PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1796194

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1796194

Enterprise Imaging IT Market by Function (VNA, PACS, Universal Viewer, Analytics), Modality (X-ray, MRI, CT, PET, SPECT, Mammo), Application (Diagnosis, Therapeutic, Theranostic), Therapy (Onco, Cardio, Neuro), End User, Region - Global Forecast to 2030

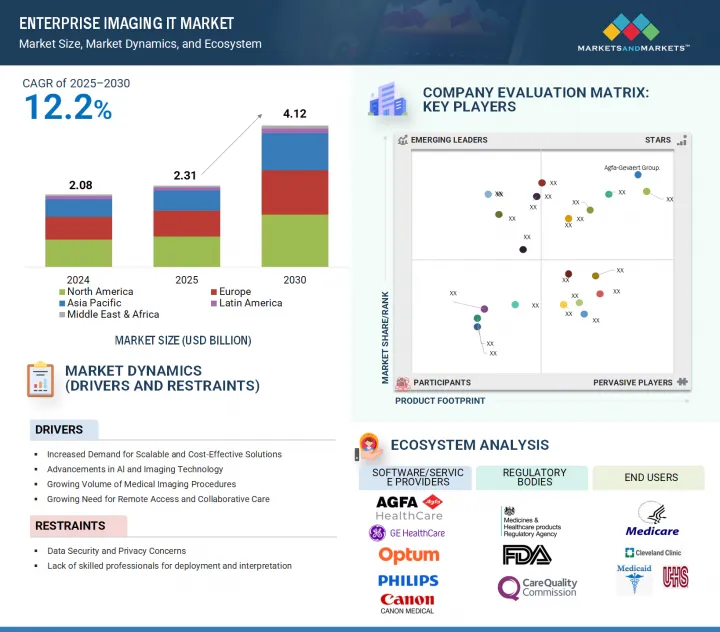

The global enterprise imaging IT market is projected to reach USD 4.12 billion by 2030 from USD 2.31 billion in 2025, at a CAGR of 12.2% during the forecast period. Demand is propelled by the shift from capital-heavy license models to cloud native SaaS deployments, which lower upfront costs and accelerate upgrades.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Function, Modality, Application, Offering, Deployment Mode, Therapeutic Area, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

The emergence of blockchain-backed image provenance platforms is enhancing data integrity and auditability across multi-vendor ecosystems. Growing medical tourism networks are driving the need for standardized, cross-border image exchange hubs, while the proliferation of point-of-care ultrasound and wearable imaging devices is expanding enterprise workflows to include real-time, bedside acquisitions.

"The diagnostics segment is the fastest-growing segment in the enterprise imaging IT market within the forecast period."

Based on applications, the enterprise imaging IT market has been divided into diagnostics, therapeutics, and clinical research. The diagnostics segment accounts for the largest share of the enterprise imaging IT market. This segment's large share and high growth can be attributed to the nationwide rollout of lung cancer screening programs, which has surged low-dose CT volumes and driven enterprise archive demand. The integration of AI-driven triage engines that automatically flag critical findings such as intracranial hemorrhages or pulmonary emboli has also pushed providers to upgrade diagnostic platforms. Additionally, the rise of quantitative radiomics and texture analysis workflows for oncology and neurology imaging is creating demand for solutions that can store, process, and mine high-dimensional feature sets at scale.

"The cardiology segment is estimated to hold the largest share of the enterprise imaging IT market in 2024, by therapeutic area."

Based on therapeutic area, the enterprise imaging IT market is segmented into neurology, cardiology, oncology, orthopedics, and other therapeutic areas. The cardiology segment held the largest share in 2024 due to the surge in CT-derived fractional flow reserve (FFR CT) workflows, which require seamless integration of computational models and high-fidelity CT archives. The rapid expansion of hybrid cath lab/OR suites is driving the demand for enterprise viewers that can overlay 3D vessel reconstructions in real time during transcatheter valve and structural interventions. New CPT codes for AI-quantified ejection fraction and chamber volumetrics are also incentivizing hospitals to deploy platforms with built-in cardiac analytics. Additionally, the proliferation of wearable ECG and implantable device data streams is pushing cardiology departments to adopt enterprise solutions that fuse multi source signals with imaging studies for comprehensive cardiac risk stratification.

"The Asia Pacific region is expected to register the highest growth rate in the enterprise imaging IT market during the forecast period."

The global enterprise imaging IT market is segmented into five major regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, Asia Pacific is expected to register the highest growth for enterprise imaging IT in the forecast period. Factors such as India's National Digital Health Mission integrating imaging data into its Health Locker for unified patient records, the rise of medical tourism hubs in Malaysia and Thailand demanding seamless cross border image exchange, public-private partnerships deploying mobile CT and MRI units in rural China, and the explosive uptake of low cost, AI powered handheld ultrasound devices in South Korea and India are all fueling Asia Pacific's rapid enterprise imaging IT adoption.

The breakdown of primary participants is as mentioned below:

- By Company Type: Tier 1 (41%), Tier 2 (31%), and Tier 3 (28%)

- By Designation: C-level Executives (44%), Directors (31%), and Others (25%)

- By Region: North America (45%), Europe (28%), Asia Pacific (20%), Latin America (4%), and the Middle East & Africa (3%)

Key Players

The prominent players in this market are Agfa-Gevaert Group (Belgium), FUJIFILM Corporation (Japan), Merative (US), Pro Medicus, Ltd. (Australia), Optum, Inc. (US), GE HealthCare (US), Intelerad (Canada), Sectra AB (Sweden), CANON MEDICAL SYSTEMS CORPORATION (Japan), Hyland Software, Inc. (US), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), INFINITT Healthcare Co., Ltd. (South Korea), Novarad (US), Mach7 Technologies (US), Hermes Medical Solutions (Sweden), Konica Minolta, Inc. (Japan), BridgeHead Software Ltd. (England), Sclmage, Inc. (US), VISUS Health IT GmbH (Germany), Dicom Systems, Inc. (US), PostDICOM (Netherlands), Qaelum (Belgium), AdvaHealth Solutions (Singapore), PaxeraHealth (US), and Rad AI (US). Players adopted organic and inorganic growth strategies such as solution launches, enhancements, and upgrades; collaborations; partnerships; acquisitions; agreements; and expansions to increase their offerings, cater to customers' unmet needs, increase their profitability, and expand their presence in the global market.

Research Coverage

- The report studies the enterprise imaging IT market based on function, modality, application, offering, deployment mode, therapeutic area, end user, and region.

- The report analyzes factors (such as drivers, restraints, opportunities, and challenges) affecting the market growth.

- The report evaluates the opportunities and challenges in the market for stakeholders and provides details of the competitive landscape for market leaders.

- The report studies micromarkets with respect to their growth trends, prospects, and contributions to the total enterprise imaging IT market.

- The report forecasts the revenue of market segments with respect to five major regions.

Reasons to Buy the Report

The report can help established firms, as well as new entrants/smaller firms, gauge the pulse of the market, which, in turn, would help them garner a greater share. Firms purchasing the report could use one or a combination of the five strategies mentioned below.

This report provides insights into the following pointers:

- Analysis of key drivers, restraints, opportunities, and challenges influencing the growth of the enterprise imaging IT market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and product launches in the enterprise imaging IT market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of enterprise imaging IT solutions across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the enterprise imaging IT market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the enterprise imaging IT market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary sources

- 2.1.1 SECONDARY DATA

- 2.2 RESEARCH APPROACH

- 2.3 MARKET SIZE ESTIMATION

- 2.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.5.1 MARKET SIZING ASSUMPTIONS

- 2.5.2 OVERALL STUDY ASSUMPTIONS

- 2.6 RISK ASSESSMENT

- 2.7 RESEARCH LIMITATIONS

- 2.7.1 METHODOLOGY-RELATED LIMITATIONS

- 2.7.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ENTERPRISE IMAGING IT MARKET OVERVIEW

- 4.2 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION & REGION

- 4.3 ENTERPRISE IMAGING IT MARKET: GEOGRAPHIC SNAPSHOT

- 4.4 ENTERPRISE IMAGING IT MARKET: DEVELOPED VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increased demand for scalable and cost-effective solutions

- 5.2.1.2 Advancements in AI and imaging technologies

- 5.2.1.3 Growing volume of medical imaging procedures

- 5.2.1.4 Growing need for remote access and collaborative care

- 5.2.1.5 Government initiatives and favorable policies

- 5.2.2 RESTRAINTS

- 5.2.2.1 Data security and privacy concerns

- 5.2.2.2 Lack of skilled professionals for deployment and interpretation

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion into emerging markets

- 5.2.3.2 Multi modality and advanced visualization

- 5.2.3.3 Partnerships with AI and analytics providers

- 5.2.3.4 Value-based care and population health management

- 5.2.3.5 Cloud native and edge computing innovations

- 5.2.4 CHALLENGES

- 5.2.4.1 Interoperability with legacy and vendor-specific systems

- 5.2.4.2 High upfront integration and deployment costs

- 5.2.4.3 Workflow disruption and user adoption

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 INDUSTRY TRENDS

- 5.4.1 AI-ENABLED DIAGNOSTICS AND PREDICTIVE ANALYTICS

- 5.4.2 UNIFIED IMAGING DATA INTEGRATION AND COLLABORATIVE DIAGNOSTICS

- 5.4.3 CLOUD-BASED IMAGING IT PLATFORMS AND DIGITAL TRANSFORMATION

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Imaging analytics platforms

- 5.7.1.2 Artificial intelligence and machine learning

- 5.7.1.3 Multi modality fusion & co registration engines

- 5.7.1.4 Zero footprint viewers

- 5.7.1.5 Mobile enterprise imaging and workflow bots

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Radiology information systems (RIS)

- 5.7.2.2 Electronic health record (EHR/EMR) integration

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Cloud computing & storage

- 5.7.3.2 Blockchain & distributed ledger technology

- 5.7.1 KEY TECHNOLOGIES

- 5.8 REGULATORY ANALYSIS

- 5.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, & OTHER ORGANIZATIONS

- 5.8.2 REGULATORY LANDSCAPE

- 5.8.2.1 North America

- 5.8.2.2 Europe

- 5.8.2.3 Asia Pacific

- 5.8.2.4 Latin America

- 5.8.2.5 Middle East & Africa

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY FUNCTION (2024)

- 5.9.2 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY REGION (2024)

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 BARGAINING POWER OF SUPPLIERS

- 5.10.2 BARGAINING POWER OF BUYERS

- 5.10.3 THREAT OF SUBSTITUTES

- 5.10.4 THREAT OF NEW ENTRANTS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 PATENT ANALYSIS

- 5.11.1 PATENT PUBLICATION TRENDS FOR ENTERPRISE IMAGING IT MARKET

- 5.11.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 5.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 END-USER ANALYSIS

- 5.13.1 UNMET NEEDS

- 5.13.2 END-USER EXPECTATIONS

- 5.14 KEY CONFERENCES & EVENTS, 2025-2026

- 5.15 CASE STUDY ANALYSIS

- 5.16 INVESTMENT & FUNDING SCENARIO

- 5.17 BUSINESS MODEL ANALYSIS

- 5.18 IMPACT OF GENERATIVE AI ON ENTERPRISE IMAGING IT MARKET

- 5.18.1 TOP USE CASES & MARKET POTENTIAL

- 5.18.1.1 Key use cases

- 5.18.2 CASE STUDIES OF AI/GENERATIVE AI IMPLEMENTATION

- 5.18.2.1 Case Study 1: Enabling interoperability and scalability across enterprise imaging networks with Dicom Systems' Unifier Platform

- 5.18.2.2 Case Study 2: More images, more insight, more collaboration - San Gerardo Hospital transforms radiology with Agfa HealthCare's Enterprise Imaging

- 5.18.3 INTERCONNECTED & ADJACENT MARKETS

- 5.18.3.1 Vendor Neutral Archive (VNA) & PACS Market

- 5.18.3.2 Medical Image Analysis Software Market

- 5.18.3.3 Healthcare IT Market

- 5.18.4 USER READINESS & IMPACT ASSESSMENT

- 5.18.4.1 User readiness

- 5.18.4.1.1 User A: Hospitals

- 5.18.4.1.2 User B: Diagnostic centers

- 5.18.4.2 Impact assessment

- 5.18.4.2.1 User A: Hospitals

- 5.18.4.2.1.1 Implementation

- 5.18.4.2.1.2 Impact

- 5.18.4.2.2 User B: Diagnostic centers

- 5.18.4.2.2.1 Implementation

- 5.18.4.2.2.2 Impact

- 5.18.4.2.1 User A: Hospitals

- 5.18.4.1 User readiness

- 5.18.1 TOP USE CASES & MARKET POTENTIAL

- 5.19 IMPACT OF 2025 US TARIFFS ON ENTERPRISE IMAGING IT MARKET

- 5.19.1 INTRODUCTION

- 5.19.2 KEY TARIFF RATES

- 5.19.3 PRICE IMPACT ANALYSIS

- 5.19.3.1 Increased costs of hardware components

- 5.19.3.2 Software & licensing inflation

- 5.19.3.3 Supply chain disruption

- 5.19.4 IMPACT ON COUNTRY/REGION

- 5.19.4.1 US

- 5.19.4.2 Europe

- 5.19.4.3 Asia Pacific

- 5.19.5 IMPACT ON END USERS

- 5.19.5.1 Hospitals (large, mid-sized, and academic medical centers)

- 5.19.5.2 Diagnostic centers (independent and chain-based)

- 5.19.5.3 Teleradiology providers

6 ENTERPRISE IMAGING IT MARKET, BY FUNCTION

- 6.1 INTRODUCTION

- 6.2 VENDOR NEUTRAL ARCHIVES (VNA)

- 6.2.1 ADVANCING SEAMLESS INFORMATION EXCHANGE THROUGH VNA SOLUTIONS TO BOOST MARKET GROWTH

- 6.3 PICTURE ARCHIVING AND COMMUNICATION SYSTEMS (PACS)

- 6.3.1 GROWING INTEGRATION OF AI WITHIN PACS FOR OPTIMIZED RADOIOLOGY WORKFLOWS TO SUPPORT MARKET GROWTH

- 6.4 IMAGE EXCHANGE

- 6.4.1 GROWING POPULARITY OF INTEROPERABLE IMAGING NETWORKS FOR PATIENT-CENTERED DATA SHARING TO DRIVE GROWTH

- 6.5 UNIVERSAL VIEWERS

- 6.5.1 GROWING UNIVERSAL VIEWER DEPLOYMENT FOR MULTI-DISCIPLINARY IMAGING TO FUEL MARKET

- 6.6 WORKFLOW ORCHESTRATION

- 6.6.1 AI-POWERED IMAGING WORKFLOW AUTOMATION AND CROSS-MODALITY COORDINATION TO PROPEL MARKET

- 6.7 ANALYTICS

- 6.7.1 GROWING NEED FOR ANALYTICS PLATFORMS FOR VALUE-BASED IMAGING AND OPERATIONAL OPTIMIZATION TO DRIVE MARKET

- 6.8 OTHER FUNCTIONS

7 ENTERPRISE IMAGING IT MARKET, BY APPLICATION

- 7.1 INTRODUCTION

- 7.2 DIAGNOSTICS

- 7.2.1 AI-ENABLED QUANTIFICATION AND INTEGRATED THERANOSTIC WORKFLOWS TO DRIVE DIAGNOSTIC IMAGING TRANSFORMATION

- 7.3 THERAPEUTICS

- 7.3.1 ADVANTAGES SUCH AS MULTIMODAL TREATMENT INTEGRATION TO OPTIMIZE ENTERPRISE IMAGING FOR THERAPEUTIC WORKFLOWS

- 7.4 CLINICAL RESEARCH

- 7.4.1 AI-ENABLED QUANTIFICATION AND RAPID-RESPONSE IMAGING WORKFLOWS TO ACCELERATE CLINICAL RESEARCH

8 ENTERPRISE IMAGING IT MARKET, BY MODALITY

- 8.1 INTRODUCTION

- 8.2 X-RAY

- 8.2.1 GROWTH IN ENTERPRISE IMAGING THROUGH AI-ENABLED X-RAY SOLUTIONS TO BOOST MARKET

- 8.3 MAGNETIC RESONANCE IMAGING (MRI)

- 8.3.1 EXPANDING MRI ENTERPRISE IT TO MEET RISING NEUROLOGICAL IMAGING DEMANDS TO SUPPORT MARKET GROWTH

- 8.4 COMPUTED TOMOGRAPHY (CT)

- 8.4.1 REGULATORY AND VALUE-BASED INCENTIVES TO FUEL CT IMAGING IT ADOPTION

- 8.5 ULTRASOUND

- 8.5.1 AI-POWERED ULTRASOUND AND POCUS TO ACCELERATE ENTERPRISE IMAGING TRANSFORMATION

- 8.6 NUCLEAR IMAGING

- 8.6.1 POSITRON EMISSION TOMOGRAPHY (PET)

- 8.6.1.1 Rising PET scan volumes to drive demand for scalable, intelligent Imaging IT

- 8.6.2 SINGLE-PHOTON EMISSION COMPUTED TOMOGRAPHY (SPECT)

- 8.6.2.1 Driving diagnostic accuracy with automated SPECT workflows to contribute to growth

- 8.6.1 POSITRON EMISSION TOMOGRAPHY (PET)

- 8.7 ENDOSCOPY

- 8.7.1 ENABLING REAL-TIME ENDOSCOPIC INSIGHTS THROUGH CLOUD-NATIVE VIDEO ORCHESTRATION TO DRIVE MARKET

- 8.8 MAMMOGRAPHY

- 8.8.1 NEED FOR ENTERPRISE IMAGING SOLUTIONS FOR HIGH-VOLUME, HIGH-RESOLUTION MAMMOGRAPHY WORKFLOWS TO FUEL GROWTH

- 8.9 FLUOROSCOPY

- 8.9.1 STRATEGIC CLOUD-NATIVE IMAGING FOR ADVANCED FLUOROSCOPY USE CASES TO AID WITH GROWTH

- 8.10 ECHOCARDIOGRAPHY

- 8.10.1 ABILITY TO ENHANCE FLUOROSCOPY IMAGING EFFICIENCY WITH AI-INTEGRATED ENTERPRISE IT SOLUTIONS TO BOOST MARKET

- 8.11 OTHER MODALITIES

9 ENTERPRISE IMAGING IT MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 SOFTWARE

- 9.2.1 ADVANCING UNIFIED IMAGING ECOSYSTEMS THROUGH CLOUD-NATIVE SOFTWARE TO BOOST MARKET GROWTH

- 9.3 SERVICES

- 9.3.1 ADVANTAGES SUCH AS EXPERT SERVICES, CLOUD MIGRATION, AND WORKFLOW OPTIMIZATION TO SUPPORT MARKET GROWTH

10 ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE

- 10.1 INTRODUCTION

- 10.2 ON-PREMISE SOLUTIONS

- 10.2.1 GROWING NEED FOR IMAGING PERFORMANCE AND DATA CONTROL THROUGH ON-PREMISE DEPLOYMENT TO SUPPORT MARKET GROWTH

- 10.3 CLOUD-BASED SOLUTIONS

- 10.3.1 RISING NEED FOR COST-EFFICIENT, SCALABLE INFRASTRUCTURE TO DRIVE DEMAND FOR CLOUD-BASED DEPLOYMENT

- 10.4 HYBRID SOLUTIONS

- 10.4.1 ABILITY TO BRIDGE DATA CONTROL AND CLOUD INNOVATION THROUGH HYBRID DEPLOYMENT TO BOOST GROWTH

11 ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA

- 11.1 INTRODUCTION

- 11.2 NEUROLOGY

- 11.2.1 INTEGRATION OF AI-DRIVEN MULTIMODAL NEUROIMAGING FOR PERSONALIZED NEUROLOGICAL CARE TO BOOST MARKET

- 11.3 CARDIOLOGY

- 11.3.1 CLOUD-ENABLED, AI-DRIVEN ENTERPRISE IMAGING PLATFORMS TO ACCELERATE ADVANCED CARDIAC DIAGNOSTICS

- 11.4 ONCOLOGY

- 11.4.1 AI-DRIVEN, MULTIMODAL ENTERPRISE IMAGING PLATFORMS TO ADVANCE PRECISION ONCOLOGY

- 11.5 ORTHOPEDICS

- 11.5.1 ABILITY OF AI-ENABLED ENTERPRISE IMAGING PLATFORMS TO TRANSFORM ORTHOPEDIC CARE TO DRIVE DEMAND

- 11.6 OTHER THERAPEUTIC AREAS

12 ENTERPRISE IMAGING IT MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 HOSPITALS

- 12.2.1 HOSPITALS TO DRIVE DEMAND FOR UNIFIED IMAGING INFRASTRUCTURE TO SUPPORT INTEGRATED CARE DELIVERY

- 12.3 DIAGNOSTIC CENTERS

- 12.3.1 GROWING ADOPTION OF ENTERPRISE IMAGING IT TO ENHANCE WORKFLOW EFFICIENCY IN DIAGNOSTIC CENTERS TO BOOST MARKET

- 12.4 CLINICS & OUTPATIENT SETTINGS

- 12.4.1 GROWING POPULARITY OF LIGHTWEIGHT ENTERPRISE IMAGING IT TO BOOST EFFICIENCY AND PATIENT THROUGHPUT TO FUEL GROWTH

- 12.5 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 12.5.1 GROWING USE OF ENTERPRISE IMAGING IT FOR TRANSLATIONAL RESEARCH AND DRUG DEVELOPMENT TO DRIVE MARKET

- 12.6 MEDTECH COMPANIES

- 12.6.1 ABILITY OF ENTERPRISE IMAGING IT TO ACCELERATE DEVICE INNOVATION AND CLINICAL INTEGRATION TO FUEL ADOPTION

- 12.7 RESEARCH & ACADEMIC INSTITUTES

- 12.7.1 GROWING NEED TO POWER DATA-DRIVEN DISCOVERY AND COLLABORATION TO SUPPORT MARKET GROWTH

- 12.8 OTHER END USERS

13 ENTERPRISE IMAGING IT MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 AI integration, cloud adoption, and regulatory push to accelerate enterprise imaging IT transformation in US

- 13.2.3 CANADA

- 13.2.3.1 Provincial interoperability mandates and cloud-enabled AI to drive growth in Canada's imaging IT market

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Hospital modernization and ePA adoption to propel Germany's enterprise imaging IT growth

- 13.3.3 UK

- 13.3.3.1 NHS push for AI-driven imaging and cloud integration to fuel market growth

- 13.3.4 FRANCE

- 13.3.4.1 France to accelerate cloud-native, interoperable imaging platforms with focus on data sovereignty

- 13.3.5 ITALY

- 13.3.5.1 Growing VNA and teleradiology adoption in Italy to modernize imaging infrastructure

- 13.3.6 SPAIN

- 13.3.6.1 Spain to scale cloud imaging and VNA for regional collaboration

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 CHINA

- 13.4.2.1 AI diagnostic approvals to accelerate market growth

- 13.4.3 JAPAN

- 13.4.3.1 Aging demographics to drive demand for scalable imaging solutions

- 13.4.4 INDIA

- 13.4.4.1 Government-led digitization to fuel imaging infrastructure expansion

- 13.4.5 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Government investments to accelerate public health digitization drives

- 13.5.3 MEXICO

- 13.5.3.1 Accelerating imaging modernization through nationwide digital integration in Mexico to boost market

- 13.5.4 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Enterprise imaging adoption accelerates across GCC amid workforce gaps and digital health push to support growth

- 13.6.3 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ENTERPRISE IMAGING IT MARKET

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2024

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 14.5.5.1 Company footprint

- 14.5.5.2 Region footprint

- 14.5.5.3 Function footprint

- 14.5.5.4 Application footprint

- 14.5.5.5 Therapeutic area footprint

- 14.5.5.6 Deployment mode footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of startups/SMEs

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/SOFTWARE COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 SOLUTION LAUNCHES, APPROVALS, AND ENHANCEMENTS

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AGFA-GEVAERT GROUP

- 15.1.1.1 Business overview

- 15.1.1.2 Solutions offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 FUJIFILM HOLDINGS CORPORATION

- 15.1.2.1 Business overview

- 15.1.2.2 Solutions offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 GE HEALTHCARE

- 15.1.3.1 Business overview

- 15.1.3.2 Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Solution launches & approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 KONINKLIJKE PHILIPS N.V.

- 15.1.4.1 Business overview

- 15.1.4.2 Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Solution launches & approvals

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 SIEMENS HEALTHINEERS AG

- 15.1.5.1 Business overview

- 15.1.5.2 Solutions offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Solution launches

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 OPTUM, INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Solutions offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.6.4 MnM view

- 15.1.6.4.1 Key strengths

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses & competitive threats

- 15.1.7 SECTRA AB

- 15.1.7.1 Business overview

- 15.1.7.2 Solutions offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Solution launches & approvals

- 15.1.7.3.2 Deals

- 15.1.8 CANON MEDICAL SYSTEMS CORPORATION

- 15.1.8.1 Business overview

- 15.1.8.2 Solutions offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Expansions

- 15.1.9 MERATIVE

- 15.1.9.1 Business overview

- 15.1.9.2 Solutions offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.10 PRO MEDICUS, LTD.

- 15.1.10.1 Business overview

- 15.1.10.2 Solutions offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Solution launches

- 15.1.10.3.2 Deals

- 15.1.11 INTELERAD MEDICAL SYSTEMS INCORPORATED

- 15.1.11.1 Business overview

- 15.1.11.2 Solutions offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Solution launches

- 15.1.11.3.2 Deals

- 15.1.12 HYLAND SOFTWARE, INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Solutions offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Solution launches

- 15.1.12.3.2 Deals

- 15.1.13 INFINITT HEALTHCARE CO., LTD.

- 15.1.13.1 Business overview

- 15.1.13.2 Solutions offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Solution launches & approvals

- 15.1.13.3.2 Deals

- 15.1.14 NOVARAD

- 15.1.14.1 Business overview

- 15.1.14.2 Solutions offered

- 15.1.15 MACH7 TECHNOLOGIES

- 15.1.15.1 Business overview

- 15.1.15.2 Solutions offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Solution launches

- 15.1.15.3.2 Deals

- 15.1.16 HERMES MEDICAL SOLUTIONS

- 15.1.16.1 Business overview

- 15.1.16.2 Solutions offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Solution launches, approvals, and enhancements

- 15.1.16.3.2 Deals

- 15.1.17 KONICA MINOLTA, INC.

- 15.1.17.1 Business overview

- 15.1.17.2 Solutions offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Solution launches & enhancements

- 15.1.17.3.2 Deals

- 15.1.18 BRIDGEHEAD SOFTWARE LTD.

- 15.1.18.1 Business overview

- 15.1.18.2 Solutions offered

- 15.1.18.3 Recent developments

- 15.1.18.3.1 Deals

- 15.1.19 SCIMAGE, INC.

- 15.1.19.1 Business overview

- 15.1.19.2 Solutions offered

- 15.1.19.3 Recent developments

- 15.1.19.3.1 Solution launches

- 15.1.19.3.2 Deals

- 15.1.20 VISUS HEALTH IT GMBH

- 15.1.20.1 Business overview

- 15.1.20.2 Solutions offered

- 15.1.20.3 Recent developments

- 15.1.20.3.1 Solution enhancements

- 15.1.1 AGFA-GEVAERT GROUP

- 15.2 OTHER PLAYERS

- 15.2.1 DICOM SYSTEMS, INC.

- 15.2.2 POSTDICOM

- 15.2.3 QAELUM

- 15.2.4 ADVAHEALTH SOLUTIONS

- 15.2.5 PAXERAHEALTH

- 15.2.6 RAD AI

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS

List of Tables

- TABLE 1 EXCHANGE RATES UTILIZED FOR CONVERSION TO USD

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 RISK ASSESSMENT: ENTERPRISE IMAGING IT MARKET

- TABLE 4 ENTERPRISE IMAGING IT MARKET: IMPACT ANALYSIS

- TABLE 5 TOP 30 HEALTHCARE DATA BREACHES IN US, 2011-2024

- TABLE 6 ENTERPRISE IMAGING IT MARKET: ROLE IN ECOSYSTEM

- TABLE 7 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 REGULATORY SCENARIO OF NORTH AMERICA

- TABLE 13 REGULATORY SCENARIO OF EUROPE

- TABLE 14 REGULATORY SCENARIO OF ASIA PACIFIC

- TABLE 15 REGULATORY SCENARIO OF LATIN AMERICA

- TABLE 16 REGULATORY SCENARIO OF MIDDLE EAST & AFRICA

- TABLE 17 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY FUNCTION (2024)

- TABLE 18 INDICATIVE PRICING FOR ENTERPRISE IT IMAGING SOLUTIONS, BY REGION (2024)

- TABLE 19 ENTERPRISE IMAGING IT MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 20 JURISDICTION ANALYSIS OF TOP APPLICANT COUNTRIES FOR ENTERPRISE IMAGING IT MARKET

- TABLE 21 ENTERPRISE IMAGING IT MARKET: LIST OF PATENTS/PATENT APPLICATIONS

- TABLE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TOP THREE END USERS (%)

- TABLE 23 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 24 UNMET NEEDS IN ENTERPRISE IMAGING IT MARKET

- TABLE 25 END-USER EXPECTATIONS IN ENTERPRISE IMAGING IT MARKET

- TABLE 26 ENTERPRISE IMAGING IT MARKET: KEY CONFERENCES & EVENTS, 2025-2026

- TABLE 27 CASE STUDY 1: ENHANCING IMAGING EFFICIENCY & SECURITY WITH SECTRA'S AUTOMATED MULTIMEDIA WORKFLOW

- TABLE 28 CASE STUDY 2: ENTERPRISE IMAGING CONSOLIDATION AT PIEDMONT HEALTHCARE WITH HYLAND VNA

- TABLE 29 CASE STUDY 3: ENTERPRISE-WIDE IMAGING UNIFICATION WITH GE'S EDISON DATALOGUE AT A LEADING MEDICAL CENTER

- TABLE 30 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 31 ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 32 VENDOR NEUTRAL ARCHIVES (VNA) OFFERED BY KEY MARKET PLAYERS

- TABLE 33 ENTERPRISE IMAGING IT MARKET FOR VENDOR NEUTRAL ARCHIVES (VNA), BY REGION, 2023-2030 (USD MILLION)

- TABLE 34 PICTURE ARCHIVING AND COMMUNICATION SYSTEMS (PACS) OFFERED BY KEY MARKET PLAYERS

- TABLE 35 ENTERPRISE IMAGING IT MARKET FOR PICTURE ARCHIVING AND COMMUNICATION SYSTEMS (PACS), BY REGION, 2023-2030 (USD MILLION)

- TABLE 36 IMAGE EXCHANGE SOLUTIONS OFFERED BY KEY MARKET PLAYERS

- TABLE 37 ENTERPRISE IMAGING IT MARKET FOR IMAGE EXCHANGE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 UNIVERSAL VIEWERS OFFERED BY KEY MARKET PLAYERS

- TABLE 39 ENTERPRISE IMAGING IT MARKET FOR UNIVERSAL VIEWERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 40 WORKFLOW ORCHESTRATION SOLUTIONS OFFERED BY KEY MARKET PLAYERS

- TABLE 41 ENTERPRISE IMAGING IT MARKET FOR WORKFLOW ORCHESTRATION, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 ANALYTICS SOLUTIONS OFFERED BY KEY MARKET PLAYERS

- TABLE 43 ENTERPRISE IMAGING IT MARKET FOR ANALYTICS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 44 ENTERPRISE IMAGING IT MARKET FOR OTHER FUNCTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 45 ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 46 ENTERPRISE IMAGING IT MARKET FOR DIAGNOSTIC APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 47 ENTERPRISE IMAGING IT MARKET FOR THERAPEUTIC APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 48 ENTERPRISE IMAGING IT MARKET FOR CLINICAL RESEARCH APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 49 ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 50 ENTERPRISE IMAGING IT MARKET FOR X-RAY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 51 ENTERPRISE IMAGING IT MARKET FOR MRI, BY REGION, 2023-2030 (USD MILLION)

- TABLE 52 ENTERPRISE IMAGING IT MARKET FOR CT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 53 ENTERPRISE IMAGING IT MARKET FOR ULTRASOUND, BY REGION, 2023-2030 (USD MILLION)

- TABLE 54 ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 55 ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 56 ENTERPRISE IMAGING IT MARKET FOR PET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 57 ENTERPRISE IMAGING IT MARKET FOR SPECT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 ENTERPRISE IMAGING IT MARKET FOR ENDOSCOPY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 59 ENTERPRISE IMAGING IT MARKET FOR MAMMOGRAPHY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 60 ENTERPRISE IMAGING IT MARKET FOR FLUOROSCOPY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 61 ENTERPRISE IMAGING IT MARKET FOR ECHOCARDIOGRAPHY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 ENTERPRISE IMAGING IT MARKET FOR OTHER MODALITIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 63 ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 64 ENTERPRISE IMAGING IT MARKET FOR SOFTWARE, BY REGION, 2023-2030 (USD MILLION)

- TABLE 65 ENTERPRISE IMAGING IT MARKET FOR SERVICES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 66 ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 67 ENTERPRISE IMAGING IT MARKET FOR ON-PREMISES SOLUTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 68 ENTERPRISE IMAGING IT MARKET FOR CLOUD-BASED SOLUTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 69 ENTERPRISE IMAGING IT MARKET FOR HYBRID SOLUTIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 70 ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 71 ENTERPRISE IMAGING IT MARKET FOR NEUROLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 72 ENTERPRISE IMAGING IT MARKET FOR CARDIOLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 73 ENTERPRISE IMAGING IT MARKET FOR ONCOLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 74 ENTERPRISE IMAGING IT MARKET FOR ORTHOPEDICS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 75 ENTERPRISE IMAGING IT MARKET FOR OTHER THERAPEUTIC AREAS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 76 ENTERPRISE IMAGING IT MARKET, FOR END USER, 2023-2030 (USD MILLION)

- TABLE 77 ENTERPRISE IMAGING IT MARKET FOR HOSPITALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 78 ENTERPRISE IMAGING IT MARKET FOR DIAGNOSTIC CENTERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 79 ENTERPRISE IMAGING IT MARKET FOR CLINICS & OUTPATIENT SETTINGS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 80 ENTERPRISE IMAGING IT MARKET FOR PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 81 ENTERPRISE IMAGING IT MARKET FOR MEDTECH COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 82 ENTERPRISE IMAGING IT MARKET FOR RESEARCH & ACADEMIC INSTITUTES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 83 ENTERPRISE IMAGING IT MARKET FOR OTHER END USERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 84 ENTERPRISE IMAGING IT MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 85 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 87 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 88 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 90 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 91 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 93 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 94 US: KEY MACROINDICATORS

- TABLE 95 US: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 96 US: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 97 US: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 98 US: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 99 US: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 100 US: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 101 US: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 102 US: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 103 CANADA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 104 CANADA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 105 CANADA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 106 CANADA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 107 CANADA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 108 CANADA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 109 CANADA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 110 CANADA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 111 EUROPE: ENTERPRISE IMAGING IT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 112 EUROPE: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 113 EUROPE: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 114 EUROPE: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 115 EUROPE: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 116 EUROPE: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 117 EUROPE: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 118 EUROPE: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 119 EUROPE: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 120 GERMANY: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 121 GERMANY: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 122 GERMANY: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 123 GERMANY: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 124 GERMANY: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 125 GERMANY: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 126 GERMANY: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 127 GERMANY: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 128 UK: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 129 UK: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 130 UK: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 UK: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 132 UK: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 133 UK: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 134 UK: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 135 UK: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 136 FRANCE: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 137 FRANCE: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 138 FRANCE: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 139 FRANCE: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 140 FRANCE: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 141 FRANCE: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 142 FRANCE: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 143 FRANCE: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 144 ITALY: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 145 ITALY: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 146 ITALY: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 147 ITALY: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 148 ITALY: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 149 ITALY: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 150 ITALY: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 151 ITALY: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 152 SPAIN: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 153 SPAIN: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 154 SPAIN: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 155 SPAIN: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 156 SPAIN: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 157 SPAIN: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 158 SPAIN: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 159 SPAIN: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 160 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 161 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 162 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 163 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 164 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 165 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 166 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 167 REST OF EUROPE: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 168 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 169 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 170 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 171 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 172 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 173 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 174 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 175 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 176 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 177 CHINA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 178 CHINA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 179 CHINA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 CHINA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 181 CHINA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 182 CHINA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 183 CHINA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 184 CHINA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 185 JAPAN: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 186 JAPAN: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 187 JAPAN: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 188 JAPAN: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 189 JAPAN: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 190 JAPAN: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 191 JAPAN: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 192 JAPAN: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 193 INDIA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 194 INDIA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 195 INDIA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 196 INDIA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 197 INDIA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 198 INDIA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 199 INDIA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 200 INDIA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 201 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 202 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 203 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 204 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 205 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 206 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 207 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 208 REST OF ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 209 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 210 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 211 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 212 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 213 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 214 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 215 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 216 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 217 LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 218 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 219 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 220 BRAZIL: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 221 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 222 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 223 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 224 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 225 BRAZIL: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 226 MEXICO: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 227 MEXICO: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 228 MEXICO: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 229 MEXICO: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 230 MEXICO: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 231 MEXICO: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 232 MEXICO: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 233 MEXICO: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 234 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 235 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 236 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 237 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 238 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 239 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 240 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 241 REST OF LATIN AMERICA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 242 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 243 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 244 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 245 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 246 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 247 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 248 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 249 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 250 MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 251 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 252 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 253 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 254 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 255 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 256 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 257 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 258 GCC COUNTRIES: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 259 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2023-2030 (USD MILLION)

- TABLE 260 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2023-2030 (USD MILLION)

- TABLE 261 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET FOR NUCLEAR IMAGING, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 262 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 263 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 264 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 265 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY THERAPEUTIC AREA, 2023-2030 (USD MILLION)

- TABLE 266 REST OF MIDDLE EAST & AFRICA: ENTERPRISE IMAGING IT MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 267 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ENTERPRISE IMAGING IT MARKET, JANUARY 2022-JUNE 2025

- TABLE 268 ENTERPRISE IMAGING IT MARKET: DEGREE OF COMPETITION

- TABLE 269 ENTERPRISE IMAGING IT MARKET: REGION FOOTPRINT

- TABLE 270 ENTERPRISE IMAGING IT MARKET: FUNCTION FOOTPRINT

- TABLE 271 ENTERPRISE IMAGING IT MARKET: APPLICATION FOOTPRINT

- TABLE 272 ENTERPRISE IMAGING IT MARKET: THERAPEUTIC AREA FOOTPRINT

- TABLE 273 ENTERPRISE IMAGING IT MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 274 ENTERPRISE IMAGING IT MARKET: DETAILED LIST OF KEY STARTUP/SME PLAYERS

- TABLE 275 ENTERPRISE IMAGING IT MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY REGION

- TABLE 276 ENTERPRISE IMAGING IT MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY FUNCTION

- TABLE 277 ENTERPRISE IMAGING IT MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY THERAPEUTIC AREA

- TABLE 278 ENTERPRISE IMAGING IT MARKET: SOLUTION LAUNCHES, APPROVALS, AND ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 279 ENTERPRISE IMAGING IT MARKET: DEALS, JANUARY 2022-JUNE 2025

- TABLE 280 ENTERPRISE IMAGING IT MARKET: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 281 AGFA-GEVAERT GROUP: COMPANY OVERVIEW

- TABLE 282 AGFA-GEVAERT GROUP: SOLUTIONS OFFERED

- TABLE 283 AGFA-GEVAERT GROUP: DEALS, JANUARY 2022-JUNE 2025

- TABLE 284 FUJIFILM HOLDINGS CORPORATION: COMPANY OVERVIEW

- TABLE 285 FUJIFILM HOLDINGS CORPORATION: SOLUTIONS OFFERED

- TABLE 286 FUJIFILM HOLDINGS CORPORATION: DEALS, JANUARY 2022-JUNE 2025

- TABLE 287 GE HEALTHCARE: COMPANY OVERVIEW

- TABLE 288 GE HEALTHCARE: SOLUTIONS OFFERED

- TABLE 289 GE HEALTHCARE: SOLUTION LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 290 GE HEALTHCARE: DEALS, JANUARY 2022-JUNE 2025

- TABLE 291 KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

- TABLE 292 KONINKLIJKE PHILIPS N.V.: SOLUTIONS OFFERED

- TABLE 293 KONINKLIJKE PHILIPS N.V.: SOLUTION LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 294 KONINKLIJKE PHILIPS N.V.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 295 KONINKLIJKE PHILIPS N.V.: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 296 SIEMENS HEALTHINEERS AG: COMPANY OVERVIEW

- TABLE 297 SIEMENS HEALTHINEERS AG: SOLUTIONS OFFERED

- TABLE 298 SIEMENS HEALTHINEERS AG: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 299 SIEMENS HEALTHINEERS AG: DEALS, JANUARY 2022-JUNE 2025

- TABLE 300 OPTUM, INC.: COMPANY OVERVIEW

- TABLE 301 OPTUM, INC.: SOLUTIONS OFFERED

- TABLE 302 OPTUM, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 303 SECTRA AB: COMPANY OVERVIEW

- TABLE 304 SECTRA AB: SOLUTIONS OFFERED

- TABLE 305 SECTRA AB: SOLUTION LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 306 SECTRA AB: DEALS, JANUARY 2022-JUNE 2025

- TABLE 307 CANON MEDICAL SYSTEMS CORPORATION: COMPANY OVERVIEW

- TABLE 308 CANON MEDICAL SYSTEMS CORPORATION: SOLUTIONS OFFERED

- TABLE 309 CANON MEDICAL SYSTEMS CORPORATION: DEALS, JANUARY 2022-JUNE 2025

- TABLE 310 CANON MEDICAL SYSTEMS CORPORATION: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 311 MERATIVE: COMPANY OVERVIEW

- TABLE 312 MERATIVE: SOLUTIONS OFFERED

- TABLE 313 MERATIVE: DEALS, JANUARY 2022-JUNE 2025

- TABLE 314 MERATIVE: EXPANSIONS, JANUARY 2022-JUNE 2025

- TABLE 315 PRO MEDICUS, LTD.: COMPANY OVERVIEW

- TABLE 316 PRO MEDICUS, LTD.: SOLUTIONS OFFERED

- TABLE 317 PRO MEDICUS, LTD.: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 318 PRO MEDICUS, LTD.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 319 INTELERAD MEDICAL SYSTEMS INCORPORATED: COMPANY OVERVIEW

- TABLE 320 INTELERAD MEDICAL SYSTEMS INCORPORATED: SOLUTIONS OFFERED

- TABLE 321 INTELERAD MEDICAL SYSTEMS INCORPORATED: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 322 INTELERAD: DEALS, JANUARY 2022-JUNE 2025

- TABLE 323 HYLAND SOFTWARE, INC.: COMPANY OVERVIEW

- TABLE 324 HYLAND SOFTWARE, INC.: SOLUTIONS OFFERED

- TABLE 325 HYLAND SOFTWARE, INC.: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 326 HYLAND SOFTWARE, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 327 INFINITT HEALTHCARE CO., LTD.: COMPANY OVERVIEW

- TABLE 328 INFINITT HEALTHCARE CO., LTD.: SOLUTIONS OFFERED

- TABLE 329 INFINITT HEALTHCARE CO., LTD.: SOLUTION LAUNCHES & APPROVALS, JANUARY 2022-JUNE 2025

- TABLE 330 INFINITT HEALTHCARE CO., LTD.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 331 NOVARAD: COMPANY OVERVIEW

- TABLE 332 NOVARAD: SOLUTIONS OFFERED

- TABLE 333 MACH7 TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 334 MACH7 TECHNOLOGIES: SOLUTIONS OFFERED

- TABLE 335 MACH7 TECHNOLOGIES: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 336 MACH7 TECHNOLOGIES: DEALS, JANUARY 2022-JUNE 2025

- TABLE 337 HERMES MEDICAL SOLUTIONS: COMPANY OVERVIEW

- TABLE 338 HERMES MEDICAL SOLUTIONS: SOLUTIONS OFFERED

- TABLE 339 HERMES MEDICAL SOLUTIONS: SOLUTION LAUNCHES, APPROVALS, AND ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 340 HERMES MEDICAL SOLUTIONS: DEALS, JANUARY 2022-JUNE 2025

- TABLE 341 KONICA MINOLTA, INC.: COMPANY OVERVIEW

- TABLE 342 KONICA MINOLTA, INC.: SOLUTIONS OFFERED

- TABLE 343 KONICA MINOLTA, INC.: SOLUTION LAUNCHES & ENHANCEMENTS, JANUARY 2022-JUNE 2025

- TABLE 344 KONICA MINOLTA, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 345 BRIDGEHEAD SOFTWARE LTD.: COMPANY OVERVIEW

- TABLE 346 BRIDGEHEAD SOFTWARE LTD.: SOLUTIONS OFFERED

- TABLE 347 BRIDGEHEAD SOFTWARE LTD.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 348 SCIMAGE, INC.: COMPANY OVERVIEW

- TABLE 349 SCIMAGE, INC.: SOLUTIONS OFFERED

- TABLE 350 SCIMAGE, INC.: SOLUTION LAUNCHES, JANUARY 2022-JUNE 2025

- TABLE 351 SCIMAGE, INC.: DEALS, JANUARY 2022-JUNE 2025

- TABLE 352 VISUS HEALTH IT GMBH: COMPANY OVERVIEW

- TABLE 353 VISUS HEALTH IT GMBH: SOLUTIONS OFFERED

- TABLE 354 VISUS HEALTH IT GMBH: SOLUTION ENHANCEMENTS, JANUARY 2022-JUNE 2025

List of Figures

- FIGURE 1 ENTERPRISE IMAGING IT MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 PRIMARY SOURCES

- FIGURE 4 INSIGHTS FROM INDUSTRY EXPERTS

- FIGURE 5 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 6 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 7 SUPPLY-SIDE MARKET ESTIMATION

- FIGURE 8 ENTERPRISE IMAGING IT MARKET: REVENUE ESTIMATION APPROACH

- FIGURE 9 BOTTOM-UP APPROACH: END-USER SPENDING ON ENTERPRISE IMAGING IT

- FIGURE 10 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES (2025-2030)

- FIGURE 11 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 12 TOP-DOWN APPROACH

- FIGURE 13 DATA TRIANGULATION METHODOLOGY

- FIGURE 14 ENTERPRISE IMAGING IT MARKET, BY FUNCTION, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 ENTERPRISE IMAGING IT MARKET, BY MODALITY, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 ENTERPRISE IMAGING IT MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 17 ENTERPRISE IMAGING IT MARKET, BY OFFERING, 2025 VS. 2030 (USD MILLION)

- FIGURE 18 ENTERPRISE IMAGING IT MARKET, BY DEPLOYMENT MODE, 2025 VS. 2030 (USD MILLION)

- FIGURE 19 ENTERPRISE IMAGING IT MARKET: GEOGRAPHICAL SNAPSHOT

- FIGURE 20 RISING IMAGING VOLUMES TO DRIVE GROWTH IN ENTERPRISE IMAGING IT MARKET

- FIGURE 21 DIAGNOSTIC APPLICATIONS IN NORTH AMERICA ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 22 INDIA TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 23 GROWTH RATES OF EMERGING ECONOMIES TO BE HIGHER THAN THOSE OF DEVELOPED MARKETS DURING FORECAST PERIOD

- FIGURE 24 ENTERPRISE IMAGING IT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 25 HEALTHCARE SECURITY BREACHES OF 500+ RECORDS IN US, 2009-2024

- FIGURE 26 US: MEDIAN HEALTHCARE DATA BREACH SIZE BY YEAR, 2009-2024

- FIGURE 27 INDIVIDUALS AFFECTED BY HEALTHCARE SECURITY BREACHES IN US, 2009-2023

- FIGURE 28 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 29 ENTERPRISE IMAGING IT MARKET: ECOSYSTEM ANALYSIS

- FIGURE 30 ENTERPRISE IMAGING IT MARKET: SUPPLY CHAIN ANALYSIS (2024)

- FIGURE 31 ENTERPRISE IMAGING IT MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 32 PATENT PUBLICATION TRENDS IN ENTERPRISE IMAGING IT MARKET, 2015-2025

- FIGURE 33 JURISDICTION AND TOP APPLICANT ANALYSIS FOR ENTERPRISE IMAGING IT MARKET

- FIGURE 34 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) FOR ENTERPRISE IMAGING IT MARKET (JANUARY 2015 TO JULY 2025)

- FIGURE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR END USERS

- FIGURE 36 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 38 MARKET POTENTIAL OF AI/GENERATIVE AI IN ENHANCING ENTERPRISE IMAGING IT ACROSS INDUSTRIES

- FIGURE 39 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- FIGURE 40 NORTH AMERICA: ENTERPRISE IMAGING IT MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: ENTERPRISE IMAGING IT MARKET SNAPSHOT

- FIGURE 42 REVENUE ANALYSIS OF KEY PLAYERS IN ENTERPRISE IMAGING IT MARKET, 2020-2024 (USD MILLION)

- FIGURE 43 MARKET SHARE ANALYSIS OF KEY PLAYERS IN ENTERPRISE IMAGING IT MARKET (2024)

- FIGURE 44 ENTERPRISE IMAGING IT MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 45 ENTERPRISE IMAGING IT MARKET: COMPANY FOOTPRINT

- FIGURE 46 ENTERPRISE IMAGING IT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 47 EV/EBITDA OF KEY VENDORS

- FIGURE 48 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 49 ENTERPRISE IMAGING IT MARKET: BRAND/SOFTWARE COMPARITIVE ANALYSIS

- FIGURE 50 AGFA-GEVAERT GROUP: COMPANY SNAPSHOT (2024)

- FIGURE 51 FUJIFILM HOLDINGS CORPORATION: COMPANY SNAPSHOT (2023)

- FIGURE 52 GE HEALTHCARE: COMPANY SNAPSHOT (2024)

- FIGURE 53 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT (2024)

- FIGURE 54 SIEMENS HEALTHINEERS AG: COMPANY SNAPSHOT (2024)

- FIGURE 55 OPTUM, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 56 SECTRA AB: COMPANY SNAPSHOT (2023)

- FIGURE 57 CANON MEDICAL SYSTEMS CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 58 PRO MEDICUS, LTD.: COMPANY SNAPSHOT (2024)

- FIGURE 59 INFINITT HEALTHCARE CO., LTD.: COMPANY SNAPSHOT (2024)

- FIGURE 60 MACH7 TECHNOLOGIES: COMPANY SNAPSHOT (2023)

- FIGURE 61 KONICA MINOLTA, INC.: COMPANY SNAPSHOT (2024)