PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083345

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083345

Thin Film Semiconductor Deposition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

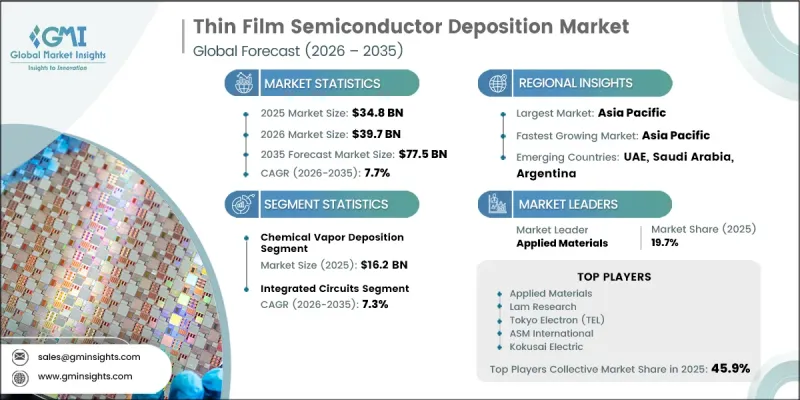

The Global Thin Film Semiconductor Deposition Market was valued at USD 34.8 billion in 2025 and is estimated to grow at a CAGR of 7.7% to reach USD 77.5 billion by 2035.

Growth is reinforced by the rapid expansion of artificial intelligence workloads, government-led semiconductor sovereignty programs, and the accelerating shift toward advanced process nodes that depend on ultra-precise atomic-level film deposition. Demand is increasingly concentrated in leading-edge logic and memory manufacturing, where chemical, physical, and atomic layer deposition techniques directly influence yield performance at sub-5nm geometries. The market is also supported by diversified end-use adoption across AI accelerators, automotive electronics, advanced memory architectures, and next-generation renewable energy devices, reinforcing a multi-industry demand base. Rising hyperscale data center deployment and cloud infrastructure expansion are further intensifying the requirement for high-performance chips, each of which requires multiple deposition cycles during fabrication. In addition, modern memory technologies such as advanced 3D NAND now involve more than 200 stacked layers, with each layer requiring repeated deposition and etching steps to maintain structural precision. This increasing process complexity continues to elevate equipment intensity per wafer, strengthening long-term demand visibility across the semiconductor deposition ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $34.8 Billion |

| Forecast Value | $77.5 Billion |

| CAGR | 7.7% |

The chemical vapor deposition segment generated USD 16.2 billion in 2025. Its dominance is supported by broad applicability across dielectric layers, conductive fills, barrier coatings, and high-density plasma processes across multiple semiconductor nodes. Strong adoption across both mature and advanced fabrication environments continues to reinforce its critical role in device manufacturing.

The integrated circuits segment accounted for USD 25.1 billion in 2025, representing 72% share. Deposition steps across IC manufacturing include dielectric formation, insulation layers, and metallization structures form the backbone of semiconductor production. Demand is particularly strong in advanced logic and high-density memory architectures, where escalating design complexity requires significantly higher deposition intensity per chip.

North America Thin Film Semiconductor Deposition Market accounted for USD 10.8 billion in 2025, capturing 31.1% share. Growth in the region is strongly centered in the United States, supported by large-scale policy initiatives and private sector expansion of semiconductor fabrication facilities across multiple states, strengthening domestic production capacity and supply chain resilience.

The competitive landscape includes leading equipment and technology providers such as Applied Materials Inc., Lam Research Corporation, Tokyo Electron Limited, ASM International N.V., Kokusai Electric Corporation, NAURA Technology Group, Veeco Instruments Inc., Aixtron SE, SVT Associates, Semicore Equipment Inc., Denton Vacuum, PSR Semi, KDF Electronic & Vacuum Services, Yunmao Technology, and ZLD Technology. Companies in the thin film semiconductor deposition market are strengthening their position through continuous investment in next-generation deposition technologies that improve atomic-level precision and process uniformity. Many firms are expanding product portfolios to support advanced nodes such as sub-5nm and high-aspect-ratio 3D architectures, where process control is increasingly critical. Strategic partnerships with semiconductor fabs and foundries are being prioritized to secure long-term equipment supply agreements and co-development programs. Manufacturers are also focusing on automation, AI-driven process control, and predictive maintenance capabilities to reduce downtime and improve yield performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Deposition Technology trends

- 2.1.2 Application trends

- 2.1.3 End use trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for AI and High-Performance Computing Chips

- 3.2.1.2 Continuous Miniaturization of Semiconductor Devices

- 3.2.1.3 Expansion of Global Semiconductor Manufacturing Facilities

- 3.2.1.4 Increasing Production of Advanced Memory and Power Semiconductors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Capital and Operational Costs of Deposition Equipment

- 3.2.2.2 Rapid Technological Evolution in Semiconductor Manufacturing

- 3.2.3 Market opportunities

- 3.2.3.1 Growing Adoption of Advanced Packaging Technologies

- 3.2.3.2 Expanding Use of Compound Semiconductors and Emerging Materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing trend analysis (Driven by primary research)

- 3.7 Future market trends

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Impact of AI and Generative AI on the market (Driven by primary research)

- 3.12 Value chain analysis (Driven by primary research)

- 3.13 Investment & funding analysis (Driven by primary research)

- 3.14 Consumer insights (Driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Deposition Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Chemical Vapor Deposition (CVD)

- 5.2.1 Atmospheric Pressure CVD (APCVD)

- 5.2.2 Low Pressure CVD (LPCVD)

- 5.2.3 Plasma Enhanced CVD (PECVD)

- 5.2.4 Other CVD Variants

- 5.3 Physical Vapor Deposition (PVD)

- 5.3.1 Sputtering

- 5.3.2 Evaporation

- 5.3.3 Other PVD Techniques

- 5.4 Atomic Layer Deposition (ALD)

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Integrated Circuits (ICs)

- 6.2.1 Microprocessors

- 6.2.2 Memory Devices (DRAM, NAND, NOR)

- 6.2.3 Others

- 6.3 Optoelectronics & Display Devices

- 6.3.1 LED Displays

- 6.3.2 OLED Panels

- 6.3.3 LCD Screens

- 6.3.4 Others

- 6.4 Solar Cells/Photovoltaics

- 6.4.1 Thin Film Solar Panels

- 6.4.2 Crystalline Silicon Solar Cells

- 6.4.3 Others

- 6.5 MEMS & Sensors

- 6.5.1 Pressure Sensors

- 6.5.2 Inertial Sensors (Accelerometers, Gyroscopes)

- 6.5.3 Optical Sensors

- 6.5.4 Others

- 6.6 Others

Chapter 7 Market Size and Forecast, By End User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Consumer Electronics

- 7.2.1 Smartphones & Tablets

- 7.2.2 Laptops & Computing Devices

- 7.2.3 Others

- 7.3 Automotive

- 7.3.1 Electric Vehicles (EVs) & Battery Management Systems

- 7.3.2 Advanced Driver Assistance Systems (ADAS)

- 7.3.3 Others

- 7.4 Energy & Power

- 7.4.1 Solar Energy Systems

- 7.4.2 Power Electronics & Converters

- 7.4.3 Others

- 7.5 Aerospace & Defense

- 7.5.1 Military Electronics & Communication Systems

- 7.5.2 Aerospace Components & Avionics

- 7.5.3 Others

- 7.6 Communication & Technology

- 7.6.1 Telecommunications Infrastructure

- 7.6.2 Data Centers & Cloud Computing

- 7.6.3 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Netherlands

- 8.3.5 Spain

- 8.3.6 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Mexico

Chapter 9 Company Profiles

- 9.1 Applied Materials Inc.

- 9.2 Lam Research Corporation

- 9.3 Tokyo Electron Limited (TEL)

- 9.4 ASM International N.V.

- 9.5 Kokusai Electric Corporation

- 9.6 NAURA Technology Group

- 9.7 Veeco Instruments Inc.

- 9.8 Aixtron SE

- 9.9 SVTA (SVT Associates)

- 9.10 Semicore Equipment Inc.

- 9.11 Denton Vacuum

- 9.12 PSR Semi

- 9.13 KDF Electronic & Vacuum Services

- 9.14 Yunmao Technology

- 9.15 ZLD Technology