PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083252

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083252

Hydroponic System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

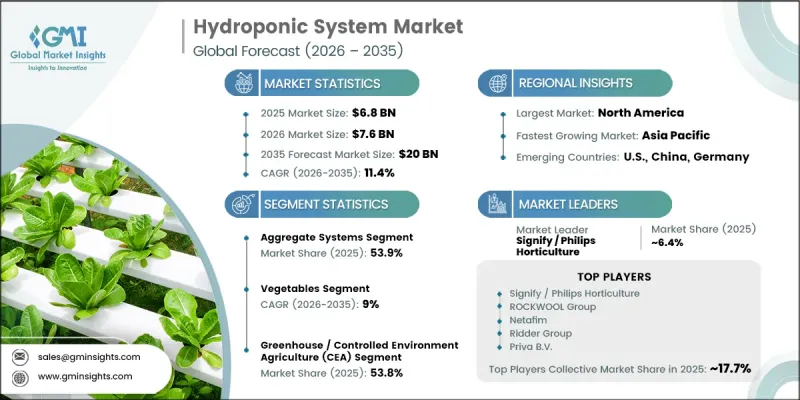

The Global Hydroponic System Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 11.4% to reach USD 20 billion by 2035.

The hydroponic system industry is witnessing strong momentum as agricultural producers increasingly seek efficient and sustainable cultivation methods capable of addressing modern food production challenges. Market expansion is being supported by the ongoing reduction in available arable land, rising consumer preference for pesticide-free produce, and the growing need for year-round crop production. In addition, hydroponic cultivation offers substantial water-saving benefits compared with conventional farming techniques, making it an attractive solution in regions facing water scarcity. Continuous advancements in controlled-environment agriculture technologies are further accelerating market growth. The integration of smart monitoring systems, automated nutrient delivery platforms, energy-efficient lighting solutions, and precision agriculture technologies is helping growers improve productivity while reducing operational costs. Hydroponic systems can deliver significantly higher yields per unit area than traditional cultivation methods, enhancing their commercial appeal across various crop categories. Growing investments in indoor farming and urban agriculture initiatives are further contributing to market development. Increasing awareness regarding food security, sustainable farming practices, and high-quality fresh produce is expected to continue supporting long-term growth opportunities across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $20 Billion |

| CAGR | 11.4% |

The hydroponic systems market is increasingly benefiting from the expansion of controlled-environment agriculture projects designed to improve food production efficiency. As concerns surrounding agricultural land availability intensify, hydroponic cultivation is gaining wider acceptance as a practical alternative to conventional farming. Government initiatives and private-sector investments focused on enhancing food security and agricultural sustainability are creating favorable conditions for market expansion. Rising demand for clean-label produce free from pesticide residues is also encouraging commercial growers to adopt hydroponic production systems that can support premium pricing and consistent product quality throughout the year.

The aggregate systems accounted for 53.9% share in 2025 and is expected to grow at a CAGR of 11.2% through 2035. The segment continues to lead the market due to its operational reliability, flexibility, and compatibility with a wide range of crops. Aggregate-based growing systems utilize inert substrates that provide stable root support while allowing growers to precisely manage nutrient and water delivery. Their adaptability to commercial greenhouse operations and large-scale agricultural facilities has contributed significantly to their widespread adoption across major cultivation regions.

The vegetables segment held a 42% share in 2025 and advancing at a CAGR of 9% through 2035. The segment benefits from established cultivation techniques, strong commercial demand, and extensive agronomic knowledge supporting efficient production practices. Hydroponic vegetable cultivation continues to gain traction among growers due to its ability to deliver consistent yields, high-quality produce, and reliable year-round supply. Strong demand from retail and foodservice channels further reinforces the segment's leading position within the market.

North America Hydroponic System Market held 32.8% share in 2025. Regional growth is supported by well-developed greenhouse infrastructure, increasing adoption of controlled-environment agriculture technologies, and strong distribution networks for fresh produce. The region continues to benefit from growing investments in indoor farming, urban agriculture projects, and advanced cultivation technologies designed to improve productivity and resource efficiency. Favorable market conditions and increasing consumer demand for sustainably grown food products are expected to support continued market expansion across North America.

Key companies operating in the global hydroponic systems market include Signify/Philips Horticulture (including Fluence), Netafim (Orbia Precision Agriculture), ROCKWOOL Group/Grodan, Priva B.V., and Ridder Group. Companies active in the hydroponic systems market are focusing on technology innovation, strategic partnerships, and product development to strengthen their competitive position and expand market presence. Manufacturers are investing in advanced automation platforms, intelligent monitoring systems, and precision nutrient management solutions to improve operational efficiency and crop productivity. Many companies are also expanding their geographic footprint through collaborations with commercial growers, greenhouse operators, and agricultural technology providers. Product portfolio diversification remains a key strategy, with businesses introducing integrated cultivation systems tailored to varying crop requirements and production scales.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 System type

- 2.2.3 Crop type

- 2.2.4 Growing environment type

- 2.2.5 End user

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Input suppliers

- 3.1.2 System & equipment manufacturers

- 3.1.3 Distributors & retailers

- 3.1.4 End users

- 3.1.5 Profit margin

- 3.1.6 Value addition at each stage

- 3.1.7 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shrinking arable land & rising global food security concerns

- 3.2.1.2 Growing consumer demand for pesticide-free, year-round fresh produce

- 3.2.1.3 Superior water-use efficiency of hydroponic systems vs. Conventional agriculture

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High initial capital investment & infrastructure setup costs

- 3.2.2.2 Elevated energy consumption for artificial lighting & climate control

- 3.2.3 Market Opportunities

- 3.2.3.1 Integration of AI, IoT & automation for cost reduction & yield optimization

- 3.2.3.2 Rising cannabis cultivation driving hydroponic system adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Emerging automation technologies in hydroponic systems

- 3.4.2 IoT-enabled monitoring & control advancements

- 3.4.3 LED lighting innovations & energy efficiency trends

- 3.5 Regulatory framework

- 3.5.1 Food safety & organic certification standards

- 3.5.2 Water use & environmental compliance regulations

- 3.5.3 Cannabis cultivation regulations by jurisdiction

- 3.5.4 Country-level agricultural support policies & subsidies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis by product category

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7 Supply chain analysis

- 3.7.1 Raw material sourcing

- 3.7.2 Equipment manufacturing & assembly landscape

- 3.7.3 Distribution network & last-mile logistics

- 3.7.4 Supply chain vulnerabilities & risk mitigation

- 3.8 Trade data analysis (driven by paid database) (HS Code 8436.80.90)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact on system components

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of traditional growing operations & business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations for AI in controlled environment agriculture

- 3.10 Capacity & production landscape (driven by primary research)

- 3.10.1 Installed capacity by region & key producer

- 3.10.2 Capacity utilization rates & expansion pipelines across major growing hubs

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Aggregate systems

- 5.2.1 Drip systems

- 5.2.2 Ebb & flow (flood & drain) systems

- 5.3 Wick systems

- 5.3.1 Liquid systems

- 5.3.2 Deep water culture (DWC)

- 5.3.3 Nutrient film technique (NFT)

- 5.3.4 Aeroponics

Chapter 6 Market Estimates and Forecast, By Crop type, 2022 - 2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Vegetables

- 6.2.1 Tomatoes

- 6.2.2 Lettuce & leafy greens

- 6.2.3 Cucumbers

- 6.2.4 Peppers

- 6.3 Herbs & microgreens

- 6.3.1 Basil & culinary herbs

- 6.3.2 Microgreens & sprouts

- 6.4 Fruits

- 6.4.1 Strawberries & berries

- 6.4.2 Melons & other fruits

- 6.5 Flowers & ornamentals

- 6.6 Others (cannabis & specialty crops)

Chapter 7 Market Estimates and Forecast, By Growing Environment, 2022 - 2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Indoor vertical farming

- 7.2.1 Multi-tier fully artificial-lit facilities

- 7.2.2 Containerized & modular farming units

- 7.3 Greenhouse / controlled environment agriculture (CEA)

- 7.3.1 Commercial greenhouses (natural + supplemental light)

- 7.3.2 Research & institutional greenhouses

- 7.4 Outdoor / open-air hydroponic systems

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Commercial growers & greenhouse enterprises

- 8.3 Urban vertical farm operators

- 8.4 Institutional & research facilities

- 8.5 Residential / home growers

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Priva B.V.

- 10.1.2 Ridder Group

- 10.1.3 Netafim (Orbia)

- 10.1.4 ROCKWOOL Group / Grodan

- 10.1.5 Signify / Philips Horticulture

- 10.1.6 Fluence

- 10.1.7 Hoogendoorn Growth Management

- 10.1.8 American Hydroponics

- 10.2 Regional Players

- 10.2.1 Artechno Growsystems

- 10.2.2 KG Systems

- 10.2.3 Urban Crop Solutions

- 10.2.4 Argus Control Systems

- 10.2.5 Dosatron International

- 10.2.6 Gavita (Hawthorne / Vireo Growth)

- 10.2.7 STARFARM

- 10.2.8 Lyine Group

- 10.2.9 Intelligent Growth Solutions (IGS)

- 10.3 Emerging brands

- 10.3.1 Growcer (+ Freight Farms assets)

- 10.3.2 ZipGrow Inc.

- 10.3.3 Valoya

- 10.3.4 OnePointOne (OPO)