PUBLISHER: Industry Experts | PRODUCT CODE: 1767030

PUBLISHER: Industry Experts | PRODUCT CODE: 1767030

Global Application Development Software Market - Applications, Platforms, Deployment Types, Company Types and Industry Sectors

Global Application Development Software Market Trends and Outlook

| Key Metrics | |

|---|---|

| Historical Period: | 2021-2023 |

| Base Year: | 2024 |

| Forecast Period: | 2024-2030 |

| Units: | Value market in US$ |

| Companies Mentioned: | 26 |

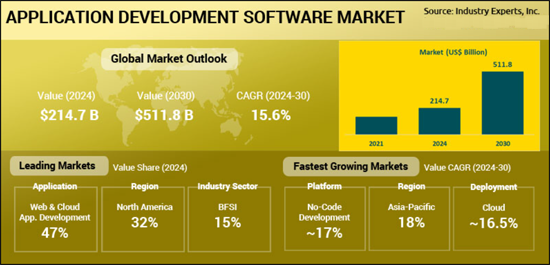

The global Application Development Software market stands at roughly US$214.6 billion in 2024 and, expanding at an estimated 15.6% CAGR, is poised to surpass US$511.8 billion by 2030. Demand is propelled by enterprise digital?transformation initiatives in banking, energy, healthcare, and other sectors that require bespoke solutions to elevate efficiency and customer engagement. Rising smartphone penetration, e-commerce momentum, and mobile banking adoption amplify the call for high-quality mobile apps. Low-code and no-code platforms empower "citizen developers," compressing development cycles and cutting costs, while cloud-native architectures spanning microservices, containerization, and serverless-deliver scalability and facilitate remote collaboration. Agile and DevOps practices embed continuous integration and delivery, and AI/ML additions automate testing, offer intelligent code suggestions, and flag defects early. Hybrid deployment needs and increasingly data-rich workloads also sustain demand for flexible, integration-friendly toolsets.

INFOGRAPHICS

Among the array of market trends influencing the global demand for Application Development Software, the growth in low-code and no-code platforms is a crucial component. An increase in the adoption of such platforms has expedited application development with negligible coding expertise. By using these platforms, non-developers and citizen developers can create applications using visual interfaces, which reduces development time and costs. Another notable trend has been the integration of AI-driven tools into development processes for automating repetitive tasks, enhancing code quality and providing predictive analytics for better user experiences. Estimates suggest that more than 80% of development teams are in line to use AI tools by 2025. Scalability, cost-efficiency and support for remote collaboration are providing cloud-native applications and cloud-based development environments with the requisite traction, making cloud deployment predominate the market.

Application Development Software Regional Market Analysis

North America captures 32.2 % of 2024 ADS revenue, powered by expansive cloud capacity, hefty R&D budgets, and over 90 % of enterprises mid-digital-transformation, driving demand for AI-ready toolchains, low-code suites, and mission-critical cloud IDEs with nonstop CI/CD; federal tax credits, state grants, and hyperscaler M&A from API-security acquisitions to generative-AI coding bots-keep innovation capital flowing, cementing the region as the command center for next-generation application development. Asia-Pacific, however, is the fastest climber, advancing at about 18 % CAGR through 2030 as government mega-programs across China, India, and ASEAN pour billions into cloud, mobile, and digital infrastructure; with nearly two billion smartphone users, flourishing e-commerce and fintech ecosystems, and innovation hubs like Bengaluru and Singapore spawning low-code/no-code tools that let resource-constrained SMBs leapfrog talent gaps, vendors delivering multilingual, localized, AI-driven suites are poised to capture the region's outsized incremental demand.

Application Development Software Market Analysis by Application

Web & cloud application development accounts for 47.3 % of 2024 ADS demand, reflecting enterprises' shift to scalable, pay-as-you-go infrastructure that trims hardware outlays and lets teams spin resources up or down with minimal friction. Continuous-integration pipelines, microservices, and browser-based access accelerate release cycles and support global collaboration, while built-in AI, ML, IoT, and big-data hooks enable highly tailored, feature-rich apps. By contrast, mobile application development will register the fastest 2024-2030 CAGR at 16.4 % as soaring smartphone penetration and 5G connectivity push businesses toward "mobile-first" engagement. Native apps outshine mobile web with push notifications, device integration, and offline use, boosting conversion rates and loyalty for banking, shopping, and entertainment. Ongoing advances in handset power, AR/VR, and edge AI, coupled with low-code/no-code platforms that let non-technical teams cut development time by up to 80 %, are opening new revenue streams via in-app purchases, subscriptions, and advertising.

Application Development Software Market Analysis by Platform Type

Web & cloud development dominates the Application Development Software landscape, capturing about 47.3 % of 2024 revenue. Its lead stems from on-demand scalability, pay-as-you-go economics, CI/CD-driven release velocity, and tight integration with AI, IoT, and big-data services-features that align with enterprise digital-transformation goals. In contrast, mobile application development, fueled by worldwide smartphone penetration, 5G roll-outs, and a shift to "mobile-first" strategies, is the fastest-advancing segment and is projected to grow at roughly 16.4 % annually through 2030. Low-code/no-code tools, richer device capabilities, and strong monetization pathways (in-app purchases, subscriptions, ads) further accelerate mobile uptake, positioning it as the primary engine of incremental demand even as web & cloud platforms remain the market's operational backbone.

Application Development Software Market Analysis by Deployment Type

Cloud deployment drives roughly 60.6 % of 2024 application-development-software revenue and is projected to grow around 16.5 % annually through 2030. Nearly nine in ten organizations now build in the cloud, drawn by 20-30 % lower up-front and operating costs versus on-premises setups, elastic scaling that absorbs volatile e-commerce and streaming traffic, and native hooks into AI/ML, IoT, microservices, and container technologies such as Kubernetes and Docker. Industries with tight regulatory oversight-finance, healthcare, retail-lean on providers' built-in encryption and GDPR, HIPAA, and SOC 2 compliance, further cementing the cloud as the preferred launch pad for sophisticated, data-intensive applications.

Application Development Software Market Analysis by Company Type

Large enterprises, those topping US$1 billion in annual revenue-drive roughly 57.1 % of 2024 Application Development Software spending, leveraging deep IT budgets, enterprise-wide digital-transformation mandates, and a preference for feature-rich, cloud-based platforms that integrate DevSecOps, AI, and microservices while meeting stringent GDPR, HIPAA, and SOC 2 requirements. Small and midsize companies, although a smaller slice today, represent the market's fastest-growing cohort, projected to expand about 17.1 % per year through 2030 as cost-sensitive firms turn to low-code/no-code and pay-as-you-go cloud tools to accelerate customer-facing app launches, slash development cycles by up to 80 %, and offset developer shortages especially across rapidly digitizing sectors like e-commerce and fintech in Asia-Pacific.

Application Development Software Market Analysis by Industry Sector

Banking, Financial Services & Insurance (BFSI) remains the largest consumer of application-development software, absorbing roughly 15.3 % of global spend in 2024 as institutions safeguard massive volumes of sensitive data, navigate GDPR/KYC/AML mandates, and meet rising expectations for mobile banking, digital wallets, and real-time payments with secure, AI-enhanced, API-rich platforms spanning fraud-detection engines, blockchain rails, and personalized chatbots; meanwhile, the Energy & Utilities sector is set to be the fastest mover, projected to expand at about 18.9 % annually through 2030 as electrification, data-center power loads, distributed energy-resource integration, and net-zero commitments drive adoption of cloud-based, IoT-enabled applications for smart-grid control, real-time monitoring, predictive maintenance, renewable integration, carbon tracking, and workforce optimization making it the market's most dynamic engine of incremental demand.

Application Development Software Market Report Scope

This global report on Application Development Software analyzes the global and regional markets based on application, platform, deployment, company type and industry sector for the period 2021-2030 with projections from 2024 to 2030 in terms of value in US$. In addition to providing profiles of major companies operating in this space, the latest corporate and industrial developments have been covered to offer a clear panorama of how and where the market is progressing.

Application Development Software Market by Geographic Region

- North America (The United States, Canada and Mexico)

- Europe (Germany, the United Kingdom, France, Italy, the Netherlands, Spain, Russia, Switzerland and Rest of Europe)

- Asia-Pacific (China, Japan, India, Australia, Singapore, South Korea and Rest of Asia-Pacific)

- South America (Brazil, Argentina, Colombia, Chile, Peru and Rest of South America)

- Middle East & Africa (The United Arab Emirates, South Africa, Egypt, Saudi Arabia, Morocco, Kuwait, Qatar and Rest of Middle East & Africa)

Application Development Software Market by Application

- Web & Cloud Application Development

- Mobile Application Development

- Desktop Application Development

Application Development Software Market by Platform

- Low-Code Development

- No-Code Development

Application Development Software Market by Deployment

- Cloud

- On-Premise

Application Development Software Market by Company Type

- Large

- Small & Medium

Application Development Software Market by Industry Sector

- BFSI

- IT & Communication

- Retail & Ecommerce

- Manufacturing

- Healthcare & Life Sciences

- Energy & Utilities

- Government

- Transportation

- Construction

- Tourism & Hospitality

- Others

Major Market Players:

|

|

TABLE OF CONTENTS

PART A: GLOBAL MARKET PERSPECTIVE

1. EXECUTIVE SUMMARY

- 1.1. A Roundup on Application Development Software

- 1.1.1. Market Segmentation for Application Development Software

- 1.1.1.1. Application Types

- 1.1.1.2. Platform Types

- 1.1.1.3. Deployment Types

- 1.1.1.4. Company Types

- 1.1.1.5. Industry Sectors

- 1.1.2. Key Trends in Application Development Software Market

- 1.1.2.1. Mobile Application Development Fuels Demand for Application Development Software

- 1.1.2.2. Custom Software Development Driving Tailored Digital Transformation

- 1.1.2.3. Cloud-Native Momentum: How Scalability, Serverless and AI Are Redefining Application Development

- 1.1.2.4. Enterprise Application Integration Evolves for the Cloud-Native, API-First Era

- 1.1.2.5. Rearchitecting Legacy Systems into Cloud-Native Microservices

- 1.1.1. Market Segmentation for Application Development Software

2. INDUSTRY LANDSCAPE

- 2.1. Application Development Software Market Outlook

- 2.1.1. Comprehensive Application Development Software Industry Analysis - Growth Drivers and Inhibitors

- 2.1.1.1. Growth Drivers

- 2.1.1.2. Inhibitors

- 2.1.1. Comprehensive Application Development Software Industry Analysis - Growth Drivers and Inhibitors

- 2.2. Entry Strategies for Application Development Software Industry

- 2.2.1. Pre-Market Entry Strategies

- 2.2.1.1. Identify and Own an Underserved Niche

- 2.2.1.2. Forge Strategic Alliances for Credibility and Reach

- 2.2.1.3. Leverage Cost-Advantaged Talent Hubs and Flexible Pricing

- 2.2.1.4. Differentiate Through Emerging Technologies

- 2.2.1.5. Build Visibility via Marketing, Community, and Funding

- 2.2.2. Post-Market Entry Strategies

- 2.2.2.1. Capitalizing on AI-Driven Development

- 2.2.2.2. Low-Code/No-Code Platforms for Citizen Developers

- 2.2.2.3. Blockchain Solutions for High-Security Workflows

- 2.2.2.4. IoT-Enabled Applications Across Industries

- 2.2.2.5. Niche Vertical and SME Opportunities

- 2.2.2.6. Cloud-Native Services, APIs and DevOps Tooling

- 2.2.2.7. Cost-Effective Talent and the Gig-Economy Edge

- 2.2.2.8. Automation of Testing, Debugging and Deployment

- 2.2.2.9. Strategic Alliances with Major Tech Ecosystems

- 2.2.2.10. Government Digital-Transformation and RegTech Niches

- 2.2.1. Pre-Market Entry Strategies

- 2.3. SWOT Analysis of Application Development Software Industry

- 2.3.1. Strengths

- 2.3.2. Weaknesses

- 2.3.3. Opportunities

- 2.3.4. Threats

- 2.4. Porter's Five Forces Analysis

- 2.5. PESTEL Analysis

3. COMPETITIVE LANDSCAPE

- 3.1. Market Positioning of Key Companies

- 3.1.1. Microsoft Corporation

- 3.1.2. Amazon Web Services, Inc (AWS)

- 3.1.3. Google LLC

- 3.1.4. Oracle Corporation

- 3.1.5. Salesforce, Inc

- 3.1.6. SAP SE

- 3.1.7. Adobe Inc

- 3.2. Market Share Analysis of Application Development Software

- 3.3. Key Market Players

- 3.3.1. Accenture PLC

- 3.3.2. Adobe Inc.

- 3.3.3. Amazon Web Services, Inc.

- 3.3.4. Atos SE

- 3.3.5. Capgemini Services SAS

- 3.3.6. Cognizant Technology Solutions Corp.

- 3.3.7. Fujitsu Ltd.

- 3.3.8. Google LLC

- 3.3.9. HCL Technologies Ltd.

- 3.3.10. Hewlett Packard Enterprise Co.

- 3.3.11. Infosys Ltd.

- 3.3.12. International Business Machines Corp. (IBM)

- 3.3.13. L&T Technology Services Limited

- 3.3.14. Mendix Technology B.V.

- 3.3.15. Microsoft Corporation

- 3.3.16. Mindteck India Ltd.

- 3.3.17. NTT DATA Corp.

- 3.3.18. Oracle Corporation

- 3.3.19. OutSystems

- 3.3.20. RSM International Ltd.

- 3.3.21. Salesforce, Inc

- 3.3.22. SAP SE

- 3.3.23. TATA Consultancy Services Ltd.

- 3.3.24. Tech Mahindra Ltd

- 3.3.25. Unisys Corp.

- 3.3.26. Wipro Ltd.

4. KEY BUSINESS & PRODUCT TRENDS

- 4.1. June 2025

- 4.1.1. Salesforce Unveils Upgraded Agentforce 3

- 4.2. April 2025

- 4.2.1. Infosys Extends its Collaboration with AIB

- 4.2.2. AWS Unveils Enhanced Amazon Q Developer Agent

- 4.2.3. Google Unveils New Capabilities to Support Application Lifecycle

- 4.3. March 2025

- 4.3.1. NTT Data and UPS Announce their Strategic Collaboration

- 4.3.2. L&T Technology Services Unveils TrackEi(TM)

- 4.3.3. SAP SE Announces Joule for Developers

- 4.3.4. Tech Mahindra and Google Cloud Extend Collaboration to Power Enterprise AI Innovation and Digital Growth

- 4.3.5. Atos and Esri France Announce Collaboration

- 4.4. February 2025

- 4.4.1. TCS Extends Strategic Partnership with DNB Bank to Drive Digital Modernization and Innovation

- 4.4.2. Fujitsu Unveils Fujitsu Cloud Service Generative AI Platform

- 4.4.3. KBC Group Extends Partnership with Cognizant

- 4.5. January 2025

- 4.5.1. OutSystems Announces Availability of Mentor

- 4.6. December 2024

- 4.6.1. Wipro Announces Acquisition of AVT

- 4.7. November 2024

- 4.7.1. L&T Technology Services Acquires Intelliswift, Deepens Software Product Development, Platform Engineering & AI Expertise

- 4.7.2. Cognizant Unveils Extensions of Cognizant-R Skygrade(TM) and Flowsource(TM) platforms

- 4.7.3. Accenture and du Announce Collaboration

- 4.8. October 2024

- 4.8.1. Fujitsu Unveils AI-Powered Application to Enhance Mobile Network Quality and Energy Efficiency

- 4.9. September 2024

- 4.9.1. Oracle Unveils New Capabilities

- 4.9.2. HPE Launches Instant-Deploy AI Apps with HPE Private Cloud AI

- 4.10. July 2024

- 4.10.1. Atos Powers UEFA EURO 2024(TM) with Advanced IT Solutions

- 4.10.2. AWS Announces Availability of AWS App Studio in Preview

- 4.11. June 2024

- 4.11.1. TCS Announces Launch of TCS AI WisdomNext(TM)

- 4.11.2. Mendix Announces Availability of Mendix 10.12.

- 4.11.3. Rackspace Technology and Mendix Enter into a Strategic Partnership

- 4.12. May 2024

- 4.12.1. Fujitsu Develops Learning Language Models under GENIAC Project

- 4.12.2. NTT DATA to Enhance and Manage Comprehensive Application Landscape of Salesforce

- 4.13. April 2024

- 4.13.1. Capgemini Signs Multiyear Deal with Valmet to Modernize IT Operations and Strengthen Business Agility

- 4.13.2. Cloud Software Group Inc. and Microsoft Corp Announce Strategic Partnership

- 4.14. March 2024

- 4.14.1. Cognizant and Google Cloud Extend Partnership to Boost Software Development Productivity

- 4.15. February 2024

- 4.15.1. LTTS and BlackBerry Partner to Accelerate Development of SDVs for Global OEMs

- 4.16. January 2024

- 4.16.1. IBM Announces Acquisition of Application Modernization Capabilities from Advanced

- 4.17. September 2023

- 4.17.1. Oracle Unveils New Application Development Capabilities

- 4.17.2. Gati and Tech Mahindra Partner for Application Development

- 4.18. June 2023

- 4.18.1. Accenture Acquires Bourne Digital

5. GLOBAL MARKET OVERVIEW

- 5.1. Global Application Development Software Market Overview by Application

- 5.1.1. Application Development Software Application Market Overview by Global Region

- 5.1.1.1. Web & Cloud Application Development

- 5.1.1.2. Mobile Application Development

- 5.1.1.3. Desktop Application Development

- 5.1.1. Application Development Software Application Market Overview by Global Region

- 5.2. Global Application Development Software Market Overview by Platform

- 5.2.1. Application Development Software Platform Market Overview by Global Region

- 5.2.1.1. Low-Code Development

- 5.2.1.2. No-Code Development

- 5.2.1. Application Development Software Platform Market Overview by Global Region

- 5.3. Global Application Development Software Market Overview by Deployment

- 5.3.1. Application Development Software Deployment Market Overview by Global Region

- 5.3.1.1. Cloud

- 5.3.1.2. On-Premise

- 5.3.1. Application Development Software Deployment Market Overview by Global Region

- 5.4. Global Application Development Software Market Overview by Company Type

- 5.4.1. Application Development Software Company Type Market Overview by Global Region

- 5.4.1.1. Large Enterprises

- 5.4.1.2. Small & Medium Enterprises

- 5.4.1. Application Development Software Company Type Market Overview by Global Region

- 5.5. Global Application Development Software Market Overview by Industry Sector

- 5.5.1. Application Development Software Industry Sector Market Overview by Global Region

- 5.5.1.1. BFSI

- 5.5.1.2. IT & Communication

- 5.5.1.3. Retail & Ecommerce

- 5.5.1.4. Manufacturing

- 5.5.1.5. Healthcare & Life Sciences

- 5.5.1.6. Energy & Utilities

- 5.5.1.7. Government

- 5.5.1.8. Transportation

- 5.5.1.9. Construction

- 5.5.1.10. Tourism & Hospitality

- 5.5.1.11. Other Sectors

- 5.5.1. Application Development Software Industry Sector Market Overview by Global Region

PART B: REGIONAL MARKET PERSPECTIVE

REGIONAL MARKET OVERVIEW

6. NORTH AMERICA

- 6.1. North American Application Development Software Market Overview by Geographic Region

- 6.2. North American Application Development Software Market Overview by Application

- 6.3. North American Application Development Software Market Overview by Platform

- 6.4. North American Application Development Software Market Overview by Deployment

- 6.5. North American Application Development Software Market Overview by Company Type

- 6.6. North American Application Development Software Market Overview by Industry Sector

- 6.7. Country-wise Analysis of North American Application Development Software Market

- 6.7.1. THE UNITED STATES

- 6.7.1.1. United States Application Development Software Market Overview by Application

- 6.7.1.2. United States Application Development Software Market Overview by Platform

- 6.7.1.3. United States Application Development Software Market Overview by Deployment

- 6.7.1.4. United States Application Development Software Market Overview by Company Type

- 6.7.1.5. United States Application Development Software Market Overview by Industry Sector

- 6.7.2. CANADA

- 6.7.2.1. Canadian Application Development Software Market Overview by Application

- 6.7.2.2. Canadian Application Development Software Market Overview by Platform

- 6.7.2.3. Canadian Application Development Software Market Overview by Deployment

- 6.7.2.4. Canadian Application Development Software Market Overview by Company Type

- 6.7.2.5. Canadian Application Development Software Market Overview by Industry Sector

- 6.7.3. MEXICO

- 6.7.3.1. Mexican Application Development Software Market Overview by Application

- 6.7.3.2. Mexican Application Development Software Market Overview by Platform

- 6.7.3.3. Mexican Application Development Software Market Overview by Deployment

- 6.7.3.4. Mexican Application Development Software Market Overview by Company Type

- 6.7.3.5. Mexican Application Development Software Market Overview by Industry Sector

- 6.7.1. THE UNITED STATES

7. EUROPE

- 7.1. European Application Development Software Market Overview by Geographic Region

- 7.2. European Application Development Software Market Overview by Application

- 7.3. European Application Development Software Market Overview by Platform

- 7.4. European Application Development Software Market Overview by Deployment

- 7.5. European Application Development Software Market Overview by Company Type

- 7.6. European Application Development Software Market Overview by Industry Sector

- 7.7. Country-wise Analysis of European Application Development Software Market

- 7.7.1. GERMANY

- 7.7.1.1. German Application Development Software Market Overview by Application

- 7.7.1.2. German Application Development Software Market Overview by Platform

- 7.7.1.3. German Application Development Software Market Overview by Deployment

- 7.7.1.4. German Application Development Software Market Overview by Company Type

- 7.7.1.5. German Application Development Software Market Overview by Industry Sector

- 7.7.2. THE UNITED KINGDOM

- 7.7.2.1. United Kingdom Application Development Software Market Overview by Application

- 7.7.2.2. United Kingdom Application Development Software Market Overview by Platform

- 7.7.2.3. United Kingdom Application Development Software Market Overview by Deployment

- 7.7.2.4. United Kingdom Application Development Software Market Overview by Company Type

- 7.7.2.5. United Kingdom Application Development Software Market Overview by Industry Sector

- 7.7.3. FRANCE

- 7.7.3.1. French Application Development Software Market Overview by Application

- 7.7.3.2. French Application Development Software Market Overview by Platform

- 7.7.3.3. French Application Development Software Market Overview by Deployment

- 7.7.3.4. French Application Development Software Market Overview by Company Type

- 7.7.3.5. French Application Development Software Market Overview by Industry Sector

- 7.7.4. ITALY

- 7.7.4.1. Italian Application Development Software Market Overview by Application

- 7.7.4.2. Italian Application Development Software Market Overview by Platform

- 7.7.4.3. Italian Application Development Software Market Overview by Deployment

- 7.7.4.4. Italian Application Development Software Market Overview by Company Type

- 7.7.4.5. Italian Application Development Software Market Overview by Industry Sector

- 7.7.5. THE NETHERLANDS

- 7.7.5.1. Dutch Application Development Software Market Overview by Application

- 7.7.5.2. Dutch Application Development Software Market Overview by Platform

- 7.7.5.3. Dutch Application Development Software Market Overview by Deployment

- 7.7.5.4. Dutch Application Development Software Market Overview by Company Type

- 7.7.5.5. Dutch Application Development Software Market Overview by Industry Sector

- 7.7.6. SPAIN

- 7.7.6.1. Spanish Application Development Software Market Overview by Application

- 7.7.6.2. Spanish Application Development Software Market Overview by Platform

- 7.7.6.3. Spanish Application Development Software Market Overview by Deployment

- 7.7.6.4. Spanish Application Development Software Market Overview by Company Type

- 7.7.6.5. Spanish Application Development Software Market Overview by Industry Sector

- 7.7.7. RUSSIA

- 7.7.7.1. Russian Application Development Software Market Overview by Application

- 7.7.7.2. Russian Application Development Software Market Overview by Platform

- 7.7.7.3. Russian Application Development Software Market Overview by Deployment

- 7.7.7.4. Russian Application Development Software Market Overview by Company Type

- 7.7.7.5. Russian Application Development Software Market Overview by Industry Sector

- 7.7.8. SWITZERLAND

- 7.7.8.1. Swiss Application Development Software Market Overview by Application

- 7.7.8.2. Swiss Application Development Software Market Overview by Platform

- 7.7.8.3. Swiss Application Development Software Market Overview by Deployment

- 7.7.8.4. Swiss Application Development Software Market Overview by Company Type

- 7.7.8.5. Swiss Application Development Software Market Overview by Industry Sector

- 7.7.9. REST OF EUROPE

- 7.7.9.1. Rest of Europe Application Development Software Market Overview by Application

- 7.7.9.2. Rest of Europe Application Development Software Market Overview by Platform

- 7.7.9.3. Rest of Europe Application Development Software Market Overview by Deployment

- 7.7.9.4. Rest of Europe Application Development Software Market Overview by Company Type

- 7.7.9.5. Rest of Europe Application Development Software Market Overview by Industry Sector

- 7.7.1. GERMANY

8. ASIA-PACIFIC

- 8.1. Asia-Pacific Application Development Software Market Overview by Geographic Region

- 8.2. Asia-Pacific Application Development Software Market Overview by Application

- 8.3. Asia-Pacific Application Development Software Market Overview by Platform

- 8.4. Asia-Pacific Application Development Software Market Overview by Deployment

- 8.5. Asia-Pacific Application Development Software Market Overview by Company Type

- 8.6. Asia-Pacific Application Development Software Market Overview by Industry Sector

- 8.7. Country-wise Analysis of Asia-Pacific Application Development Software Market

- 8.7.1. CHINA

- 8.7.1.1. Chinese Application Development Software Market Overview by Application

- 8.7.1.2. Chinese Application Development Software Market Overview by Platform

- 8.7.1.3. Chinese Application Development Software Market Overview by Deployment

- 8.7.1.4. Chinese Application Development Software Market Overview by Company Type

- 8.7.1.5. Chinese Application Development Software Market Overview by Industry Sector

- 8.7.2. JAPAN

- 8.7.2.1. Japanese Application Development Software Market Overview by Application

- 8.7.2.2. Japanese Application Development Software Market Overview by Platform

- 8.7.2.3. Japanese Application Development Software Market Overview by Deployment

- 8.7.2.4. Japanese Application Development Software Market Overview by Company Type

- 8.7.2.5. Japanese Application Development Software Market Overview by Industry Sector

- 8.7.3. INDIA

- 8.7.3.1. Indian Application Development Software Market Overview by Application

- 8.7.3.2. Indian Application Development Software Market Overview by Platform

- 8.7.3.3. Indian Application Development Software Market Overview by Deployment

- 8.7.3.4. Indian Application Development Software Market Overview by Company Type

- 8.7.3.5. Indian Application Development Software Market Overview by Industry Sector

- 8.7.4. AUSTRALIA

- 8.7.4.1. Australia Application Development Software Market Overview by Application

- 8.7.4.2. Australia Application Development Software Market Overview by Platform

- 8.7.4.3. Australia Application Development Software Market Overview by Deployment

- 8.7.4.4. Australia Application Development Software Market Overview by Company Type

- 8.7.4.5. Australia Application Development Software Market Overview by Industry Sector

- 8.7.5. SINGAPORE

- 8.7.5.1. Singaporean Application Development Software Market Overview by Application

- 8.7.5.2. Singaporean Application Development Software Market Overview by Platform

- 8.7.5.3. Singaporean Application Development Software Market Overview by Deployment

- 8.7.5.4. Singaporean Application Development Software Market Overview by Company Type

- 8.7.5.5. Singaporean Application Development Software Market Overview by Industry Sector

- 8.7.6. SOUTH KOREA

- 8.7.6.1. South Korean Application Development Software Market Overview by Application

- 8.7.6.2. South Korean Application Development Software Market Overview by Platform

- 8.7.6.3. South Korean Application Development Software Market Overview by Deployment

- 8.7.6.4. South Korean Application Development Software Market Overview by Company Type

- 8.7.6.5. South Korean Application Development Software Market Overview by Industry Sector

- 8.7.7. REST OF ASIA-PACIFIC

- 8.7.7.1. Rest of Asia-Pacific Application Development Software Market Overview by Application

- 8.7.7.2. Rest of Asia-Pacific Application Development Software Market Overview by Platform

- 8.7.7.3. Rest of Asia-Pacific Application Development Software Market Overview by Deployment

- 8.7.7.4. Rest of Asia-Pacific Application Development Software Market Overview by Company Type

- 8.7.7.5. Rest of Asia-Pacific Application Development Software Market Overview by Industry Sector

- 8.7.1. CHINA

9. SOUTH AMERICA

- 9.1. South American Application Development Software Market Overview by Geographic Region

- 9.2. South American Application Development Software Market Overview by Application

- 9.3. South American Application Development Software Market Overview by Platform

- 9.4. South American Application Development Software Market Overview by Deployment

- 9.5. South American Application Development Software Market Overview by Company Type

- 9.6. South American Application Development Software Market Overview by Industry Sector

- 9.7. Country-wise Analysis of South American Application Development Software Market

- 9.7.1. BRAZIL

- 9.7.1.1. Brazilian Application Development Software Market Overview by Application

- 9.7.1.2. Brazilian Application Development Software Market Overview by Platform

- 9.7.1.3. Brazilian Application Development Software Market Overview by Deployment

- 9.7.1.4. Brazilian Application Development Software Market Overview by Company Type

- 9.7.1.5. Brazilian Application Development Software Market Overview by Industry Sector

- 9.7.2. ARGENTINA

- 9.7.2.1. Argentine Application Development Software Market Overview by Application

- 9.7.2.2. Argentine Application Development Software Market Overview by Platform

- 9.7.2.3. Argentine Application Development Software Market Overview by Deployment

- 9.7.2.4. Argentine Application Development Software Market Overview by Company Type

- 9.7.2.5. Argentine Application Development Software Market Overview by Industry Sector

- 9.7.3. COLOMBIA

- 9.7.3.1. Colombian Application Development Software Market Overview by Application

- 9.7.3.2. Colombian Application Development Software Market Overview by Platform

- 9.7.3.3. Colombian Application Development Software Market Overview by Deployment

- 9.7.3.4. Colombian Application Development Software Market Overview by Company Type

- 9.7.3.5. Colombian Application Development Software Market Overview by Industry Sector

- 9.7.4. CHILE

- 9.7.4.1. Chilean Application Development Software Market Overview by Application

- 9.7.4.2. Chilean Application Development Software Market Overview by Platform

- 9.7.4.3. Chilean Application Development Software Market Overview by Deployment

- 9.7.4.4. Chilean Application Development Software Market Overview by Company Type

- 9.7.4.5. Chilean Application Development Software Market Overview by Industry Sector

- 9.7.5. PERU

- 9.7.5.1. Peruvian Application Development Software Market Overview by Application

- 9.7.5.2. Peruvian Application Development Software Market Overview by Platform

- 9.7.5.3. Peruvian Application Development Software Market Overview by Deployment

- 9.7.5.4. Peruvian Application Development Software Market Overview by Company Type

- 9.7.5.5. Peruvian Application Development Software Market Overview by Industry Sector

- 9.7.6. REST OF SOUTH AMERICA

- 9.7.6.1. Rest of South America Application Development Software Market Overview by Application

- 9.7.6.2. Rest of South America Application Development Software Market Overview by Platform

- 9.7.6.3. Rest of South America Application Development Software Market Overview by Deployment

- 9.7.6.4. Rest of South America Application Development Software Market Overview by Company Type

- 9.7.6.5. Rest of South America Application Development Software Market Overview by Industry Sector

- 9.7.1. BRAZIL

10. MIDDLE EAST & AFRICA

- 10.1. Middle East & Africa Application Development Software Market Overview by Geographic Region

- 10.2. Middle East & Africa Application Development Software Market Overview by Application

- 10.3. Middle East & Africa Application Development Software Market Overview by Platform

- 10.4. Middle East & Africa Application Development Software Market Overview by Deployment

- 10.5. Middle East & Africa Application Development Software Market Overview by Company Type

- 10.6. Middle East & Africa Application Development Software Market Overview by Industry Sector

- 10.7. Country-wise Analysis of Middle East & Africa Application Development Software Market

- 10.7.1. THE UNITED ARAB EMIRATES

- 10.7.1.1. United Arab Emirates Application Development Software Market Overview by Application

- 10.7.1.2. United Arab Emirates Application Development Software Market Overview by Platform

- 10.7.1.3. United Arab Emirates Application Development Software Market Overview by Deployment

- 10.7.1.4. United Arab Emirates Application Development Software Market Overview by Company Type

- 10.7.1.5. United Arab Emirates Application Development Software Market Overview by Industry Sector

- 10.7.2. SOUTH AFRICA

- 10.7.2.1. South African Application Development Software Market Overview by Application

- 10.7.2.2. South African Application Development Software Market Overview by Platform

- 10.7.2.3. South African Application Development Software Market Overview by Deployment

- 10.7.2.4. South African Application Development Software Market Overview by Company Type

- 10.7.2.5. South African Application Development Software Market Overview by Industry Sector

- 10.7.3. EGYPT

- 10.7.3.1. Egyptian Application Development Software Market Overview by Application

- 10.7.3.2. Egyptian Application Development Software Market Overview by Platform

- 10.7.3.3. Egyptian Application Development Software Market Overview by Deployment

- 10.7.3.4. Egyptian Application Development Software Market Overview by Company Type

- 10.7.3.5. Egyptian Application Development Software Market Overview by Industry Sector

- 10.7.4. SAUDI ARABIA

- 10.7.4.1. Saudi Arabian Application Development Software Market Overview by Application

- 10.7.4.2. Saudi Arabian Application Development Software Market Overview by Platform

- 10.7.4.3. Saudi Arabian Application Development Software Market Overview by Deployment

- 10.7.4.4. Saudi Arabian Application Development Software Market Overview by Company Type

- 10.7.4.5. Saudi Arabian Application Development Software Market Overview by Industry Sector

- 10.7.5. MOROCCO

- 10.7.5.1. Moroccan Application Development Software Market Overview by Application

- 10.7.5.2. Moroccan Application Development Software Market Overview by Platform

- 10.7.5.3. Moroccan Application Development Software Market Overview by Deployment

- 10.7.5.4. Moroccan Application Development Software Market Overview by Company Type

- 10.7.5.5. Moroccan Application Development Software Market Overview by Industry Sector

- 10.7.6. KUWAIT

- 10.7.6.1. Kuwait Application Development Software Market Overview by Application

- 10.7.6.2. Kuwait Application Development Software Market Overview by Platform

- 10.7.6.3. Kuwait Application Development Software Market Overview by Deployment

- 10.7.6.4. Kuwait Application Development Software Market Overview by Company Type

- 10.7.6.5. Kuwait Application Development Software Market Overview by Industry Sector

- 10.7.7. QATAR

- 10.7.7.1. Qatar Application Development Software Market Overview by Application

- 10.7.7.2. Qatar Application Development Software Market Overview by Platform

- 10.7.7.3. Qatar Application Development Software Market Overview by Deployment

- 10.7.7.4. Qatar Application Development Software Market Overview by Company Type

- 10.7.7.5. Qatar Application Development Software Market Overview by Industry Sector

- 10.7.8. REST OF MIDDLE EAST & AFRICA

- 10.7.8.1. Rest of Middle East & Africa Application Development Software Market Overview by Application

- 10.7.8.2. Rest of Middle East & Africa Application Development Software Market Overview by Platform

- 10.7.8.3. Rest of Middle East & Africa Application Development Software Market Overview by Deployment

- 10.7.8.4. Rest of Middle East & Africa Application Development Software Market Overview by Company Type

- 10.7.8.5. Rest of Middle East & Africa Application Development Software Market Overview by Industry Sector

- 10.7.1. THE UNITED ARAB EMIRATES

PART C: GUIDE TO THE INDUSTRY

- 1. NORTH AMERICA

- 2. EUROPE

- 3. ASIA-PACIFIC

PART D: ANNEXURE

- 1. RESEARCH METHODOLOGY

- 2. FEEDBACK

Charts & Graphs

PART A: GLOBAL MARKET PERSPECTIVE

- Chart 1: Global Application Development Software Market (2024 & 2030) by Geographic Region

- Chart 2: Global Application Development Software Market (2024 & 2030) by Application

- Chart 3: Global Application Development Software Market (2024 & 2030) by Platform Type

- Chart 4: Global Application Development Software Market (2024 & 2030) by Deployment Type

- Chart 5: Global Application Development Software Market (2024 & 2030) by Company Type

- Chart 6: Global Application Development Software Market (2024 & 2030) by Industry Sector

- Chart 7: Global Application Development Software Market Share (2024) by Company

GLOBAL MARKET OVERVIEW

- Chart 8: Global Application Development Software Market Analysis (2021-2030) in US$ Million

- Chart 9: Global Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 10: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 11: Global Web & Cloud Application Development Software Market Analysis (2021-2030) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 12: Glance at 2021, 2024 and 2030 Global Web & Cloud Application Development Software Market Share (%) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 13: Global Mobile Application Development Software Market Analysis (2021-2030) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 14: Glance at 2021, 2024 and 2030 Global Mobile Application Development Software Market Share (%) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 15: Global Desktop Application Development Software Market Analysis (2021-2030) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 16: Glance at 2021, 2024 and 2030 Global Desktop Application Development Software Market Share (%) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 17: Global Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 18: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 19: Global Application Development Software Market Analysis (2021-2030) in Low-Code Development Segment by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 20: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Low-Code Development Segment by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 21: Global Application Development Software Market Analysis (2021-2030) in No-Code Development Segment by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 22: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in No-Code Development Segment by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 23: Global Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 24: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 25: Global Application Development Software Market Analysis (2021-2030) in Cloud Deployments by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 26: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Cloud Deployments by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 27: Global Application Development Software Market Analysis (2021-2030) in On-Premise Deployments by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 28: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in On-Premise Deployments by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 29: Global Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 30: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 31: Global Application Development Software Market Analysis (2021-2030) in Large Enterprises by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 32: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Large Enterprises by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 33: Global Application Development Software Market Analysis (2021-2030) in Small & Medium Enterprises by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 34: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Small & Medium Enterprises by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 35: Global Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 36: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

- Chart 37: Global Application Development Software Market Analysis (2021-2030) in BFSI Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 38: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in BFSI Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 39: Global Application Development Software Market Analysis (2021-2030) in IT & Communication Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 40: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in IT & Communication Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 41: Global Application Development Software Market Analysis (2021-2030) in Retail & Ecommerce Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 42: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Retail & Ecommerce Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 43: Global Application Development Software Market Analysis (2021-2030) in Manufacturing Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 44: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Manufacturing Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 45: Global Application Development Software Market Analysis (2021-2030) in Healthcare & Life Sciences Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 46: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Healthcare & Life Sciences Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 47: Global Application Development Software Market Analysis (2021-2030) in Energy & Utilities Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 48: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Energy & Utilities Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 49: Global Application Development Software Market Analysis (2021-2030) in Government Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 50: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Government Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 51: Global Application Development Software Market Analysis (2021-2030) in Transportation Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 52: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Transportation Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 53: Global Application Development Software Market Analysis (2021-2030) in Construction Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 54: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Construction Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 55: Global Application Development Software Market Analysis (2021-2030) in Tourism & Hospitality Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 56: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Tourism & Hospitality Sector by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

- Chart 57: Global Application Development Software Market Analysis (2021-2030) in Other Industry Sectors by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 58: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) in Other Industry Sectors by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

PART B: REGIONAL MARKET PERSPECTIVE

- Chart 59: Global Application Development Software Market Analysis (2021-2030) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa in US$ Million

- Chart 60: Glance at 2021, 2024 and 2030 Global Application Development Software Market Share (%) by Geographic Region - North America, Europe, Asia-Pacific, South America and Middle East & Africa

REGIONAL MARKET OVERVIEW

NORTH AMERICA

- Chart 61: North American Application Development Software Market Analysis (2021-2030) in US$ Million

- Chart 62: North American Application Development Software Market Analysis (2021-2030) by Geographic Region - United States, Canada and Mexico in US$ Million

- Chart 63: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Geographic Region - United States, Canada and Mexico

- Chart 64: North American Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 65: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 66: North American Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 67: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 68: North American Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 69: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 70: North American Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 71: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 72: North American Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 73: Glance at 2021, 2024 and 2030 North American Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

THE UNITED STATES

- Chart 74: United States Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 75: Glance at 2021, 2024 and 2030 United States Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 76: United States Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 77: Glance at 2021, 2024 and 2030 United States Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 78: United States Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 79: Glance at 2021, 2024 and 2030 United States Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 80: United States Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 81: Glance at 2021, 2024 and 2030 United States Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 82: United States Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 83: Glance at 2021, 2024 and 2030 United States Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

CANADA

- Chart 84: Canadian Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 85: Glance at 2021, 2024 and 2030 Canadian Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 86: Canadian Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 87: Glance at 2021, 2024 and 2030 Canadian Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 88: Canadian Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 89: Glance at 2021, 2024 and 2030 Canadian Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 90: Canadian Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 91: Glance at 2021, 2024 and 2030 Canadian Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 92: Canadian Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 93: Glance at 2021, 2024 and 2030 Canadian Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

MEXICO

- Chart 94: Mexican Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 95: Glance at 2021, 2024 and 2030 Mexican Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 96: Mexican Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 97: Glance at 2021, 2024 and 2030 Mexican Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 98: Mexican Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 99: Glance at 2021, 2024 and 2030 Mexican Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 100: Mexican Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 101: Glance at 2021, 2024 and 2030 Mexican Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 102: Mexican Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 103: Glance at 2021, 2024 and 2030 Mexican Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

EUROPE

- Chart 104: European Application Development Software Market Analysis (2021-2030) in US$ Million

- Chart 105: European Application Development Software Market Analysis (2021-2030) by Geographic Region - Germany, United Kingdom, France, Italy, Netherlands, Spain, Russia, Switzerland and Rest of Europe in US$ Million

- Chart 106: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Geographic Region - Germany, United Kingdom, France, Italy, Netherlands, Spain, Russia, Switzerland and Rest of Europe

- Chart 107: European Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 108: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 109: European Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 110: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 111: European Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 112: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 113: European Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 114: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 115: European Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 116: Glance at 2021, 2024 and 2030 European Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

GERMANY

- Chart 117: German Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 118: Glance at 2021, 2024 and 2030 German Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 119: German Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 120: Glance at 2021, 2024 and 2030 German Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 121: German Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 122: Glance at 2021, 2024 and 2030 German Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 123: German Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 124: Glance at 2021, 2024 and 2030 German Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 125: German Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 126: Glance at 2021, 2024 and 2030 German Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

THE UNITED KINGDOM

- Chart 127: United Kingdom Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 128: Glance at 2021, 2024 and 2030 United Kingdom Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 129: United Kingdom Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 130: Glance at 2021, 2024 and 2030 United Kingdom Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 131: United Kingdom Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 132: Glance at 2021, 2024 and 2030 United Kingdom Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 133: United Kingdom Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 134: Glance at 2021, 2024 and 2030 United Kingdom Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 135: United Kingdom Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 136: Glance at 2021, 2024 and 2030 United Kingdom Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

FRANCE

- Chart 137: French Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 138: Glance at 2021, 2024 and 2030 French Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 139: French Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 140: Glance at 2021, 2024 and 2030 French Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 141: French Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 142: Glance at 2021, 2024 and 2030 French Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 143: French Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 144: Glance at 2021, 2024 and 2030 French Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 145: French Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 146: Glance at 2021, 2024 and 2030 French Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

ITALY

- Chart 147: Italian Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 148: Glance at 2021, 2024 and 2030 Italian Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 149: Italian Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 150: Glance at 2021, 2024 and 2030 Italian Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 151: Italian Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 152: Glance at 2021, 2024 and 2030 Italian Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 153: Italian Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 154: Glance at 2021, 2024 and 2030 Italian Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 155: Italian Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 156: Glance at 2021, 2024 and 2030 Italian Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

THE NETHERLANDS

- Chart 157: Dutch Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 158: Glance at 2021, 2024 and 2030 Dutch Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 159: Dutch Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 160: Glance at 2021, 2024 and 2030 Dutch Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 161: Dutch Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 162: Glance at 2021, 2024 and 2030 Dutch Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 163: Dutch Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 164: Glance at 2021, 2024 and 2030 Dutch Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 165: Dutch Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 166: Glance at 2021, 2024 and 2030 Dutch Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

SPAIN

- Chart 167: Spanish Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 168: Glance at 2021, 2024 and 2030 Spanish Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 169: Spanish Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 170: Glance at 2021, 2024 and 2030 Spanish Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 171: Spanish Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 172: Glance at 2021, 2024 and 2030 Spanish Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 173: Spanish Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 174: Glance at 2021, 2024 and 2030 Spanish Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 175: Spanish Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 176: Glance at 2021, 2024 and 2030 Spanish Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

RUSSIA

- Chart 177: Russian Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 178: Glance at 2021, 2024 and 2030 Russian Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 179: Russian Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 180: Glance at 2021, 2024 and 2030 Russian Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 181: Russian Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 182: Glance at 2021, 2024 and 2030 Russian Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 183: Russian Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 184: Glance at 2021, 2024 and 2030 Russian Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 185: Russian Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 186: Glance at 2021, 2024 and 2030 Russian Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

SWITZERLAND

- Chart 187: Swiss Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 188: Glance at 2021, 2024 and 2030 Swiss Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 189: Swiss Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million

- Chart 190: Glance at 2021, 2024 and 2030 Swiss Application Development Software Market Share (%) by Platform - Low-Code Development and No-Code Development

- Chart 191: Swiss Application Development Software Market Analysis (2021-2030) by Deployment - Cloud and On-Premise in US$ Million

- Chart 192: Glance at 2021, 2024 and 2030 Swiss Application Development Software Market Share (%) by Deployment - Cloud and On-Premise

- Chart 193: Swiss Application Development Software Market Analysis (2021-2030) by Company Type - Large and Small & Medium in US$ Million

- Chart 194: Glance at 2021, 2024 and 2030 Swiss Application Development Software Market Share (%) by Company Type - Large and Small & Medium

- Chart 195: Swiss Application Development Software Market Analysis (2021-2030) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others in US$ Million

- Chart 196: Glance at 2021, 2024 and 2030 Swiss Application Development Software Market Share (%) by Industry Sector - BFSI, IT & Communication, Retail & Ecommerce, Manufacturing, Healthcare & Life Sciences, Energy & Utilities, Government, Transportation, Construction, Tourism & Hospitality and Others

REST OF EUROPE

- Chart 197: Rest of Europe Application Development Software Market Analysis (2021-2030) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development in US$ Million

- Chart 198: Glance at 2021, 2024 and 2030 Rest of Europe Application Development Software Market Share (%) by Application - Web & Cloud Application Development, Mobile Application Development and Desktop Application Development

- Chart 199: Rest of Europe Application Development Software Market Analysis (2021-2030) by Platform - Low-Code Development and No-Code Development in US$ Million