PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1802927

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1802927

Fluid Transfer System Market by Propulsion & Component (Petrol/Gasoline, Diesel, CNG, Battery Electric, Plug-In Hybrid Electric), System Type, Vehicle Type (Passenger Cars, LCVs, Trucks, and Buses), and Region - Global Forecast to 2032

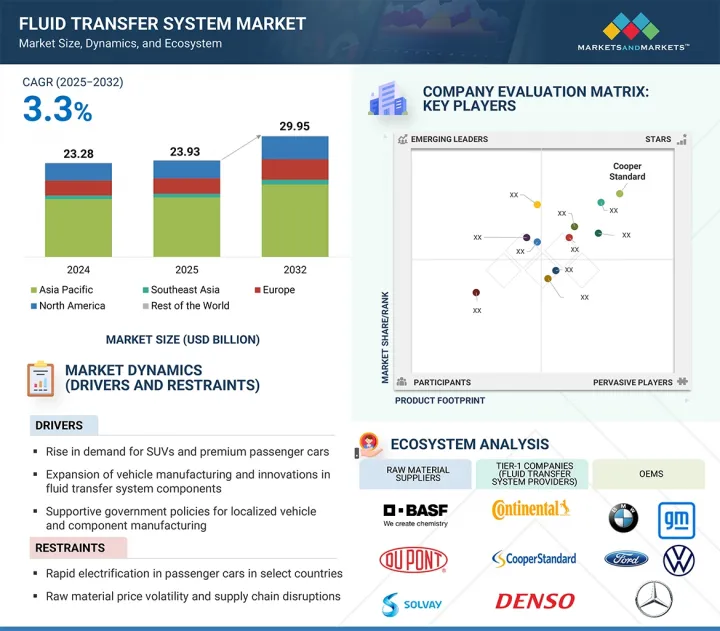

The fluid transfer system market is projected to reach USD 29.95 billion in 2032, from USD 23.93 billion in 2025, with a CAGR of 3.3%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Units Considered | Volume (Thousand Units) and Value (USD Billion) |

| Segments | Propulsion & Component, Vehicle Type, System Type, and Region |

| Regions covered | Asia Pacific, Southeast Asia, Europe, North America, and Rest of the World |

The fluid transfer system market is poised for steady growth, supported by increased vehicle production, stricter emission standards, and broader adoption of advanced mobility technologies. The demand for fluid transfer systems is also driven by their critical role in managing fuel, air, oil, coolant, and other fluids essential for performance, efficiency, and safety across ICE and electric vehicles.

The shift toward premium passenger cars is expanding the use of advanced air conditioning, suspension, and emission control lines, while stricter regulations such as BS-VI and Euro 6 are boosting demand for SCR, DPF, and EVAP lines. Similarly, the growing penetration of EVs is driving new opportunities for thermal management components, including battery, motor, and power electronics cooling lines.

"Suspension systems are expected to show a significant growth rate during the forecast period."

The suspension systems segment in the fluid transfer system market is expected to experience significant growth during the forecast period, driven by rising demand for improved vehicle stability, comfort, and handling. Components related to suspension fluid transfer, such as hydraulic suspension lines, air suspension lines, shock absorber hoses, and anti-roll hoses, are vital for maintaining vehicle stability, minimizing body roll, and allowing adjustable ride height and load management. In passenger cars, trends toward premiumization are accelerating the adoption of air suspension and advanced damping systems, while in commercial vehicles, hydraulic and air suspension lines are essential for durability and load control. The shift to electric buses further boosts demand, as these vehicles increasingly utilize air suspension systems to ensure smoother rides and offset battery weight. As manufacturers invest in advanced suspension technologies to meet consumer expectations for comfort, performance, and safety, the suspension segment is becoming one of the most promising growth areas in the fluid transfer system market.

"Passenger cars are expected to hold the largest share during the forecast period."

The passenger cars segment is expected to account for the largest share of the fluid transfer system market during the forecast period, driven by both volume growth and rapid adoption of advanced vehicle technologies. Increasing demand for premium and mid-range vehicles is expanding the use of air suspension systems and dual-zone or rear-seat air conditioning, boosting requirements for specialized air suspension and A/C fluid transfer lines. Stricter emission standards worldwide, such as BS-VI in India and Euro 6 in Europe, are accelerating the adoption of selective catalytic reduction (SCR) and diesel particulate filter (DPF) lines, as well as other exhaust after-treatment components. At the same time, growing penetration of hybrid and electric passenger cars is creating new opportunities for battery, motor, and DC-DC converter coolant hoses, adding to the traditional demand for fuel and lubrication lines. This combined effect of regulatory compliance, rising comfort features, and electrification ensures that the passenger car segment will remain the largest and most dynamic market for fluid transfer systems.

"Europe's fluid transfer system market is expected to witness notable growth during the forecast period."

Europe is expected to experience significant growth in the fluid transfer system market during the forecast period, supported by its well-established automotive manufacturing base, leadership in technology, and strict regulatory frameworks. The region is home to top OEMs such as Volkswagen, BMW, Mercedes-Benz, Renault, Stellantis, Volvo, and Scania, along with Tier-1 suppliers and fluid transfer specialists like TI Fluid Systems, Continental AG, Gates Corporation, and Parker Hannifin, which ensure continuous innovation and large-scale supply capability. Regulatory changes, including the Euro 6d standard and the upcoming Euro 7 regulations, are increasing demand for advanced emission control lines, exhaust gas recirculation pipes, and thermal management hoses to meet tightening CO2 and NOx reduction standards across passenger cars, trucks, and buses. Electrification is rapidly expanding in both passenger vehicles and heavy commercial trucks, creating opportunities for new product categories such as battery coolant hoses, thermal lines for inverters and motors, and specialized EV climate control tubing. Plug-in hybrid vehicles also support dual demands, maintaining requirements for conventional fuel and oil lines while opening up opportunities in EV cooling and heating systems. Europe's strong truck and bus manufacturing sector, led by Daimler Truck, MAN, Iveco, and Volvo, is further increasing demand for durable high-pressure fuel lines, SCR and EGR assemblies, and thermal hoses, as fleets work to meet stricter emission standards and electrification goals.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various organizations operating in this market.

- By Company Type: Tier 1 - 32%, Tier 2 - 45%, and Tier 3 - 23%

- By Designation: Directors - 36%, Managers - 43%, and Others - 21%

- By Region: Asia Pacific - 36%, Southeast Asia - 13%, Europe - 24%, North America - 21%, and Rest of the World - 6%

The fluid transfer system market is led by major companies, including Cooper Standard (US), TI Fluid Systems (UK), Sumitomo Riko Company Limited (Japan), Parker Hannifin Corp (US), and Gates Corporation (US). These firms are expanding their product ranges to reinforce their market position.

Research Coverage:

The report covers the fluid transfer system market by propulsion & component {petrol/gasoline [intake hose, vacuum hose, fuel feed line, feed return line, fuel leak-off assembly, turbocharger oil feed line, turbocharger oil drain line, turbocharger coolant line, turbocharger coolant return line, positive crankcase ventilation (PCV) hose, vacuum modulator hose, dipstick tube, fluid return hose, pressure control solenoid hose, transmission oil cooler lines, hydraulic power steering hose, fuel delivery line, high-pressure fuel injection line/direct injection line, fuel rail, CNG tube, CNG hose, fuel vapor vent line, fuel injector line, fuel filler neck, fuel filler line, thermal line, expansion valve tube, A/C cabin climate control, radiator hose, reservoir, overflow hose, bypass hose, DC-DC converter cooling hose, motor cooling hose, battery coolant hose, A/C drain line, hydraulic suspension line, air suspension line, shock absorber hose, anti-roll hose, brake and clutch hose & line assembly, vacuum booster hose, brake bundle assembly, EGR tube & assembly, SCR tube & assembly, EVAP line, differential pressure hose, tailpipe, sunroof drain hose, windshield washer hose, power door lock hose, oil line], diesel, CNG, battery electric, and plug-in hybrid electric}, system type (engine, transmission, power steering, fuel delivery, thermal management, suspension, brake & clutch, exhaust, body & exterior, and lubrication), vehicle type (passenger cars, light commercial vehicles, trucks, and buses), and region. It also provides an in-depth competitive analysis of key market players, their company profiles, critical observations related to product and business offerings, recent developments, and growth strategies.

Key Benefits of Buying this Report:

The report serves as a valuable resource for market leaders and new entrants by providing insights into the closest approximations of revenue numbers for the fluid transfer system market and its subsegments. It aids stakeholders in comprehending the competitive landscape, allowing them to position their businesses effectively and devise suitable go-to-market strategies. Additionally, the report sheds light on the market pulse, outlining key drivers, restraints, challenges, and opportunities within the industry. It also offers an understanding of the current and future pricing trends related to the fluid transfer system market, equipping stakeholders with essential information for their decision-making processes.

The report provides insight into the following:

- Analysis of drivers (rise in demand for SUVs and premium passenger cars, expansion of vehicle manufacturing and innovation in fluid transfer system components, supportive government policies for localized vehicle and component manufacturing), restraints (growing electrification in passenger cars in select countries), opportunities (rapid adoption of PHEVs, sustained demand in trucks amid slower rate of electrification, innovations in thermal management systems for electrified powertrains), and challenges (electrification in public transport, tariff-driven procurement volatility and system-level disruptions)

- Product Development/Innovation: Detailed insights into upcoming technologies, R&D activities, and product launches in the fluid transfer system market

- Market Development: Comprehensive information about lucrative markets; this report analyzes the fluid transfer system market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the fluid transfer system market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and service offerings of leading players in the fluid transfer system market, such as Cooper Standard (US), TI Fluid Systems (UK), Sumitomo Riko Company Limited (Japan), Parker Hannifin Corp (US), and Gates Corporation (US)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary participants

- 2.1.2.2 Primary interviews from demand and supply sides

- 2.1.2.3 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FLUID TRANSFER SYSTEM MARKET

- 4.2 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE

- 4.3 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE

- 4.4 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION

- 4.5 FLUID TRANSFER SYSTEM MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rise in demand for SUVs and premium passenger cars

- 5.2.1.2 Expansion of vehicle manufacturing and innovations in fluid transfer systems

- 5.2.1.3 Supportive government policies for localized manufacturing

- 5.2.2 RESTRAINTS

- 5.2.2.1 Electrification of passenger cars in select countries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rapid adoption of PHEVs

- 5.2.3.2 Sustained demand in trucks due to slower rate of electrification

- 5.2.3.3 Advances in thermal management systems for electrified powertrains

- 5.2.4 CHALLENGES

- 5.2.4.1 Shift toward electric buses and municipal EV fleets

- 5.2.4.2 Tariff-driven procurement volatility and system-level disruptions

- 5.2.1 DRIVERS

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE OF FLUID TRANSFER COMPONENTS OFFERED BY KEY PLAYERS

- 5.4.2 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE

- 5.4.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 VCOLLAB'S SOLUTION IMPROVES SIMULATION EFFICIENCY FOR COOPER STANDARD

- 5.7.2 FLUID COOLING SYSTEMS' PROCESS COOLING SOLUTION ENHANCES ALUMINUM WELDING PROCESS FOR FORD

- 5.7.3 LUCAS-MILHAUPT'S FLUX-FREE BRAZING PROCESS ENSURES LEAK-FREE FUEL SENDERS FOR FORD

- 5.8 PATENT ANALYSIS

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Multi-layer hose and tube technology

- 5.9.1.2 Advanced materials and composites

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Additive manufacturing

- 5.9.2.2 Automation and control systems

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 EV thermal management

- 5.9.1 KEY TECHNOLOGIES

- 5.10 TRADE ANALYSIS

- 5.10.1 IMPORT SCENARIO (HS CODE 4009)

- 5.10.2 EXPORT SCENARIO (HS CODE 4009)

- 5.11 TARIFF AND REGULATORY LANDSCAPE

- 5.11.1 TARIFF DATA

- 5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.3 REGULATORY ANALYSIS FOR FLUID TRANSFER SYSTEM MARKET

- 5.11.3.1 US

- 5.11.3.2 China

- 5.11.3.3 Japan

- 5.11.3.4 India

- 5.11.3.5 South Korea

- 5.11.3.6 Europe

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.13.2 BUYING CRITERIA

- 5.14 IMPACT OF AI

- 5.15 OEM AND TIER-1 SOURCING/ADOPTION STRATEGIES

- 5.15.1 OEM SOURCING STRATEGIES

- 5.15.2 TIER-1 ADOPTION AND DIFFERENTIATION STRATEGIES

- 5.16 DIGITALIZATION AND SMART MANUFACTURING INITIATIVES

- 5.16.1 MODULAR, AUTOMATED, AND TRACEABLE PRODUCTION SYSTEMS

- 5.16.2 SMART MANUFACTURING PLATFORMS ENABLING PREDICTIVE MAINTENANCE AND REAL-TIME PROCESS OPTIMIZATION

- 5.16.3 EMBEDDED SENSOR TECHNOLOGIES AND ADVANCED MATERIALS

- 5.16.4 SCALABLE DIGITAL MANUFACTURING SUPPORTING ELECTRIFICATION

- 5.16.5 AI-DRIVEN QUALITY CHECKS, ADDITIVE MANUFACTURING, AND 5G CONNECTIVITY

- 5.17 SHIFT TOWARD ELECTRIFICATION

- 5.17.1 DECLINE IN CONVENTIONAL ICE FLUID TRANSFER SYSTEMS

- 5.17.2 ELEVATED DEMAND FOR EV-DRIVEN FLUID TRANSFER SYSTEMS

- 5.17.3 RISE IN MODULAR AND INTEGRATED ASSEMBLIES

- 5.17.4 AFTERMARKET'S SHIFT AWAY FROM ICE FLUID TRANSFER SYSTEMS

- 5.18 MATERIAL ANALYSIS, BY FLUID TRANSFER COMPONENT

- 5.19 SUPPLIER ANALYSIS, BY FLUID TRANSFER SYSTEM

6 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION AND COMPONENT

- 6.1 INTRODUCTION

- 6.2 PETROL/GASOLINE

- 6.2.1 RISING ADOPTION OF TURBOCHARGED ENGINES TO DRIVE MARKET

- 6.3 DIESEL

- 6.3.1 INCREASING STRINGENCY OF NOX EMISSION REGULATIONS TO DRIVE MARKET

- 6.4 CNG

- 6.4.1 GROWING INCLINATION TOWARD CLEANER FUEL ALTERNATIVES TO DRIVE MARKET

- 6.5 BATTERY ELECTRIC

- 6.5.1 EMERGING ELECTRIFICATION TRENDS TO DRIVE MARKET

- 6.6 PLUG-IN HYBRID ELECTRIC

- 6.6.1 CONSUMER DEMAND FOR FUEL EFFICIENCY AND DYNAMIC PERFORMANCE TO DRIVE MARKET

- 6.7 PRIMARY INSIGHTS

7 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE

- 7.1 INTRODUCTION

- 7.2 PASSENGER CARS

- 7.2.1 STRICTER EMISSION NORMS AND SURGE IN ELECTRIFICATION TO DRIVE MARKET

- 7.3 LIGHT COMMERCIAL VEHICLES

- 7.3.1 HEIGHTENED ADOPTION OF AUTOMATIC TRANSMISSIONS TO DRIVE MARKET

- 7.4 TRUCKS

- 7.4.1 RAPID INDUSTRIALIZATION AND INCREASED LOGISTICS ACTIVITIES TO DRIVE MARKET

- 7.5 BUSES

- 7.5.1 INTEGRATION OF AIR SUSPENSION IN NEW ELECTRIC BUSES TO DRIVE MARKET

- 7.6 PRIMARY INSIGHTS

8 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE

- 8.1 INTRODUCTION

- 8.2 ENGINE

- 8.2.1 NEED FOR HEAT RESISTANCE AND PRESSURE TOLERANCE TO DRIVE MARKET

- 8.3 TRANSMISSION

- 8.3.1 RISE OF AUTOMATIC TRANSMISSION DESIGNS TO DRIVE MARKET

- 8.4 POWER STEERING

- 8.4.1 CONTINUED RELIANCE ON HYDRAULIC STEERING IN COMMERCIAL VEHICLES TO DRIVE MARKET

- 8.5 FUEL DELIVERY

- 8.5.1 RIGOROUS EMISSION NORMS AND ELEVATED CNG ADOPTION TO DRIVE MARKET

- 8.6 THERMAL MANAGEMENT

- 8.6.1 SHIFT TOWARD HIGHER CAPACITY COOLING SYSTEMS TO DRIVE MARKET

- 8.7 SUSPENSION

- 8.7.1 HIGH DEMAND FOR IMPROVED RIDE COMFORT AND DURABILITY TO DRIVE MARKET

- 8.8 BRAKE & CLUTCH

- 8.8.1 IMPLEMENTATION OF STRICT VEHICLE SAFETY STANDARDS TO DRIVE MARKET

- 8.9 EXHAUST

- 8.9.1 WIDE ADOPTION OF AFTERTREATMENT TECHNOLOGIES IN COMMERCIAL VEHICLES TO DRIVE MARKET

- 8.10 BODY & EXTERIOR

- 8.10.1 INTEGRATION OF PREMIUM COMFORT AND SAFETY FEATURES IN MASS-MARKET MODELS TO DRIVE MARKET

- 8.11 LUBRICATION

- 8.11.1 EXPANSION OF DOWNSIZED ENGINES TO DRIVE MARKET

- 8.12 PRIMARY INSIGHTS

9 FLUID TRANSFER SYSTEM MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 ASIA PACIFIC

- 9.2.1 MACROECONOMIC OUTLOOK

- 9.2.2 CHINA

- 9.2.2.1 Domestic OEM dominance and high NEV growth to drive market

- 9.2.3 INDIA

- 9.2.3.1 Emission compliance and local manufacturing to drive market

- 9.2.4 JAPAN

- 9.2.4.1 Dual-propulsion vehicle trends to drive market

- 9.2.5 SOUTH KOREA

- 9.2.5.1 Rising EV output to drive market

- 9.3 SOUTHEAST ASIA

- 9.3.1 MACROECONOMIC OUTLOOK

- 9.3.2 THAILAND

- 9.3.2.1 Expansion of domestic automotive manufacturing to drive market

- 9.3.3 INDONESIA

- 9.3.3.1 OEM investment in modern gasoline engine platforms to drive market

- 9.3.4 VIETNAM

- 9.3.4.1 Surge in vehicle electrification to drive market

- 9.3.5 PHILIPPINES

- 9.3.5.1 Urbanization and financing trends to drive market

- 9.4 NORTH AMERICA

- 9.4.1 MACROECONOMIC OUTLOOK

- 9.4.2 US

- 9.4.2.1 Plans for increasing domestic manufacturing to drive market

- 9.4.3 CANADA

- 9.4.3.1 High penetration of light commercial vehicles and trucks to drive market

- 9.4.4 MEXICO

- 9.4.4.1 Expansion of advanced powertrain production to drive market

- 9.5 EUROPE

- 9.5.1 MICROECONOMIC OUTLOOK

- 9.5.2 GERMANY

- 9.5.2.1 Collaborations between OEMs and Tier-1 suppliers to drive market

- 9.5.3 FRANCE

- 9.5.3.1 Focus on emission reduction and transition toward electrification to drive market

- 9.5.4 ITALY

- 9.5.4.1 High demand for fluid transfer systems in commercial vehicle applications to drive market

- 9.5.5 SPAIN

- 9.5.5.1 Diverse vehicle production mix to drive market

- 9.5.6 UK

- 9.5.6.1 Fleet electrification momentum to drive market

- 9.5.7 REST OF EUROPE

- 9.6 REST OF THE WORLD

- 9.6.1 MACROECONOMIC OUTLOOK

- 9.6.2 SOUTH AFRICA

- 9.6.2.1 Growing automotive manufacturing to drive market

- 9.6.3 KENYA

- 9.6.3.1 Increasing vehicle assembly activities to drive market

- 9.6.4 EGYPT

- 9.6.4.1 Established automotive manufacturing base to drive market

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 10.3 MARKET SHARE ANALYSIS, 2024

- 10.4 REVENUE ANALYSIS, 2020-2024

- 10.5 COMPANY VALUATION AND FINANCIAL METRICS

- 10.6 BRAND/PRODUCT COMPARISON

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT

- 10.7.5.1 Company footprint

- 10.7.5.2 Region footprint

- 10.7.5.3 System type footprint

- 10.7.5.4 Propulsion footprint

- 10.7.5.5 Vehicle type footprint

- 10.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING

- 10.8.5.1 List of start-ups/SMEs

- 10.8.5.2 Competitive benchmarking of start-ups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

- 10.9.3 EXPANSIONS

- 10.9.4 OTHER DEVELOPMENTS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 COOPER STANDARD

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches/developments

- 11.1.1.3.2 Deals

- 11.1.1.3.3 Other developments

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 TI FLUID SYSTEMS

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Solutions offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches/developments

- 11.1.2.3.2 Deals

- 11.1.2.3.3 Expansions

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 SUMITOMO RIKO COMPANY LIMITED

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Expansions

- 11.1.3.3.2 Other developments

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 PARKER HANNIFIN CORP

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Solutions offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Product launches/developments

- 11.1.4.3.2 Deals

- 11.1.4.3.3 Expansions

- 11.1.4.3.4 Other developments

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 GATES CORPORATION

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Product launches/developments

- 11.1.5.4 MnM view

- 11.1.5.4.1 Key strengths

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 SANOH INDUSTRIAL CO., LTD.

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Solutions offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Other developments

- 11.1.7 CONTINENTAL AG

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Solutions offered

- 11.1.7.3 Recent development

- 11.1.7.3.1 Expansions

- 11.1.8 DENSO CORPORATION

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions offered

- 11.1.9 HUTCHINSON

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Solutions offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Product launches/developments

- 11.1.9.3.2 Expansions

- 11.1.10 NICHIRIN

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Solutions offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Deals

- 11.1.11 USUI CO. LTD.

- 11.1.11.1 Business overview

- 11.1.11.2 Products/Solutions offered

- 11.1.11.3 Recent developments

- 11.1.11.3.1 Other developments

- 11.1.12 KONGSBERG AUTOMOTIVE

- 11.1.12.1 Business overview

- 11.1.12.2 Products/Solutions offered

- 11.1.12.3 Recent developments

- 11.1.12.3.1 Other developments

- 11.1.13 AKWEL

- 11.1.13.1 Business overview

- 11.1.13.2 Products/Solutions offered

- 11.1.13.3 Recent developments

- 11.1.13.3.1 Expansions

- 11.1.13.3.2 Other developments

- 11.1.14 IMPERIAL AUTO

- 11.1.14.1 Business overview

- 11.1.14.2 Products/Solutions offered

- 11.1.14.3 Recent developments

- 11.1.14.3.1 Deals

- 11.1.14.3.2 Expansions

- 11.1.15 ROBERT BOSCH GMBH

- 11.1.15.1 Business overview

- 11.1.15.2 Products/Solutions offered

- 11.1.15.3 Recent developments

- 11.1.15.3.1 Product launches/developments

- 11.1.1 COOPER STANDARD

- 11.2 OTHER PLAYERS

- 11.2.1 LANDER TUBULAR PRODUCTS

- 11.2.2 TRISTONE

- 11.2.3 FLEXITECH

- 11.2.4 DELFINGEN

- 11.2.5 TALBROS

- 11.2.6 MANULI RYCO GROUP

- 11.2.7 GRACO INC.

- 11.2.8 NEWAGE INDUSTRIES

- 11.2.9 ARAYMOND ET CIE

- 11.2.10 CALEX AUTO

- 11.2.11 ARTH RUBBERS

- 11.2.12 MARUYASU INDUSTRIES CO., LTD.

12 RECOMMENDATIONS BY MARKETSANDMARKETS

- 12.1 ASIA PACIFIC TO BE LEADING MARKET FOR FLUID TRANSFER SYSTEMS

- 12.2 COMPANIES' EMPHASIS ON LIGHTWEIGHT MATERIALS

- 12.3 TREND OF ELECTRIFICATION

- 12.4 HIGH DEMAND FOR HVAC AND AIR SUSPENSION FLUID TRANSFER SYSTEMS IN COMMERCIAL VEHICLES

- 12.5 CONCLUSION

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.4.1 FLUID TRANSFER SYSTEM MARKET, FOR TWO & THREE-WHEELERS AND OFF-HIGHWAY VEHICLES AT REGIONAL LEVEL

- 13.4.2 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, FOR ADDITIONAL COUNTRIES

- 13.4.3 COMPANY INFORMATION

- 13.4.3.1 Profiling of additional market players (up to five)

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS

List of Tables

- TABLE 1 MARKET DEFINITION, BY VEHICLE TYPE

- TABLE 2 MARKET DEFINITION, BY PROPULSION

- TABLE 3 MARKET DEFINITION, BY COMPONENT

- TABLE 4 MARKET DEFINITION, BY SYSTEM TYPE

- TABLE 5 INCLUSIONS AND EXCLUSIONS

- TABLE 6 CURRENCY EXCHANGE RATES, 2019-2024

- TABLE 7 IMPACT OF MARKET DYNAMICS ON FLUID TRANSFER SYSTEM MARKET

- TABLE 8 AVERAGE SELLING PRICE OF FLUID TRANSFER COMPONENTS OFFERED BY KEY PLAYERS, 2024 (USD)

- TABLE 9 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2024 (USD)

- TABLE 10 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024 (USD)

- TABLE 11 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 12 PATENT ANALYSIS

- TABLE 13 IMPORT DATA FOR HS CODE 4009-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 14 EXPORT DATA FOR HS CODE 4009-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 15 IMPORT TARIFFS ON FLUID TRANSFER COMPONENTS

- TABLE 16 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 EURO-5 VS. EURO-6 VEHICLE EMISSION STANDARDS ON NEW EUROPEAN DRIVING CYCLE

- TABLE 21 KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE (%)

- TABLE 23 KEY BUYING CRITERIA, BY VEHICLE TYPE

- TABLE 24 MATERIAL ANALYSIS, BY FLUID TRANSFER COMPONENT

- TABLE 25 BRAKE & CLUTCH FLUID TRANSFER SYSTEM SUPPLIERS, 2022-2025

- TABLE 26 FUEL DELIVERY FLUID TRANSFER SYSTEM SUPPLIERS, 2022-2025

- TABLE 27 THERMAL MANAGEMENT FLUID TRANSFER SYSTEM SUPPLIERS, 2022-2025

- TABLE 28 POWER STEERING FLUID TRANSFER SYSTEM SUPPLIERS, 2022-2025

- TABLE 29 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION, 2021-2024 (THOUSAND UNITS)

- TABLE 30 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION, 2025-2032 (THOUSAND UNITS)

- TABLE 31 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION, 2021-2024 (USD MILLION)

- TABLE 32 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION, 2025-2032 (USD MILLION)

- TABLE 33 PETROL/GASOLINE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 34 PETROL/GASOLINE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 35 PETROL/GASOLINE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 36 PETROL/GASOLINE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 37 DIESEL: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 38 DIESEL: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 39 DIESEL: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 40 DIESEL: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 41 CNG: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 42 CNG: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 43 CNG: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 44 CNG: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 45 BATTERY ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 46 BATTERY ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 47 BATTERY ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 48 BATTERY ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 49 PLUG-IN HYBRID ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 50 PLUG-IN HYBRID ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 51 PLUG-IN HYBRID ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 52 PLUG-IN HYBRID ELECTRIC: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 53 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 54 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 55 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, 2021-2024 (USD MILLION)

- TABLE 56 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, 2025-2032 (USD MILLION)

- TABLE 57 PASSENGER CARS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 58 PASSENGER CARS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 59 PASSENGER CARS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 60 PASSENGER CARS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 61 LIGHT COMMERCIAL VEHICLES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 62 LIGHT COMMERCIAL VEHICLES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 63 LIGHT COMMERCIAL VEHICLES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 64 LIGHT COMMERCIAL VEHICLES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 65 TRUCKS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 66 TRUCKS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 67 TRUCKS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 68 TRUCKS: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 69 BUSES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 70 BUSES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 71 BUSES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 72 BUSES: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 73 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 74 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE, 2025-2032 (THOUSAND UNITS)

- TABLE 75 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE, 2021-2024 (USD MILLION)

- TABLE 76 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE, 2025-2032 (USD MILLION)

- TABLE 77 ENGINE: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 78 ENGINE: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 79 ENGINE: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 80 ENGINE: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 81 TRANSMISSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 82 TRANSMISSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 83 TRANSMISSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 84 TRANSMISSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 85 POWER STEERING: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 86 POWER STEERING: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 87 POWER STEERING: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 88 POWER STEERING: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 89 FUEL DELIVERY: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 90 FUEL DELIVERY: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 91 FUEL DELIVERY: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 92 FUEL DELIVERY: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 93 THERMAL MANAGEMENT: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 94 THERMAL MANAGEMENT: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 95 THERMAL MANAGEMENT: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 96 THERMAL MANAGEMENT: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 97 SUSPENSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 98 SUSPENSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 99 SUSPENSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 100 SUSPENSION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 101 BRAKE & CLUTCH: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 102 BRAKE & CLUTCH: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 103 BRAKE & CLUTCH: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 104 BRAKE & CLUTCH: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 105 EXHAUST: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 106 EXHAUST: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 107 EXHAUST: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 108 EXHAUST: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 109 BODY & EXTERIOR: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 110 BODY & EXTERIOR: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 111 BODY & EXTERIOR: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 112 BODY & EXTERIOR: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 113 LUBRICATION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 114 LUBRICATION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 115 LUBRICATION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 116 LUBRICATION: FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 117 FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (THOUSAND UNITS)

- TABLE 118 FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (THOUSAND UNITS)

- TABLE 119 FLUID TRANSFER SYSTEM MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 120 FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025-2032 (USD MILLION)

- TABLE 121 ASIA PACIFIC: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 122 ASIA PACIFIC: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 123 ASIA PACIFIC: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 124 ASIA PACIFIC: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 125 CHINA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 126 CHINA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 127 CHINA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 128 CHINA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 129 INDIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 130 INDIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 131 INDIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 132 INDIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 133 JAPAN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 134 JAPAN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 135 JAPAN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 136 JAPAN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 137 SOUTH KOREA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 138 SOUTH KOREA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 139 SOUTH KOREA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 140 SOUTH KOREA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 141 SOUTHEAST ASIA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 142 SOUTHEAST ASIA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 143 SOUTHEAST ASIA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 144 SOUTHEAST ASIA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 145 THAILAND: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 146 THAILAND: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 147 THAILAND: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 148 THAILAND: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 149 INDONESIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 150 INDONESIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 151 INDONESIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 152 INDONESIA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 153 VIETNAM: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 154 VIETNAM: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 155 VIETNAM: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 156 VIETNAM: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 157 PHILIPPINES: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 158 PHILIPPINES: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 159 PHILIPPINES: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 160 PHILIPPINES: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 161 NORTH AMERICA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 162 NORTH AMERICA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 163 NORTH AMERICA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 164 NORTH AMERICA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 165 US: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 166 US: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 167 US: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 168 US: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 169 CANADA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 170 CANADA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 171 CANADA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 172 CANADA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 173 MEXICO: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 174 MEXICO: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 175 MEXICO: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 176 MEXICO: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 177 EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 178 EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 179 EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 180 EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 181 GERMANY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 182 GERMANY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 183 GERMANY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 184 GERMANY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 185 FRANCE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 186 FRANCE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 187 FRANCE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 188 FRANCE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 189 ITALY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 190 ITALY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 191 ITALY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 192 ITALY: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 193 SPAIN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 194 SPAIN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 195 SPAIN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 196 SPAIN: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 197 UK: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 198 UK: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 199 UK: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 200 UK: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 201 REST OF EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 202 REST OF EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 203 REST OF EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 204 REST OF EUROPE: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 205 REST OF THE WORLD: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (THOUSAND UNITS)

- TABLE 206 REST OF THE WORLD: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (THOUSAND UNITS)

- TABLE 207 REST OF THE WORLD: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 208 REST OF THE WORLD: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025-2032 (USD MILLION)

- TABLE 209 SOUTH AFRICA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 210 SOUTH AFRICA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 211 SOUTH AFRICA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 212 SOUTH AFRICA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 213 KENYA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 214 KENYA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 215 KENYA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 216 KENYA: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 217 EGYPT: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (THOUSAND UNITS)

- TABLE 218 EGYPT: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (THOUSAND UNITS)

- TABLE 219 EGYPT: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2021-2024 (USD MILLION)

- TABLE 220 EGYPT: FLUID TRANSFER SYSTEM MARKET, BY COMPONENT, 2025-2032 (USD MILLION)

- TABLE 221 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- TABLE 222 FLUID TRANSFER SYSTEM MARKET: DEGREE OF COMPETITION, 2024

- TABLE 223 REGION FOOTPRINT

- TABLE 224 SYSTEM TYPE FOOTPRINT

- TABLE 225 PROPULSION FOOTPRINT

- TABLE 226 VEHICLE TYPE FOOTPRINT

- TABLE 227 LIST OF START-UPS/SMES

- TABLE 228 COMPETITIVE BENCHMARKING OF START-UPS/SMES

- TABLE 229 FLUID TRANSFER SYSTEM MARKET: PRODUCT LAUNCHES/ DEVELOPMENTS, 2022-2025

- TABLE 230 FLUID TRANSFER SYSTEM MARKET: DEALS, 2022-2025

- TABLE 231 FLUID TRANSFER SYSTEM MARKET: EXPANSIONS, 2022-2025

- TABLE 232 FLUID TRANSFER SYSTEM MARKET: OTHER DEVELOPMENTS, 2022-2025

- TABLE 233 COOPER STANDARD: COMPANY OVERVIEW

- TABLE 234 COOPER STANDARD: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 235 COOPER STANDARD: PRODUCTS/SOLUTIONS OFFERED

- TABLE 236 COOPER STANDARD: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 237 COOPER STANDARD: DEALS

- TABLE 238 COOPER STANDARD: OTHER DEVELOPMENTS

- TABLE 239 TI FLUID SYSTEMS: COMPANY OVERVIEW

- TABLE 240 TI FLUID SYSTEMS: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 241 TI FLUID SYSTEMS: PRODUCTS/SOLUTIONS OFFERED

- TABLE 242 TI FLUID SYSTEMS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 243 TI FLUID SYSTEMS: DEALS

- TABLE 244 TI FLUID SYSTEMS: EXPANSIONS

- TABLE 245 SUMITOMO RIKO COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 246 SUMITOMO RIKO COMPANY LIMITED: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 247 SUMITOMO RIKO COMPANY LIMITED: PRODUCTS/SOLUTIONS OFFERED

- TABLE 248 SUMITOMO RIKO COMPANY LIMITED: EXPANSIONS

- TABLE 249 SUMITOMO RIKO COMPANY LIMITED: OTHER DEVELOPMENTS

- TABLE 250 PARKER HANNIFIN CORP: COMPANY OVERVIEW

- TABLE 251 PARKER HANNIFIN CORP: PRODUCTS/SOLUTIONS OFFERED

- TABLE 252 PARKER HANNIFIN CORP: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 253 PARKER HANNIFIN CORP: DEALS

- TABLE 254 PARKER HANNIFIN CORP: EXPANSIONS

- TABLE 255 PARKER HANNIFIN CORP: OTHER DEVELOPMENTS

- TABLE 256 GATES CORPORATION: COMPANY OVERVIEW

- TABLE 257 GATES CORPORATION: PRODUCTS/SOLUTIONS OFFERED

- TABLE 258 GATES CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 259 SANOH INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 260 SANOH INDUSTRIAL CO., LTD.: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 261 SANOH INDUSTRIAL CO., LTD.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 262 SANOH INDUSTRIAL CO., LTD.: OTHER DEVELOPMENTS

- TABLE 263 CONTINENTAL AG: COMPANY OVERVIEW

- TABLE 264 CONTINENTAL AG: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 265 CONTINENTAL AG: PRODUCTS/SOLUTIONS OFFERED

- TABLE 266 CONTINENTAL AG: EXPANSIONS

- TABLE 267 DENSO CORPORATION: COMPANY OVERVIEW

- TABLE 268 DENSO CORPORATION: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 269 DENSO CORPORATION: PRODUCTS/SOLUTIONS OFFERED

- TABLE 270 HUTCHINSON: COMPANY OVERVIEW

- TABLE 271 HUTCHINSON: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 272 HUTCHINSON: PRODUCTS/SOLUTIONS OFFERED

- TABLE 273 HUTCHINSON: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 274 HUTCHINSON: EXPANSIONS

- TABLE 275 NICHIRIN: COMPANY OVERVIEW

- TABLE 276 NICHIRIN: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 277 NICHIRIN: PRODUCTS/SOLUTIONS OFFERED

- TABLE 278 NICHIRIN: DEALS

- TABLE 279 USUI CO. LTD.: COMPANY OVERVIEW

- TABLE 280 USUI CO. LTD.: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 281 USUI CO. LTD.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 282 USUI CO. LTD.: OTHER DEVELOPMENTS

- TABLE 283 KONGSBERG AUTOMOTIVE: COMPANY OVERVIEW

- TABLE 284 KONGSBERG AUTOMOTIVE: PRODUCTS/SOLUTIONS OFFERED

- TABLE 285 KONGSBERG AUTOMOTIVE: OTHER DEVELOPMENTS

- TABLE 286 AKWEL: COMPANY OVERVIEW

- TABLE 287 AKWEL: PRODUCTS/SOLUTIONS OFFERED

- TABLE 288 AKWEL: EXPANSIONS

- TABLE 289 AKWEL: OTHER DEVELOPMENTS

- TABLE 290 IMPERIAL AUTO: COMPANY OVERVIEW

- TABLE 291 IMPERIAL AUTO: PRODUCTS/SOLUTIONS OFFERED

- TABLE 292 IMPERIAL AUTO: DEALS

- TABLE 293 IMPERIAL AUTO: EXPANSIONS

- TABLE 294 ROBERT BOSCH GMBH: COMPANY OVERVIEW

- TABLE 295 ROBERT BOSCH GMBH: MAJOR FLUID TRANSFER COMPONENT SUPPLY AGREEMENTS

- TABLE 296 ROBERT BOSCH GMBH: PRODUCTS/SOLUTIONS OFFERED

- TABLE 297 ROBERT BOSCH GMBH: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 298 LANDER TUBULAR PRODUCTS: COMPANY OVERVIEW

- TABLE 299 TRISTONE: COMPANY OVERVIEW

- TABLE 300 FLEXITECH: COMPANY OVERVIEW

- TABLE 301 DELFINGEN: COMPANY OVERVIEW

- TABLE 302 TALBROS: COMPANY OVERVIEW

- TABLE 303 MANULI RYCO GROUP: COMPANY OVERVIEW

- TABLE 304 GRACO INC.: COMPANY OVERVIEW

- TABLE 305 NEWAGE INDUSTRIES: COMPANY OVERVIEW

- TABLE 306 ARAYMOND ET CIE: COMPANY OVERVIEW

- TABLE 307 CALEX AUTO: COMPANY OVERVIEW

- TABLE 308 ARTH RUBBERS: COMPANY OVERVIEW

- TABLE 309 MARUYASU INDUSTRIES CO., LTD.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 FLUID TRANSFER SYSTEM MARKET SEGMENTATION

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 RESEARCH DESIGN MODEL

- FIGURE 4 PRIMARY INSIGHTS

- FIGURE 5 MARKET SIZE ESTIMATION: HYPOTHESIS BUILDING

- FIGURE 6 BOTTOM-UP APPROACH

- FIGURE 7 MARKET SIZE ESTIMATION NOTES

- FIGURE 8 DATA TRIANGULATION

- FIGURE 9 GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS

- FIGURE 10 DEMAND AND SUPPLY-SIDE FACTOR ANALYSIS

- FIGURE 11 FLUID TRANSFER SYSTEM MARKET OUTLOOK

- FIGURE 12 FLUID TRANSFER SYSTEM MARKET, BY REGION

- FIGURE 13 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE

- FIGURE 14 KEY PLAYERS IN FLUID TRANSFER SYSTEM MARKET

- FIGURE 15 ADVANCEMENTS IN FLUID TRANSFER TECHNOLOGIES TO DRIVE MARKET

- FIGURE 16 PASSENGER CARS TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 17 BRAKE & CLUTCH SEGMENT TO HOLD HIGHEST SHARE IN 2032

- FIGURE 18 BATTERY ELECTRIC TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 19 ASIA PACIFIC TO SURPASS OTHER REGIONAL MARKETS IN 2025

- FIGURE 20 FLUID TRANSFER SYSTEM MARKET DYNAMICS

- FIGURE 21 SUV REGISTRATIONS IN EUROPE, 2024

- FIGURE 22 COMPARATIVE OVERVIEW OF HOSE MATERIALS AND APPLICATIONS

- FIGURE 23 ELECTRIC PASSENGER CAR SALES, BY COUNTRY/REGION, 2019-2024

- FIGURE 24 PHEV SALES, BY COUNTRY/REGION, 2019-2024

- FIGURE 25 EV THERMAL MANAGEMENT FLUID TRANSFER SOLUTION

- FIGURE 26 ELECTRIC BUS SALES, BY COUNTRY/REGION, 2023-2024

- FIGURE 27 PROJECTED DECLINE IN AUTOMOTIVE OUTPUT FROM 25% US TARIFFS ON VEHICLE IMPORTS, BY COUNTRY

- FIGURE 28 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 29 AVERAGE SELLING PRICE TREND, BY VEHICLE TYPE, 2022-2024 (USD)

- FIGURE 30 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2024 (USD)

- FIGURE 31 ECOSYSTEM ANALYSIS

- FIGURE 32 VALUE CHAIN ANALYSIS

- FIGURE 33 PATENT ANALYSIS

- FIGURE 34 MULTI-LAYER HOSE AND TUBE TECHNOLOGY

- FIGURE 35 COMPARISON OF THERMOPLASTIC MATERIALS

- FIGURE 36 COOLING WATER HOSE LINES FOR EV THERMAL MANAGEMENT

- FIGURE 37 IMPORT DATA FOR HS CODE 4009-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 38 EXPORT DATA FOR HS CODE 4009-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- FIGURE 39 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE

- FIGURE 40 KEY BUYING CRITERIA, BY VEHICLE TYPE

- FIGURE 41 IMPACT OF ELECTRIFICATION ON FLUID TRANSFER SYSTEMS

- FIGURE 42 FLUID TRANSFER SYSTEM MARKET, BY PROPULSION, 2025 VS. 2032 (USD MILLION)

- FIGURE 43 FLUID TRANSFER SYSTEM MARKET, BY VEHICLE TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 44 FLUID TRANSFER SYSTEM MARKET, BY SYSTEM TYPE, 2025 VS. 2032 (USD MILLION)

- FIGURE 45 FLUID TRANSFER SYSTEM MARKET, BY REGION, 2025 VS. 2032 (USD MILLION)

- FIGURE 46 ASIA PACIFIC: FLUID TRANSFER SYSTEM MARKET SNAPSHOT

- FIGURE 47 ASIA PACIFIC: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 48 ASIA PACIFIC: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 49 ASIA PACIFIC: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 50 ASIA PACIFIC: MANUFACTURING INDUSTRY CONTRIBUTION TO GDP, BY COUNTRY, 2024

- FIGURE 51 INDIA: FLUID TRANSFER SYSTEM KIT SIZE, BY PASSENGER CAR OEM

- FIGURE 52 SOUTHEAST ASIA: FLUID TRANSFER SYSTEM MARKET, BY COUNTRY, 2025 VS. 2032 (USD MILLION)

- FIGURE 53 SOUTHEAST ASIA: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 54 SOUTHEAST ASIA: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 55 SOUTHEAST ASIA: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 56 SOUTHEAST ASIA: MANUFACTURING INDUSTRY CONTRIBUTION TO GDP, BY COUNTRY, 2024

- FIGURE 57 NORTH AMERICA: FLUID TRANSFER SYSTEM MARKET SNAPSHOT

- FIGURE 58 NORTH AMERICA: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 59 NORTH AMERICA: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 60 NORTH AMERICA: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 61 NORTH AMERICA: MANUFACTURING INDUSTRY CONTRIBUTION TO GDP, BY COUNTRY, 2024

- FIGURE 62 EUROPE: FLUID TRANSFER SYSTEM MARKET SNAPSHOT

- FIGURE 63 EUROPE: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 64 EUROPE: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 65 EUROPE: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 66 EUROPE: MANUFACTURING INDUSTRY CONTRIBUTION TO GDP, BY COUNTRY, 2024

- FIGURE 67 REST OF THE WORLD: FLUID TRANSFER SYSTEM MARKET SNAPSHOT

- FIGURE 68 REST OF THE WORLD: REAL GDP GROWTH RATE, BY COUNTRY, 2024-2026

- FIGURE 69 REST OF THE WORLD: GDP PER CAPITA, BY COUNTRY, 2024-2026

- FIGURE 70 REST OF THE WORLD: INFLATION RATE AVERAGE CONSUMER PRICES, BY COUNTRY, 2024-2026

- FIGURE 71 REST OF THE WORLD: MANUFACTURING INDUSTRY CONTRIBUTION TO GDP, BY COUNTRY, 2024

- FIGURE 72 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

- FIGURE 73 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2024 (USD BILLION)

- FIGURE 74 COMPANY VALUATION (USD BILLION)

- FIGURE 75 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 76 BRAND/PRODUCT COMPARISON

- FIGURE 77 COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 78 COMPANY FOOTPRINT

- FIGURE 79 COMPANY EVALUATION MATRIX (START-UPS/SMES), 2024

- FIGURE 80 COOPER STANDARD: COMPANY SNAPSHOT

- FIGURE 81 TI FLUID SYSTEMS: COMPANY SNAPSHOT

- FIGURE 82 SUMITOMO RIKO COMPANY LIMITED: COMPANY SNAPSHOT

- FIGURE 83 PARKER HANNIFIN CORP: COMPANY SNAPSHOT

- FIGURE 84 GATES CORPORATION: COMPANY SNAPSHOT

- FIGURE 85 SANOH INDUSTRIAL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 86 CONTINENTAL AG: COMPANY SNAPSHOT

- FIGURE 87 DENSO CORPORATION: COMPANY SNAPSHOT

- FIGURE 88 NICHIRIN: COMPANY SNAPSHOT

- FIGURE 89 KONGSBERG AUTOMOTIVE: COMPANY SNAPSHOT

- FIGURE 90 AKWEL: COMPANY SNAPSHOT

- FIGURE 91 ROBERT BOSCH GMBH: COMPANY SNAPSHOT