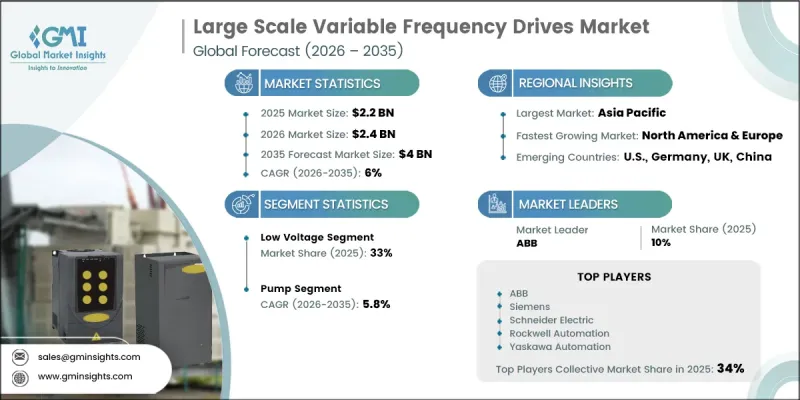

The Global Large Scale Variable Frequency Drives Market was valued at USD 2.2 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 4 billion by 2035.

Demand growth is tied to the fact that industrial motor systems account for nearly 45% of global electricity consumption, positioning variable frequency drives as a key efficiency optimization tool for reducing operational costs and emissions. Industrial capital spending across power generation, water management, mining, chemicals, and grid modernization continues to reinforce adoption, with VFDs increasingly embedded in large electromechanical systems as standard control components. In developing regions, new industrial projects are generating fresh demand for high-capacity drives equipped with remote monitoring and IoT-based diagnostics, while developed markets are focused on replacing aging fixed-speed motor systems through modernization programs. The market's long-term growth is structurally driven, as electrification and automation of industrial processes continue to improve energy performance and regulatory compliance across sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.2 Billion |

| Forecast Value | $4 Billion |

| CAGR | 6% |

The low voltage segment held 33% share in 2025 and is projected to grow at a CAGR of 4.7% through 2035. These drives, typically operating below 1 kV, are widely used in mid-range power applications such as auxiliary ventilation systems, secondary pumping operations, and conveyor mechanisms within manufacturing environments. Growth in this segment is relatively moderate due to market maturity in core applications and increasing pricing pressure from regional manufacturers, particularly in Asia, which is intensifying competition in standardized product categories.

The pump application segment held a 42.2% share in 2025, growing at a CAGR of 5.8% through 2035. Variable frequency drives are widely used in pumping systems to regulate motor speed according to real-time demand, significantly improving energy efficiency compared to fixed-speed alternatives. Strong adoption is observed in oil and gas operations, where pump control systems are essential for extraction and transport processes, as well as in water and wastewater infrastructure, which continues to expand due to ongoing utility modernization programs and urban infrastructure development.

North America Large Scale Variable Frequency Drives Market accounted for 20.9% share in 2025 and is projected to grow at a CAGR of 6.3% through 2035. The United States remains the primary regional contributor, supported by a large installed base of industrial motors, extensive energy and process infrastructure, and regulatory frameworks focused on energy efficiency improvements. Federal-level efficiency initiatives and industrial compliance requirements continue to encourage the replacement of legacy motor systems with advanced variable speed drive technologies, particularly in process industries, utilities, and energy-intensive operations.

Major players operating in the global large scale variable frequency drives market include ABB, Siemens, Schneider Electric, Rockwell Automation, Yaskawa Automation & Drives, TMEIC, GE Vernova, and NIDEC. Companies in the large scale variable frequency drives market are strengthening their position through continuous investment in high-efficiency power electronics and advanced motor control algorithms that improve energy optimization across industrial systems. They are expanding their product portfolios with digitalized drives that integrate IoT connectivity, predictive maintenance, and remote diagnostics capabilities. Strategic collaborations with industrial automation providers and EPC contractors are enabling deeper integration of VFDs into large-scale infrastructure projects. Manufacturers are also focusing on modular and scalable drive architectures to meet diverse application requirements across voltage ranges and industries. Expansion into emerging markets is being supported by localized manufacturing and service networks to reduce deployment costs and improve responsiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Voltage trends

- 2.4 Application trends

- 2.5 End-use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis, 2022-2035 (USD/Unit) (Driven by Primary Research)

- 3.7.1 By voltage (Driven by Primary Research)

- 3.7.2 By region (Driven by Primary Research)

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

- 3.10 Impact of AI & Generative AI on the market (Solution Core)

- 3.10.1 AI-Driven production optimization (Solution Core)

- 3.10.2 Predictive maintenance & fault detection (Solution Core)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Voltage, 2022 - 2035 (USD Million, '000 Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, '000 Units)

- 6.1 Key trends

- 6.2 Pump

- 6.3 Fan

- 6.4 Conveyor

- 6.5 Compressor

- 6.6 Extruder

- 6.7 Others

Chapter 7 Market Size and Forecast, By End-Use, 2022 - 2035 (USD Million, '000 Units)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Power generation

- 7.4 Mining & metals

- 7.5 Pulp & paper

- 7.6 Marine

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Benshaw

- 9.3 Delta Electronics

- 9.4 Eaton

- 9.5 Emotron

- 9.6 Fuji Electric

- 9.7 GE Vernova

- 9.8 General Atomics

- 9.9 Hiconics Technology

- 9.10 Hitachi Hi-Rel Power Electronics

- 9.11 Ingeteam

- 9.12 NIDEC

- 9.13 Rockwell Automation

- 9.14 Schneider Electric

- 9.15 Shenzhen INVT Electric

- 9.16 Siemens

- 9.17 TMEIC

- 9.18 Triol

- 9.19 VEM Group

- 9.20 Wolong Electric Group

- 9.21 Xi'an XICHI Electric

- 9.22 YASKAWA Automation & Drives