PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083106

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083106

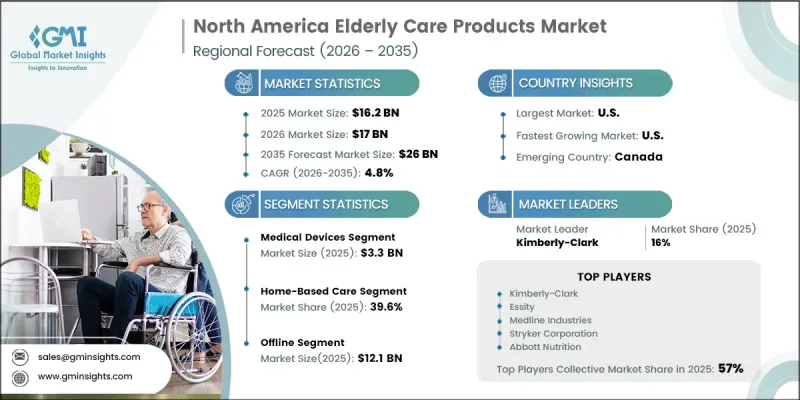

North America Elderly Care Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Elderly Care Products Market was valued at USD 16.2 billion in 2025 and is estimated to grow at a CAGR of 4.8% to reach USD 26 billion by 2035.

The market continues to grow as North America experiences a steady rise in its aging population, creating sustained demand for products designed to support the health, comfort, and independence of older adults. Improvements in life expectancy and demographic shifts are contributing to a larger elderly population that requires specialized care solutions for everyday living. As healthcare needs become more prominent with advancing age, consumers increasingly seek products that enhance safety, mobility, wellness, and overall quality of life. This demographic transformation is encouraging manufacturers to introduce innovative products that address evolving consumer preferences while improving convenience and long-term care outcomes. Growing awareness of healthy aging, increasing healthcare spending, and continuous advancements in product development are further supporting market growth. At the same time, the expanding elderly population is driving consistent demand for a broad range of care products, encouraging companies to diversify their offerings and improve product performance. These long-term demographic and healthcare trends are expected to create favorable opportunities for the North America elderly care products market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.2 Billion |

| Forecast Value | $26 Billion |

| CAGR | 4.8% |

As the aging population continues to increase across North America, the demand for elderly care products is expected to grow steadily. Age-related health conditions often require greater levels of personal assistance and long-term support, encouraging higher adoption of products designed to improve comfort, safety, and daily living. This growing consumer base is also driving demand for a wider range of care solutions with enhanced functionality and improved usability. Manufacturers are responding by expanding their product portfolios and investing in innovation to develop more advanced, reliable, and user-friendly solutions. Continuous product development and diversification are becoming essential competitive strategies as companies work to meet changing consumer expectations and strengthen their presence within the North America elderly care products market.

The medical devices segment accounted for USD 3.3 billion in 2025. Medical devices remain a vital category because the aging population requires continuous health management and ongoing medical support. The increasing prevalence of long-term health conditions among older adults continues to drive demand for dependable medical equipment that supports routine health assessment and disease management. Consumers increasingly prefer devices that are accurate, easy to operate, and suitable for regular use, contributing to the segment's strong market position. Continuous technological improvements and greater emphasis on preventive healthcare are expected to further strengthen demand for medical devices across the regional elderly care products industry.

The home-based care segment held a 39.6% share in 2025. The increasing preference for receiving care within the home continues to reshape the regional market as older adults seek greater independence, comfort, and familiarity in their daily lives. Home care solutions allow aging individuals to maintain their preferred lifestyle while reducing dependence on institutional care settings. Financial considerations also contribute to this shift, as many consumers seek cost-effective long-term care alternatives. Growing demand for products that support independent living is encouraging manufacturers to expand their home care portfolios and develop solutions that improve convenience, accessibility, and overall quality of life for elderly consumers.

United States Elderly Care Products Market held a 72.8% share, generating USD 11.8 billion in 2025. The country maintains its leadership position due to its large and rapidly expanding elderly population, which continues to create substantial demand for products designed to support aging consumers. Strong healthcare infrastructure, high consumer purchasing power, and widespread access to healthcare services further contribute to market growth. Rising investments in elderly wellness and long-term care continue to encourage product adoption across the country. As demographic trends continue to favor population aging, the United States is expected to remain the largest contributor to revenue within the North America elderly care products market.

Major companies operating in the North America elderly care products market include Invacare Corporation, Medline Industries, Stryker Corporation, Arjo, Essity, Kimberly-Clark, Abbott Nutrition, Drive Medical, Graham-Field Health Products, Carex Health Brands, Dynarex Corporation, Enovis Corporation, First Quality Enterprises, EZ-ACCESS, Medical Guardian, Stander Inc., Silverts Adaptive Clothing & Footwear, Bay Alarm Medical, Kinova Inc., Broda Seating, and Vayyar Imaging. Companies operating in the North America elderly care products market are focusing on continuous product innovation to strengthen their competitive position and address the evolving needs of aging consumers. Businesses are investing in research and development to improve product quality, functionality, comfort, and ease of use while incorporating advanced technologies into their offerings. Many manufacturers are expanding their product portfolios to serve a broader customer base and capture additional market opportunities. Strategic partnerships, distribution network expansion, and collaborations with healthcare providers are helping companies improve market reach and customer accessibility. Organizations are also increasing investments in manufacturing capabilities and supply chain optimization to ensure consistent product availability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Care type

- 2.2.4 End use

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapidly aging population

- 3.2.1.2 Shift toward home-based care

- 3.2.1.3 Expanding healthcare spending

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of advanced products

- 3.2.2.2 Regulatory compliance & approvals

- 3.2.3 Opportunities

- 3.2.3.1 Smart home integration for elderly care

- 3.2.3.2 Expansion of remote patient monitoring (RPM)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 North America (FDA - medical device classifications & OTC pathways)

- 3.4.2 Global reimbursement policies & coverage landscape

- 3.5 Pricing analysis (driven by primary research)

- 3.5.1 Historical price trend analysis (2022-2025)

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Trade data analysis (driven by paid database)

- 3.6.1 Import/export volume & value trends

- 3.6.2 Key trade corridors & tariff impact

- 3.7 Impact of AI & generative AI on the market

- 3.7.1 AI-driven disruption of existing business models

- 3.7.2 GenAI use cases & adoption roadmap by segment

- 3.7.3 Risks, limitations & regulatory considerations

- 3.8 Treatment infrastructure & clinical adoption landscape (driven by primary research)

- 3.8.1 Facility & treatment center distribution by region

- 3.8.2 Adoption readiness by care setting & payer type

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Mobility products

- 5.2.1 Wheelchairs (manual & powered)

- 5.2.2 Walkers & rollators

- 5.2.3 Mobility scooters

- 5.2.4 Canes & crutches

- 5.2.5 Stair lifts & hoists

- 5.3 Bathroom safety products

- 5.3.1 Grab bars & handrails

- 5.3.2 Shower chairs & bath seats

- 5.3.3 Commode chairs

- 5.3.4 Toilet seat raisers & accessories

- 5.4 Comfort care products

- 5.4.1 Adjustable beds & pressure-relief mattresses

- 5.4.2 Heating pads & therapeutic wraps

- 5.4.3 Fall protection pads & bed rails

- 5.4.4 Riser recliner chairs & assistive furniture

- 5.5 Medical devices

- 5.5.1 Hearing aids & assistive listening devices

- 5.5.2 Blood pressure & cardiac monitoring devices

- 5.5.3 Blood glucose monitors

- 5.5.4 Pulse oximeters & respiratory aids

- 5.5.5 Remote patient monitoring (RPM) systems

- 5.6 Incontinence products

- 5.6.1 Incontinence pads & liners

- 5.6.2 Absorbent underwear & adult diapers

- 5.6.3 Underpads & bed protectors

- 5.6.4 External catheters & urinary sheaths

- 5.7 Nutritional supplements

- 5.7.1 Multi-vitamin & mineral combinations

- 5.7.2 Protein & meal replacement supplements

- 5.7.3 Dietary fiber & digestive health products

- 5.7.4 Food thickeners & dysphagia management products

- 5.8 Daily living aids & others

- 5.8.1 Adaptive kitchen & eating utensils

- 5.8.2 Dressing & grooming aids

- 5.8.3 Vision & communication aids

- 5.8.4 Smart home safety & emergency alert devices

Chapter 6 Market Estimates and Forecast, By Care Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Home care & independent living support

- 6.3 Chronic disease management

- 6.4 Post-acute rehabilitation care

- 6.5 Palliative & end-of-life care

- 6.6 Preventive health management

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Home-based care

- 7.3 Hospitals & clinics

- 7.4 Nursing homes & skilled nursing facilities

- 7.5 Assisted living & continuing care retirement communities (CCRCS)

- 7.6 Adult day care & rehabilitation centers

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Offline

- 8.2.1 Pharmacies & medical supply stores

- 8.2.2 Specialty durable medical equipment (DME) retailers

- 8.2.3 Hospital & institutional procurement

- 8.3 Online

- 8.3.1 E-commerce websites

- 8.3.2 Brand websites

Chapter 9 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 U.S.

- 9.3 Canada

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Invacare Corporation

- 10.1.2 Medline Industries

- 10.1.3 Stryker Corporation

- 10.1.4 Arjo

- 10.1.5 Essity

- 10.1.6 Kimberly-Clark

- 10.1.7 Abbott Nutrition

- 10.2 Regional players

- 10.2.1 Drive Medical

- 10.2.2 Graham-Field Health Products

- 10.2.3 Carex Health Brands

- 10.2.4 Dynarex Corporation

- 10.2.5 Enovis Corporation

- 10.2.6 First Quality Enterprises

- 10.2.7 EZ-ACCESS

- 10.3 Emerging players

- 10.3.1 Medical Guardian

- 10.3.2 Stander Inc.

- 10.3.3 Silverts Adaptive Clothing & Footwear

- 10.3.4 Bay Alarm Medical

- 10.3.5 Kinova Inc.

- 10.3.6 Broda Seating

- 10.3.7 Vayyar Imaging