PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1812621

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1812621

Digital Health Market by Offering (Hardware, Apps (Telehealth, DTx, Patient Portals, Pharmacy)), Disease, Use Case, End User, and Region - Global Forecast to 2030

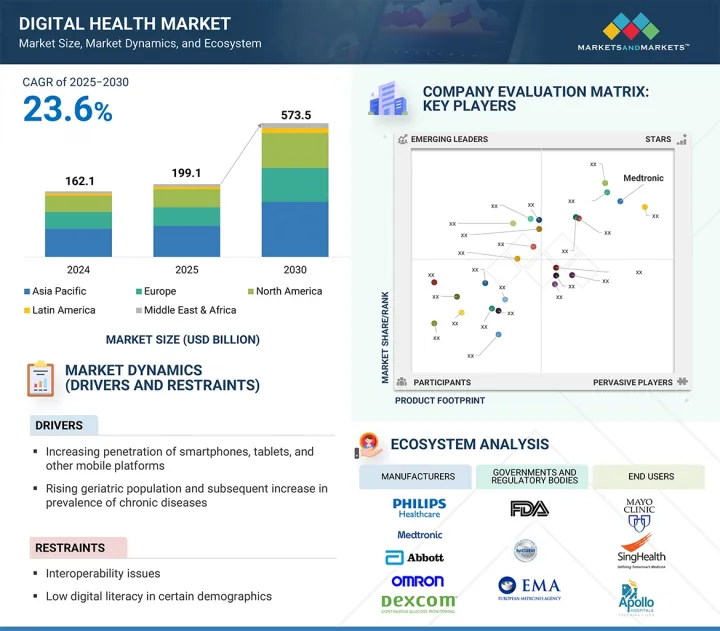

The global digital health market is projected to reach USD 573.5 billion by 2030 from USD 199.1 billion in 2025, at a high CAGR of 23.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Offering, disease, use case, and end user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The market is advancing steadily, propelled by the increasing demand for value-based care, the rising burden of chronic diseases, and a growing emphasis on preventive healthcare. With aging populations and escalating healthcare costs, providers and payers are turning to digital tools to improve care outcomes while optimizing resource utilization.

Solutions such as remote patient monitoring, digital therapeutics, and mobile health apps are playing a critical role in enabling continuous, at-home care, especially for chronic conditions like diabetes, hypertension, and heart disease. The market is further supported by expanding insurance coverage for digital interventions, strong consumer interest in health tracking, and innovation from both medtech and big tech players. Despite this momentum, the sector faces persistent challenges, chief among them are concerns over data security and privacy, regulatory uncertainty for emerging digital therapeutics, and the digital divide that limits access for elderly and low-income populations. These barriers must be addressed to fully realize the potential of digital health in delivering scalable, equitable, and high-quality care.

"Mental & behavioral health under the disease segment is expected to register the fastest growth during the forecast period."

In 2024, mental & behavioral health emerged as the fastest-growing segment of the digital health market. This is due to the rising awareness of mental well-being, increasing prevalence of stress, anxiety, and depression, and the reduced stigma around seeking help. The expansion of telepsychiatry, therapy apps, and AI-driven mental health platforms provides accessible, affordable, and confidential support, while integration with wearable devices and remote monitoring allows real-time tracking of behavioral patterns. These factors, combined with employer wellness programs and supportive healthcare policies, are driving rapid adoption and market expansion in this segment.

"The patients & consumers segment is projected to dominate the digital health market, by end user, during the forecast period."

In 2024, patients & consumers was the fastest-growing end-user segment in the digital health market. This is because of increasing health awareness, rising smartphone and wearable adoption, and the demand for personalized, on-demand healthcare solutions. Digital health apps, telemedicine platforms, and remote monitoring tools empower individuals to actively manage their health, access care anytime, and track vital signs or lifestyle metrics in real time. The shift toward preventive care, convenience-focused healthcare delivery, and self-management of chronic conditions has made patients and consumers the most dynamic growth driver in the market.

"Asia Pacific to witness the highest growth rate during the forecast period."

The Asia Pacific region is expected to register the fastest growth in the digital health market over the forecast period. Government initiatives promoting telemedicine, electronic health records, and AI-driven healthcare, combined with rising healthcare investments and expanding private sector participation, are accelerating adoption. Companies such as Halodoc (Indonesia) raised USD 100 million (in 2023), bringing its total to USD 258 million, with over 20 million monthly users on its platform. Government-led initiatives such as India's Ayushman Bharat Digital Mission (ABDM) is building a national digital health infrastructure, spanning EHRs, citizen health IDs, and analytics. In addition, strong private sector participation, increasing venture capital investments, and strategic partnerships between technology companies and healthcare providers are fueling innovation.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the authentication and brand protection marketplace. The break-down of primary interviews is as mentioned below:

- By Company Type - Tier 1: 31%, Tier 2: 28%, and Tier 3: 41%

- By Designation - C-level: 31%, Director-level: 25%, and Others: 44%

- By Region - North America: 32%, Europe: 32%, Asia Pacific: 26%, Middle East & Africa: 5%, Latin America: 5%

Key Players in the Digital Health Market

The key players operating in the digital health market include Medtronic (Ireland), Abbott (US), OMRON Healthcare, Inc. (Japan), Koninklijke Philips N.V. (Netherlands), Apple Inc. (US), Fitbit (US), Dexcom, Inc. (US), Boston Scientific Corporation (US), Masimo (US), Teladoc Health, Inc. (US), American Well (US), Hims & Hers Health, Inc. (US), Headspace (US), Noom, Inc. (US), Cerebral Inc. (US), Epic System Corporation (US), Omada Health Inc. (US), ORACLE (US), Click Therapeutics (US), Welldoc, Inc. (US), EverlyWell (US), TruDoc Healthcare LLC (UAE), CareSimple Inc. (US), VivaLNK, Inc. (US), Biobeat (Israel), and Virtual Therapeutics Corp. (US).

Research Coverage:

The report analyzes the digital health market and aims to estimate the market size and future growth potential of various market segments, based on offering, disease, use case, end user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers (Increasing penetration of smartphones, tablets, and other mobile platforms, Rising geriatric population and subsequent increase in prevalence of chronic diseases, Rising focus on patient-centric healthcare solutions, Increase in the use of wearables, Advancements in Al, Sensors & Connectivity (5G and 6G), Growth of Al-Powered Virtual Assistants and Chatbots), restraints (Interoperability issues, Low Digital Literacy in Certain Demographics), opportunities (Shift toward intelligent health ecosystem to deliver personalized health experiences, Increasing shift towards outpatient care model, Improving regulatory support and reimbursements, Advancements in digital health), and challenges (Clinical Validation & Long-Term Efficacy, Data Privacy and security concerns) influencing the growth of the digital health market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the digital health market

- Market Development: Comprehensive information on the lucrative emerging markets, components, deployments, technologies, applications, end users, and regions

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the digital health market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players, like Medtronic (Ireland), Abbott (US), OMRON Healthcare, Inc. (Japan), Koninklijke Philips N.V. (Netherlands), and Apple Inc. (US), in the digital health market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary interviews

- 2.1.2.2 Insights from primary experts

- 2.1.2.3 Breakdown of primary sources

- 2.1.1 SECONDARY DATA

- 2.2 RESEARCH METHODOLOGY

- 2.3 MARKET SIZE ESTIMATION

- 2.4 DATA TRIANGULATION

- 2.5 MARKET RANKING ANALYSIS

- 2.6 RISK ASSESSMENT

- 2.7 STUDY ASSUMPTIONS

- 2.8 LIMITATIONS

- 2.8.1 METHODOLOGY-RELATED LIMITATIONS

- 2.8.2 SCOPE-RELATED LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 DIGITAL HEALTH MARKET OVERVIEW

- 4.2 NORTH AMERICA: DIGITAL HEALTH MARKET, BY END USER AND COUNTRY

- 4.3 DIGITAL HEALTH MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 DIGITAL HEALTH MARKET: REGIONAL MIX

- 4.5 DIGITAL HEALTH MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing penetration of smartphones, tablets, and other mobile platforms

- 5.2.1.2 Rising geriatric population and subsequent increase in prevalence of chronic diseases

- 5.2.1.3 Rising focus on patient-centric healthcare solutions

- 5.2.1.4 Rising use of wearables

- 5.2.1.5 Advancements in AI, sensors, and connectivity (5G and 6G)

- 5.2.1.6 Growth of AI-powered virtual assistants and chatbots

- 5.2.2 RESTRAINTS

- 5.2.2.1 Low digital literacy in certain demographics

- 5.2.2.2 Interoperability issues

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Shift toward intelligent health ecosystem to deliver personalized health experiences

- 5.2.3.2 Increasing shift towards outpatient care

- 5.2.3.3 Improving regulatory support and reimbursements

- 5.2.3.4 Advancements in digital health

- 5.2.4 CHALLENGES

- 5.2.4.1 Healthcare gap in emerging economies

- 5.2.4.2 Privacy and security concerns

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 INDUSTRY TRENDS

- 5.4.1 EMERGENCE OF VALUE-BASED STRATEGY FOR CONTINUOUS CARE

- 5.4.2 HOME: NEW HEALTHCARE HUB

- 5.4.3 TECHNOLOGICALLY ENABLED PRIMARY CARE SERVICES

- 5.4.4 RISING AWARENESS OF DIGITAL THERAPEUTICS TO TREAT HUMAN DISEASES

- 5.4.5 SURGE IN MHEALTH APPS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 mHealth apps

- 5.7.1.2 Wearable sensors & devices

- 5.7.1.3 Remote patient monitoring

- 5.7.1.4 Digital therapeutics

- 5.7.1.5 Telehealth/virtual care platforms

- 5.7.1.6 AI-powered tools

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Cloud computing & edge processing

- 5.7.2.2 Data analytics & visualization

- 5.7.2.3 Bluetooth & IoT connectivity

- 5.7.2.4 EHR integration

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Digital twins

- 5.7.3.2 AR/VR & extended reality (XR)

- 5.7.3.3 Voice assistants/smart speakers

- 5.7.1 KEY TECHNOLOGIES

- 5.8 TARIFF AND REGULATORY ANALYSIS

- 5.8.1 TARIFF DATA FOR HS CODE 9018

- 5.8.2 TARIFF DATA FOR HS CODE 9021

- 5.8.3 TARIFF DATA FOR HS CODE 8517

- 5.8.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8.5 REGULATORY FRAMEWORK

- 5.9 PRICING ANALYSIS

- 5.9.1 INDICATIVE PRICE, BY OFFERING

- 5.9.2 INDICATIVE PRICE, BY REGION

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.10.2 BARGAINING POWER OF BUYERS

- 5.10.3 THREAT OF SUBSTITUTES

- 5.10.4 THREAT OF NEW ENTRANTS

- 5.10.5 BARGAINING POWER OF SUPPLIERS

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.11.2 BUYING CRITERIA

- 5.12 PATENT ANALYSIS

- 5.12.1 PATENT PUBLICATION TRENDS FOR DIGITAL HEALTH MARKET

- 5.12.2 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR DIGITAL HEALTH

- 5.12.3 MAJOR PATENTS IN DIGITAL HEALTH MARKET

- 5.13 UNMET NEEDS AND END-USER EXPECTATIONS

- 5.13.1 UNMET NEEDS IN DIGITAL HEALTH MARKET

- 5.13.2 END-USER EXPECTATIONS

- 5.14 KEY CONFERENCES AND EVENTS

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 CASE STUDY 1: CLINICAS DEL AZUCAR (CDA)

- 5.15.2 CASE STUDY 2: NOVA HOSPITAL & ENOVACOM

- 5.15.3 CASE STUDY 3: APPLE & NHS TEAMS

- 5.16 DIGITAL HEALTH MARKET: INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- 5.17 TRADE ANALYSIS

- 5.17.1 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 8518)

- 5.17.2 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9021)

- 5.17.3 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9022)

- 5.17.4 TRADE ANALYSIS FOR DIGITAL HEALTH DEVICES (HSN CODE 9018)

- 5.18 DIGITAL HEALTH MARKET BUSINESS MODELS

- 5.18.1 SUBSCRIPTION-BASED MODELS

- 5.18.2 SOFTWARE AS A SERVICE (SAAS)/PLATFORM AS A SERVICE (PAAS)

- 5.18.3 FREEMIUM MODELS WITH TIERED ACCESS

- 5.18.4 OUTCOMES-BASED AND VALUE-BASED MODELS

- 5.19 IMPACT OF AI/GEN AI IN DIGITAL HEALTH MARKET

- 5.19.1 KEY USE CASES

- 5.19.2 CASE STUDIES OF AI/GENERATIVE AI IMPLEMENTATION

- 5.19.2.1 Artificial intelligence in public health

- 5.19.2.2 Artificial intelligence in digital health-issues and dimensions of ethical concerns

- 5.19.3 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 5.19.3.1 Telehealth and telemedicine

- 5.19.3.2 Wearable devices

- 5.19.3.3 Remote patient monitoring (RPM)

- 5.19.3.4 Mobile health (mHealth)

- 5.19.4 USER READINESS & IMPACT ASSESSMENT

- 5.19.4.1 User readiness

- 5.19.4.1.1 User A: Healthcare providers

- 5.19.4.1.2 User B: Healthcare payers

- 5.19.4.1.3 User C: Patients & consumers

- 5.19.4.1.4 User D: Pharmaceutical, biotech, and MedTech companies (including CROs)

- 5.19.4.1.5 User E: Other end users (academic institutes, research centers, government bodies)

- 5.19.4.2 Impact assessment

- 5.19.4.2.1 User A: Healthcare providers

- 5.19.4.2.1.1 Implementation

- 5.19.4.2.1.2 Impact

- 5.19.4.2.2 User B: Healthcare payers

- 5.19.4.2.2.1 Implementation

- 5.19.4.2.2.2 Impact

- 5.19.4.2.3 User C: Patients & consumers

- 5.19.4.2.3.1 Implementation

- 5.19.4.2.3.2 Impact

- 5.19.4.2.4 User D: Pharmaceutical, biotech, and MedTech companies (including CROs)

- 5.19.4.2.4.1 Implementation

- 5.19.4.2.4.2 Impact

- 5.19.4.2.5 User E: Other end users (academic institutes, research centers, government bodies)

- 5.19.4.2.5.1 Implementation

- 5.19.4.2.5.2 Impact

- 5.19.4.2.1 User A: Healthcare providers

- 5.19.4.1 User readiness

- 5.20 IMPACT OF 2025 US TARIFFS-DIGITAL HEALTH MARKET

- 5.20.1 INTRODUCTION

- 5.20.2 KEY TARIFF RATES

- 5.20.3 PRICE IMPACT ANALYSIS

- 5.20.4 IMPACT ON COUNTRIES/REGIONS

- 5.20.4.1 US

- 5.20.5 EUROPE

- 5.20.6 ASIA PACIFIC

- 5.20.7 IMPACT ON END-USE INDUSTRIES

- 5.20.7.1 Healthcare providers

- 5.20.7.2 Healthcare payers

- 5.20.7.3 Patients and consumers

- 5.20.7.4 Pharmaceutical, biotechnology, and MedTech companies

- 5.20.7.5 Other end users

- 5.21 REIMBURSEMENT ANALYSIS

- 5.22 RISK FACTORS AND MARKET ENTRY BARRIERS

- 5.23 FUTURE OUTLOOK AND DISRUPTION SCENARIOS

6 DIGITAL HEALTH MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.2 HARDWARE

- 6.2.1 SMART HARDWARE SOLUTIONS VITAL IN POWERING DIGITAL HEALTH

- 6.2.2 WEARABLES

- 6.2.2.1 Wearables to empower patients with real-time health monitoring

- 6.2.3 CONSUMER-GRADED WEARABLE HEALTHCARE DEVICES

- 6.2.3.1 Wearable healthcare devices to empower consumers to be proactive about their well-being

- 6.2.4 CLINICAL-GRADE WEARABLE HEALTHCARE DEVICES

- 6.2.4.1 Clinical-grade devices to allow remote care with continuous monitoring

- 6.2.5 IMPLANTABLE DEVICES

- 6.2.5.1 Real-time data transmission to healthcare providers for proactive intervention and personalized care

- 6.2.6 HANDHELD & PORTABLE DEVICES

- 6.2.6.1 Compact design and integration with mobile health applications to make them highly effective for use in remote care

- 6.2.7 STATIONARY DEVICES

- 6.2.7.1 Stationary devices to be upgraded with IoT integration, AI-driven analytics, and cloud-enabled interoperability

- 6.3 SOLUTIONS/APPLICATIONS

- 6.3.1 TELEHEALTHCARE/TELEMEDICINE

- 6.3.1.1 Demand to advance connected care via virtual health platforms

- 6.3.2 REMOTE PATIENT MONITORING

- 6.3.2.1 Expected to be more seamlessly integrated with telemedicine platforms, expanding their capabilities

- 6.3.3 VIRTUAL CARE & VIDEO CONSULTATION

- 6.3.3.1 Offering enhanced efficiency, accessibility, and accuracy in remote healthcare, assisting in triaging patients and automating documentation

- 6.3.4 VIRTUAL SITTING & NURSING PLATFORMS

- 6.3.4.1 Offering remote patient monitoring with bidirectional communication

- 6.3.1 TELEHEALTHCARE/TELEMEDICINE

- 6.4 MHEALTH APPS

- 6.4.1 TRANSFORMING CARE DELIVERY WITH MOBILE HEALTH SOLUTIONS

- 6.5 DIGITAL THERAPEUTICS

- 6.5.1 EMPOWERING HEALTH BY COMBINING REAL-TIME DATA COLLECTION, PATIENT ENGAGEMENT TOOLS, AND INTEGRATION WITH HEALTHCARE PROVIDERS' SYSTEMS

- 6.6 DIGITAL PHARMACY & MEDICATION ACCESS

- 6.6.1 ENHANCING MEDICATION ACCESS BY REACHING RURAL OR UNDERSERVED POPULATIONS, REDUCING TRAVEL AND WAIT TIMES, AND IMPROVING CONTINUITY OF CARE

- 6.7 DIGITAL DIAGNOSTICS & AT-HOME TESTING

- 6.7.1 MOSTLY USED IN GLUCOSE MONITORING AND OTHER INFECTIOUS DISEASE TESTS, CHOLESTEROL AND LIPID PANELS, GENETIC TESTING, AND HORMONE OR FERTILITY ASSESSMENTS

- 6.8 PATIENT PORTALS

- 6.8.1 PERSONALIZED HEALTH CONTENT, APPOINTMENT REMINDERS, AND SECURE MESSAGING AIM TO IMPROVE PATIENT ENGAGEMENT AND CARE COORDINATION

- 6.9 OTHER DIGITAL HEALTH SOLUTIONS/APPLICATIONS

7 DIGITAL HEALTH MARKET, BY DISEASE

- 7.1 INTRODUCTION

- 7.2 DIABETES

- 7.2.1 INTEGRATING AI IN DIGITAL HEALTH TO CATER TO DIABETIC PATIENTS

- 7.3 CARDIOLOGY

- 7.3.1 OFFERING EARLIER DETECTION, CONTINUOUS MONITORING, AND PERSONALIZED MANAGEMENT OF CARDIOVASCULAR CONDITIONS

- 7.4 MENTAL HEALTH & BEHAVIORAL HEALTH

- 7.4.1 IMPROVING ACCESSIBILITY TO MENTAL HEALTH SERVICES, ESPECIALLY IN UNDERSERVED REGIONS

- 7.5 RESPIRATORY DISORDERS

- 7.5.1 ENABLING REAL-TIME MONITORING OF LUNG FUNCTION, MEDICATION ADHERENCE, AND OXYGEN LEVELS

- 7.6 LIFESTYLE & WELLNESS IMPROVEMENT

- 7.6.1 EXPANDING ACCESS AND PERSONALIZING CARE IN MENTAL & BEHAVIORAL HEALTH THROUGH DIGITAL HEALTH

- 7.7 NEUROLOGY

- 7.7.1 ADVANCING NEUROLOGICAL CARE WITH DIGITAL HEALTH INNOVATIONS

- 7.8 MUSCULOSKELETAL DISORDERS/PAIN MANAGEMENT

- 7.8.1 ACCELERATING INNOVATION IN HANDHELD & PORTABLE DEVICES TO BOOST MARKET GROWTH

- 7.9 ONCOLOGY

- 7.9.1 ADOPTION OF AI IN REMOTE PATIENT MONITORING (RPM) TO LEAD TO ITS EMERGING AS PROMISING SOLUTION TO SUPPORT PERSONALIZED CARE

- 7.10 WOMEN'S HEALTH & REPRODUCTIVE HEALTH

- 7.10.1 ENHANCING PREVENTIVE CARE, EMPOWERING WOMEN WITH SELF-MANAGEMENT TOOLS, AND STRENGTHENING OUTCOMES IN REPRODUCTIVE AND MATERNAL HEALTH

- 7.11 OTHER DISEASES

8 DIGITAL HEALTH MARKET, BY USE CASE

- 8.1 INTRODUCTION

- 8.2 PREVENTIVE CARE & WELLNESS

- 8.2.1 DRIVING PROACTIVE HEALTH MANAGEMENT THROUGH DIGITAL INNOVATION

- 8.3 DIAGNOSIS

- 8.3.1 ADVANCING DIAGNOSIS THROUGH AI-POWERED SYMPTOM CHECKING AND EARLY DETECTION

- 8.4 TREATMENT

- 8.4.1 FEEDING REAL-TIME DATA TO HEALTHCARE PROVIDERS, ALLOWING TREATMENT ADJUSTMENTS AND PROACTIVE INTERVENTIONS

- 8.5 PATIENT MONITORING

- 8.5.1 SHIFT TOWARD PERSONALIZED, SCALABLE, AND PREVENTIVE CARE

- 8.6 REHABILITATION & RECOVERY

- 8.6.1 PARTICULARLY IMPACTFUL IN POST-SURGICAL CARE, NEUROLOGICAL REHABILITATION, STROKE RECOVERY, AND MUSCULOSKELETAL THERAPY

- 8.7 OTHER USE CASES

9 DIGITAL HEALTH MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.2.1.1 Rise in demand for high-quality care and government support to encourage digital health adoption in hospitals

- 9.2.2 CLINICS & OTHER OUTPATIENT SETTINGS

- 9.2.2.1 Increase in demand for cost-effective care and postoperative monitoring to drive digital health adoption in outpatient settings

- 9.2.3 OTHER HEALTHCARE PROVIDERS

- 9.2.1 HOSPITALS

- 9.3 HEALTHCARE PAYERS

- 9.3.1 PUBLIC PAYERS

- 9.3.1.1 Driving population health and value-based care through digital innovation

- 9.3.2 PRIVATE PAYERS

- 9.3.2.1 Personalized benefit designs, value-based provider contracting, and delivering consumer-centric experiences

- 9.3.1 PUBLIC PAYERS

- 9.4 PATIENTS & CONSUMERS

- 9.4.1 AI AND WEARABLE DEVICES TO DRIVE GROWTH IN DIGITAL HEALTH FOR PERSONALIZED CARE AND ACCESSIBILITY

- 9.5 PHARMACEUTICAL, BIOTECHNOLOGY, AND MEDTECH COMPANIES

- 9.5.1 PHARMACEUTICAL AND BIOTECH ADOPTION OF DIGITAL HEALTH TO ENHANCE DRUG DEVELOPMENT, PATIENT ENGAGEMENT, AND ADHERENCE

- 9.6 OTHER END USERS

10 DIGITAL HEALTH MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 10.2.2 US

- 10.2.2.1 Integration of AI, data interoperability, and virtual-first care models to drive market

- 10.2.3 CANADA

- 10.2.3.1 Advancing health equity and access through digital infrastructure

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 10.3.2 GERMANY

- 10.3.2.1 Innovation-focused policy framework and digital infrastructure expansion to support growth

- 10.3.3 UK

- 10.3.3.1 Increase in prevalence of chronic and lifestyle-related diseases and high penetration of wearables to drive market

- 10.3.4 FRANCE

- 10.3.4.1 Government support for e-Health to propel market

- 10.3.5 ITALY

- 10.3.5.1 Digital transformation and integrated care to support market growth

- 10.3.6 SPAIN

- 10.3.6.1 Health system modernization and data-driven care to enable digital health growth in Spain

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 10.4.2 CHINA

- 10.4.2.1 High burden of chronic diseases to fuel market growth

- 10.4.3 JAPAN

- 10.4.3.1 Large geriatric population and strong push toward modernization to propel market

- 10.4.4 INDIA

- 10.4.4.1 Growing adoption of telemedicine and mounting pressure to reduce healthcare expenditure to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Telehealth and digital integration to drive growth in Australia's digital health market

- 10.4.6 SOUTH KOREA

- 10.4.6.1 AI, data ecosystems, and cross-sector synergy to power South Korea's digital health growth

- 10.4.7 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 10.5.2 BRAZIL

- 10.5.2.1 Government digitalization push and interoperability frameworks to catalyze market expansion

- 10.5.3 MEXICO

- 10.5.3.1 Government reforms, infrastructural expansion, and chronic disease burden to drive market

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 10.6.2 GCC

- 10.6.2.1 AI leadership, virtual infrastructure, and policy alignment to power digital health growth in GCC

- 10.6.2.2 Saudi Arabia

- 10.6.2.2.1 Rapid digital health transformation to propel market in Saudi Arabia

- 10.6.2.3 UAE

- 10.6.2.3.1 UAE emerges as regional pioneer in digital healthcare innovation

- 10.6.2.4 Rest of GCC

- 10.6.3 SOUTH AFRICA

- 10.6.3.1 Infrastructure expansion, youthful demographics, and innovation ecosystems to accelerate digital health growth

- 10.6.4 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL HEALTH MARKET

- 11.3 REVENUE SHARE ANALYSIS OF TOP MARKET PLAYERS

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 BRAND/SOFTWARE COMPARISON

- 11.6 COMPANY VALUATION & FINANCIAL METRICS

- 11.6.1 FINANCIAL METRICS

- 11.6.2 COMPANY VALUATION

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT

- 11.7.6 REGION FOOTPRINT

- 11.7.7 OFFERING FOOTPRINT

- 11.7.8 DISEASE FOOTPRINT

- 11.7.9 USE CASE FOOTPRINT

- 11.7.10 END USER FOOTPRINT

- 11.8 STARTUP/SME EVALUATION MATRIX, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 DYNAMIC COMPANIES

- 11.8.3 RESPONSIVE COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of startups/SMEs

- 11.9 COMPETITIVE SCENARIO AND TRENDS

- 11.9.1 PRODUCT LAUNCHES & APPROVALS

- 11.9.2 DEALS

- 11.9.3 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 MEDTRONIC

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches & approvals

- 12.1.1.3.2 Deals

- 12.1.1.3.3 Other developments

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 ABBOTT

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches & approvals

- 12.1.2.3.2 Deals

- 12.1.2.4 MnM view

- 12.1.2.4.1 Key strengths

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 DEXCOM, INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches & approvals

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 KONINKLIJKE PHILIPS N.V.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches & approvals

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansions

- 12.1.4.4 MnM view

- 12.1.4.4.1 Key strengths

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 FITBIT, INC. (GOOGLE)

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches & approvals

- 12.1.5.3.2 Deals

- 12.1.5.4 MnM view

- 12.1.5.4.1 Key strengths

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 OMRON HEALTHCARE, INC.

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches & approvals

- 12.1.6.3.2 Deals

- 12.1.7 APPLE, INC.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches & approvals

- 12.1.7.3.2 Deals

- 12.1.8 BOSTON SCIENTIFIC CORPORATION

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches & approvals

- 12.1.8.3.2 Deals

- 12.1.9 MASIMO

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Product launches & approvals

- 12.1.9.3.2 Deals

- 12.1.10 TELADOC HEALTH, INC.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Product launches & approvals

- 12.1.10.3.2 Deals

- 12.1.11 AMERICAN WELL

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Product launches & approvals

- 12.1.11.3.2 Deals

- 12.1.11.3.3 Other developments

- 12.1.12 HIMS & HERS HEALTH, INC.

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Product launches & approvals

- 12.1.12.3.2 Deals

- 12.1.13 HEADSPACE

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches & approvals

- 12.1.13.3.2 Deals

- 12.1.14 NOOM, INC.

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product launches & approvals

- 12.1.14.3.2 Deals

- 12.1.15 CEREBRAL INC.

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.15.3 Recent developments

- 12.1.15.3.1 Product launches & approvals

- 12.1.15.3.2 Deals

- 12.1.16 EPIC SYSTEMS CORPORATION

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Product launches & approvals

- 12.1.16.3.2 Deals

- 12.1.17 OMADA HEALTH INC.

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Product launches & approvals

- 12.1.17.3.2 Deals

- 12.1.18 ORACLE

- 12.1.18.1 Business overview

- 12.1.18.2 Products offered

- 12.1.18.3 Recent developments

- 12.1.18.3.1 Product launches & approvals

- 12.1.18.3.2 Deals

- 12.1.19 CLICK THERAPEUTICS, INC.

- 12.1.19.1 Business overview

- 12.1.19.2 Products offered

- 12.1.19.3 Recent developments

- 12.1.19.3.1 Product launches & approvals

- 12.1.19.3.2 Deals

- 12.1.20 WELLDOC, INC.

- 12.1.20.1 Business overview

- 12.1.20.2 Products offered

- 12.1.20.3 Recent developments

- 12.1.20.3.1 Product launches & approvals

- 12.1.20.3.2 Deals

- 12.1.21 EVERLYWELL

- 12.1.21.1 Business overview

- 12.1.21.2 Products offered

- 12.1.21.3 Recent developments

- 12.1.21.3.1 Product launches & approvals

- 12.1.21.3.2 Deals

- 12.1.1 MEDTRONIC

- 12.2 OTHER PLAYERS

- 12.2.1 TRUDOC HEALTHCARE LLC

- 12.2.2 CARESIMPLE INC.

- 12.2.3 VIVALNK, INC.

- 12.2.4 BIOBEAT

- 12.2.5 VIRTUAL THERAPEUTICS CORP.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 FACTOR ANALYSIS

- TABLE 2 LARGEST HEALTHCARE DATA BREACHES (2021-2025)

- TABLE 3 AVERAGE TARIFFS UNDER HS CODE 9018

- TABLE 4 AVERAGE TARIFFS UNDER HS CODE 9021

- TABLE 5 AVERAGE TARIFFS UNDER HS CODE 8517

- TABLE 6 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 DIGITAL HEALTH MARKET: REGULATORY STANDARDS

- TABLE 11 REGULATORY REQUIREMENTS IN NORTH AMERICA

- TABLE 12 REGULATORY REQUIREMENTS IN EUROPE

- TABLE 13 REGULATORY REQUIREMENTS IN ASIA PACIFIC

- TABLE 14 REGULATORY REQUIREMENTS IN LATIN AMERICA

- TABLE 15 REGULATORY REQUIREMENTS IN MIDDLE EAST & AFRICA

- TABLE 16 INDICATIVE PRICE OF DIGITAL HEALTH SOLUTIONS, BY OFFERING, 2024

- TABLE 17 INDICATIVE PRICE OF DIGITAL HEALTH SOLUTIONS, BY REGION, 2024

- TABLE 18 DIGITAL HEALTH MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 20 KEY BUYING CRITERIA FOR DIGITAL HEALTH MARKET OFFERINGS

- TABLE 21 UNMET NEEDS IN DIGITAL HEALTH MARKET

- TABLE 22 END-USER EXPECTATIONS IN DIGITAL HEALTH MARKET

- TABLE 23 DIGITAL HEALTH MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- TABLE 24 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 25 DIGITAL HEALTH MARKET: CPT CODES AND REIMBURSEMENT ANALYSIS

- TABLE 26 DIGITAL HEALTH MARKET: RISK FACTORS AND MARKET ENTRY BARRIERS

- TABLE 27 DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 28 DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 29 DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 30 DIGITAL HEALTH WEARABLES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 31 CONSUMER-GRADED WEARABLE HEALTHCARE DEVICES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 32 CLINICAL-GRADE WEARABLE HEALTHCARE DEVICES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 33 IMPLANTABLE DIGITAL HEALTH DEVICES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 34 HANDHELD & PORTABLE DIGITAL HEALTH DEVICES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 35 STATIONARY DIGITAL HEALTH DEVICES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 36 DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 37 DIGITAL HEALTH SERVICES SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 38 TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 39 COMPANIES OFFERING DIGITAL HEALTH SOLUTIONS FOR REMOTE PATIENT MONITORING

- TABLE 40 REMOTE PATIENT MONITORING SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 41 COMPANIES OFFERING DIGITAL HEALTH SOLUTIONS FOR VIRTUAL CARE

- TABLE 42 VIRTUAL CARE & VIDEO CONSULTATION SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 43 COMPANIES OFFERING VIRTUAL SITTING & NURSING PLATFORMS

- TABLE 44 VIRTUAL SITTING & NURSING PLATFORMS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 45 MHEALTH APPS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 DIGITAL THERAPEUTICS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 47 DIGITAL PHARMACY & MEDICATION ACCESS SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 48 DIGITAL DIAGNOSTICS & AT-HOME TESTING SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 49 PATIENT PORTAL SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 50 OTHER DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 51 DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 52 COMPANIES OFFERING DIGITAL HEALTH FOR DIABETES SOLUTIONS

- TABLE 53 DIGITAL HEALTH MARKET FOR DIABETES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 54 DIGITAL HEALTH MARKET FOR CARDIOLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 55 DIGITAL HEALTH MARKET FOR MENTAL HEALTH & BEHAVIORAL HEALTH, BY REGION, 2023-2030 (USD MILLION)

- TABLE 56 COMPANIES OFFERING DIGITAL HEALTH SOLUTIONS FOR RESPIRATORY DISORDERS

- TABLE 57 DIGITAL HEALTH MARKET FOR RESPIRATORY DISORDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 DIGITAL HEALTH MARKET FOR LIFESTYLE & WELLNESS IMPROVEMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 59 DIGITAL HEALTH MARKET FOR NEUROLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 60 DIGITAL HEALTH MARKET FOR MUSCULOSKELETAL DISORDERS/PAIN MANAGEMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 61 DIGITAL HEALTH MARKET FOR ONCOLOGY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 DIGITAL HEALTH MARKET FOR WOMEN'S HEALTH & REPRODUCTIVE HEALTH, BY REGION, 2023-2030 (USD MILLION)

- TABLE 63 DIGITAL HEALTH MARKET FOR OTHER DISEASES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 64 DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 65 DIGITAL HEALTH MARKET FOR PREVENTIVE CARE & WELLNESS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 66 DIGITAL HEALTH MARKET FOR DIAGNOSIS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 67 DIGITAL HEALTH MARKET FOR TREATMENT, BY REGION, 2023-2030 (USD MILLION)

- TABLE 68 DIGITAL HEALTH MARKET FOR PATIENT MONITORING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 69 DIGITAL HEALTH MARKET FOR REHABILITATION & RECOVERY, BY REGION, 2023-2030 (USD MILLION)

- TABLE 70 DIGITAL HEALTH MARKET FOR OTHER USE CASES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 71 DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 72 DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 73 DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 74 DIGITAL HEALTH MARKET FOR HOSPITALS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 75 DIGITAL HEALTH MARKET FOR CLINICS & OTHER OUTPATIENT SETTINGS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 76 DIGITAL HEALTH MARKET FOR OTHER HEALTHCARE PROVIDERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 77 DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 78 DIGITAL HEALTH MARKET FOR PUBLIC PAYERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 79 DIGITAL HEALTH MARKET FOR PRIVATE PAYERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 80 DIGITAL HEALTH MARKET FOR PATIENTS & CONSUMERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 81 DIGITAL HEALTH MARKET FOR PHARMACEUTICAL, BIOTECHNOLOGY, AND MEDTECH COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 82 DIGITAL HEALTH MARKET FOR OTHER END USERS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 83 DIGITAL HEALTH MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 84 NORTH AMERICA: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 85 NORTH AMERICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 87 NORTH AMERICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 88 NORTH AMERICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 90 NORTH AMERICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 91 NORTH AMERICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 93 NORTH AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 94 NORTH AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 95 US: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 96 US: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 97 US: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 98 US: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 99 US: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 100 US: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 101 US: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 102 US: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 103 US: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 104 US: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 105 CANADA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 106 CANADA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 107 CANADA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 108 CANADA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 109 CANADA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 110 CANADA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 111 CANADA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 112 CANADA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 113 CANADA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 114 CANADA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 115 EUROPE: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 116 EUROPE: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 117 EUROPE: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 118 EUROPE: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 119 EUROPE: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 120 EUROPE: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 121 EUROPE: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 122 EUROPE: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 123 EUROPE: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 124 EUROPE: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 125 EUROPE: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 126 GERMANY: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 127 GERMANY: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 128 GERMANY: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 129 GERMANY: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 130 GERMANY: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 131 GERMANY: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 132 GERMANY: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 133 GERMANY: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 134 GERMANY: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 135 GERMANY: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 136 UK: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 137 UK: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 138 UK: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 139 UK: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 140 UK: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 141 UK: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 142 UK: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 143 UK: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 144 UK: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 145 UK: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 146 FRANCE: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 147 FRANCE: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 148 FRANCE: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 149 FRANCE: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 150 FRANCE: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 151 FRANCE: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 152 FRANCE: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 153 FRANCE: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 154 FRANCE: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 155 FRANCE: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 156 ITALY: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 157 ITALY: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 158 ITALY: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 159 ITALY: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 160 ITALY: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 161 ITALY: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 162 ITALY: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 163 ITALY: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 164 ITALY: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 165 ITALY: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 166 SPAIN: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 167 SPAIN: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 168 SPAIN: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 169 SPAIN: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 170 SPAIN: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 171 SPAIN: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 172 SPAIN: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 173 SPAIN: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 174 SPAIN: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 175 SPAIN: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 176 REST OF EUROPE: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 177 REST OF EUROPE: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 178 REST OF EUROPE: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 179 REST OF EUROPE: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 180 REST OF EUROPE: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 181 REST OF EUROPE: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 182 REST OF EUROPE: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 183 REST OF EUROPE: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 184 REST OF EUROPE: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 185 REST OF EUROPE: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 186 ASIA PACIFIC: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 187 ASIA PACIFIC: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 188 ASIA PACIFIC: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 189 ASIA PACIFIC: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 190 ASIA PACIFIC: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 191 ASIA PACIFIC: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 192 ASIA PACIFIC: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 193 ASIA PACIFIC: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 194 ASIA PACIFIC: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 195 ASIA PACIFIC: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 196 ASIA PACIFIC: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 197 CHINA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 198 CHINA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 199 CHINA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 200 CHINA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 201 CHINA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 202 CHINA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 203 CHINA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 204 CHINA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 205 CHINA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 206 CHINA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 207 JAPAN: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 208 JAPAN: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 209 JAPAN: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 210 JAPAN: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 211 JAPAN: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 212 JAPAN: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 213 JAPAN: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 214 JAPAN: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 215 JAPAN: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 216 JAPAN: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 217 INDIA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 218 INDIA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 219 INDIA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 220 INDIA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 221 INDIA: TELEHEALTHCARE/ TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 222 INDIA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 223 INDIA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 224 INDIA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 225 INDIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 226 INDIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 227 AUSTRALIA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 228 AUSTRALIA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 229 AUSTRALIA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 230 AUSTRALIA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 231 AUSTRALIA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 232 AUSTRALIA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 233 AUSTRALIA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 234 AUSTRALIA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 235 AUSTRALIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 236 AUSTRALIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 237 SOUTH KOREA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 238 SOUTH KOREA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 239 SOUTH KOREA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 240 SOUTH KOREA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 241 SOUTH KOREA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 242 SOUTH KOREA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 243 SOUTH KOREA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 244 SOUTH KOREA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 245 SOUTH KOREA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 246 SOUTH KOREA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 247 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 248 REST OF ASIA PACIFIC: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 249 REST OF ASIA PACIFIC: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 250 REST OF ASIA PACIFIC: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 251 REST OF ASIA PACIFIC: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 252 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 253 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 254 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 255 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 256 REST OF ASIA PACIFIC: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 257 LATIN AMERICA: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 258 LATIN AMERICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 259 LATIN AMERICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 260 LATIN AMERICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 261 LATIN AMERICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 262 LATIN AMERICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 263 LATIN AMERICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 264 LATIN AMERICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 265 LATIN AMERICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 266 LATIN AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 267 LATIN AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 268 BRAZIL: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 269 BRAZIL: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 270 BRAZIL: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 271 BRAZIL: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 272 BRAZIL: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 273 BRAZIL: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 274 BRAZIL: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 275 BRAZIL: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 276 BRAZIL: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 277 BRAZIL: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 278 MEXICO: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 279 MEXICO: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 280 MEXICO: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 281 MEXICO: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 282 MEXICO: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 283 MEXICO: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 284 MEXICO: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 285 MEXICO: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 286 MEXICO: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 287 MEXICO: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 288 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 289 REST OF LATIN AMERICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 290 REST OF LATIN AMERICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 291 REST OF LATIN AMERICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 292 REST OF LATIN AMERICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 293 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 294 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 295 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 296 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 297 REST OF LATIN AMERICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 298 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 299 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 300 MIDDLE EAST & AFRICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 301 MIDDLE EAST & AFRICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 303 MIDDLE EAST & AFRICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 304 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 305 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 306 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 307 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 308 MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 309 GCC: DIGITAL HEALTH MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 310 GCC: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 311 GCC: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 312 GCC: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 313 GCC: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 314 GCC: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 315 GCC: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 316 GCC: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 317 GCC: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 318 GCC: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 319 GCC: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 320 SAUDI ARABIA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 321 SAUDI ARABIA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 322 SAUDI ARABIA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 323 SAUDI ARABIA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 324 SAUDI ARABIA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 325 SAUDI ARABIA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 326 SAUDI ARABIA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 327 SAUDI ARABIA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 328 SAUDI ARABIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 329 SAUDI ARABIA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 330 UAE: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 331 UAE: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 332 UAE: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 333 UAE: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 334 UAE: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 335 UAE: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 336 UAE: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 337 UAE: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 338 UAE: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 339 UAE: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 340 REST OF GCC: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 341 REST OF GCC: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 342 REST OF GCC: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 343 REST OF GCC: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 344 REST OF GCC: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 345 REST OF GCC: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 346 REST OF GCC: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 347 REST OF GCC: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 348 REST OF GCC: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 349 REST OF GCC: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 350 SOUTH AFRICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 351 SOUTH AFRICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 352 SOUTH AFRICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 353 SOUTH AFRICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 354 SOUTH AFRICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 355 SOUTH AFRICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 356 SOUTH AFRICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 357 SOUTH AFRICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 358 SOUTH AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 359 SOUTH AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 360 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 361 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH HARDWARE MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 362 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH WEARABLES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 363 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 364 REST OF MIDDLE EAST & AFRICA: TELEHEALTHCARE/TELEMEDICINE SOLUTIONS/APPLICATIONS MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 365 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY DISEASE, 2023-2030 (USD MILLION)

- TABLE 366 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY USE CASE, 2023-2030 (USD MILLION)

- TABLE 367 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 368 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PAYERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 369 REST OF MIDDLE EAST & AFRICA: DIGITAL HEALTH MARKET FOR HEALTHCARE PROVIDERS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 370 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL HEALTH MARKET, JANUARY 2022-JULY 2025

- TABLE 371 DIGITAL HEALTH MARKET: DEGREE OF COMPETITION

- TABLE 372 DIGITAL HEALTH MARKET: REGION FOOTPRINT

- TABLE 373 DIGITAL HEALTH MARKET: OFFERING FOOTPRINT

- TABLE 374 DIGITAL HEALTH MARKET: DISEASE FOOTPRINT

- TABLE 375 DIGITAL HEALTH MARKET: USE CASE FOOTPRINT

- TABLE 376 DIGITAL HEALTH MARKET: END USER FOOTPRINT

- TABLE 1 DIGITAL HEALTH MARKET: DETAILED LIST OF KEY STARTUPS/SME PLAYERS

- TABLE 377 DIGITAL HEALTH MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY REGION

- TABLE 378 DIGITAL HEALTH MARKET: COMPETITIVE BENCHMARKING OF KEY EMERGING PLAYERS/STARTUPS, BY DISEASE

- TABLE 379 DIGITAL HEALTH MARKET: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 380 DIGITAL HEALTH MARKET: DEALS, JANUARY 2022-JULY 2025

- TABLE 381 DIGITAL HEALTH MARKET: OTHER DEVELOPMENTS, JANUARY 2022-JULY 2025

- TABLE 382 MEDTRONIC: COMPANY OVERVIEW

- TABLE 383 MEDTRONIC: PRODUCTS OFFERED

- TABLE 384 MEDTRONIC: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 385 MEDTRONIC: DEALS, JANUARY 2022-JULY 2025

- TABLE 386 MEDTRONIC: OTHER DEVELOPMENTS, JANUARY 2022-JULY 2025

- TABLE 387 ABBOTT: COMPANY OVERVIEW

- TABLE 388 ABBOTT: PRODUCTS OFFERED

- TABLE 389 ABBOTT: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 390 ABBOTT: DEALS, JANUARY 2022-JULY 2025

- TABLE 391 DEXCOM, INC.: COMPANY OVERVIEW

- TABLE 392 DEXCOM, INC.: PRODUCTS OFFERED

- TABLE 393 DEXCOM, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 394 DEXCOM, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 395 KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

- TABLE 396 KONINKLIJKE PHILIPS N.V.: PRODUCTS OFFERED

- TABLE 397 KONINKLIJKE PHILIPS N.V.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 398 KONINKLIJKE PHILIPS N.V.: DEALS, JANUARY 2022-JULY 2025

- TABLE 399 KONINKLIJKE PHILIPS N.V.: EXPANSIONS, JANUARY 2022-JULY 2025

- TABLE 400 FITBIT, INC.: COMPANY OVERVIEW

- TABLE 401 FITBIT, INC.: PRODUCTS OFFERED

- TABLE 402 FITBIT, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 403 FITBIT, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 404 OMRON HEALTHCARE, INC.: COMPANY OVERVIEW

- TABLE 405 OMRON HEALTHCARE, INC.: PRODUCTS OFFERED

- TABLE 406 OMRON HEALTHCARE, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 407 OMRON HEALTHCARE, INC., JANUARY 2022-JULY 2025

- TABLE 408 APPLE, INC.: COMPANY OVERVIEW

- TABLE 409 APPLE, INC.: PRODUCTS OFFERED

- TABLE 410 APPLE, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 411 APPLE, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 412 BOSTON SCIENTIFIC CORPORATION: COMPANY OVERVIEW

- TABLE 413 BOSTON SCIENTIFIC CORPORATION: PRODUCTS OFFERED

- TABLE 414 BOSTON SCIENTIFIC CORPORATION: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 415 BOSTON SCIENTIFIC CORPORATION: DEALS, JANUARY 2022-JULY 2025

- TABLE 416 MASIMO: COMPANY OVERVIEW

- TABLE 417 MASIMO: PRODUCTS OFFERED

- TABLE 418 MASIMO: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 419 MASIMO: DEALS, JANUARY 2022-JULY 2025

- TABLE 420 TELADOC HEALTH, INC.: COMPANY OVERVIEW

- TABLE 421 TELADOC HEALTH, INC.: PRODUCTS OFFERED

- TABLE 422 TELADOC HEALTH, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 423 TELADOC HEALTH, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 424 AMERICAN WELL: COMPANY OVERVIEW

- TABLE 425 AMERICAN WELL: PRODUCTS OFFERED

- TABLE 426 AMERICAN WELL: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 427 AMERICAN WELL: DEALS, JANUARY 2022-JULY 2025

- TABLE 428 AMERICAN WELL: OTHER DEVELOPMENTS, JANUARY 2022-JULY 2025

- TABLE 429 HIMS & HERS HEALTH, INC.: COMPANY OVERVIEW

- TABLE 430 HIMS & HERS HEALTH, INC.: PRODUCTS OFFERED

- TABLE 431 HIMS & HERS HEALTH, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 432 HIMS & HERS HEALTH, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 433 HEADSPACE: COMPANY OVERVIEW

- TABLE 434 HEADSPACE: PRODUCTS OFFERED

- TABLE 435 HEADSPACE: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 436 HEADSPACE: DEALS, JANUARY 2022-JULY 2025

- TABLE 437 NOOM, INC.: COMPANY OVERVIEW

- TABLE 438 NOOM, INC.: PRODUCTS OFFERED

- TABLE 439 NOOM, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 440 NOOM, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 441 CEREBRAL INC.: COMPANY OVERVIEW

- TABLE 442 CEREBRAL INC.: PRODUCTS OFFERED

- TABLE 443 CEREBRAL INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 444 CEREBRAL INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 445 EPIC SYSTEMS CORPORATION: COMPANY OVERVIEW

- TABLE 446 EPIC SYSTEMS CORPORATION: PRODUCTS OFFERED

- TABLE 447 EPIC SYSTEM CORPORATION: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 448 EPIC SYSTEM CORPORATION: DEALS, JANUARY 2022-JULY 2025

- TABLE 449 OMADA HEALTH INC.: COMPANY OVERVIEW

- TABLE 450 OMADA HEALTH INC.: PRODUCTS OFFERED

- TABLE 451 OMADA HEALTH INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 452 OMADA HEALTH INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 453 ORACLE: COMPANY OVERVIEW

- TABLE 454 ORACLE: PRODUCTS OFFERED

- TABLE 455 ORACLE: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 456 ORACLE: DEALS, JANUARY 2022-JULY 2025

- TABLE 457 CLICK THERAPEUTICS, INC.: COMPANY OVERVIEW

- TABLE 458 CLICK THERAPEUTICS, INC.: PRODUCTS OFFERED

- TABLE 459 CLICK THERAPEUTICS, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 460 CLICK THERAPEUTICS, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 461 WELLDOC, INC.: COMPANY OVERVIEW

- TABLE 462 WELLDOC, INC.: PRODUCTS OFFERED

- TABLE 463 WELLDOC, INC.: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 464 WELLDOC, INC.: DEALS, JANUARY 2022-JULY 2025

- TABLE 465 EVERLYWELL: COMPANY OVERVIEW

- TABLE 466 EVERLYWELL: PRODUCTS OFFERED

- TABLE 467 EVERLYWELL: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-JULY 2025

- TABLE 468 EVERLYWELL: DEALS, JANUARY 2022-JULY 2025

List of Figures

- FIGURE 1 RESEARCH DESIGN

- FIGURE 2 PRIMARY SOURCES

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 5 SUPPLY-SIDE MARKET SIZE ESTIMATION

- FIGURE 6 DIGITAL HEALTH MARKET: REVENUE ESTIMATION APPROACH

- FIGURE 7 BOTTOM-UP APPROACH: END USER SPENDING ON DIGITAL HEALTH

- FIGURE 8 TOP-DOWN APPROACH

- FIGURE 9 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES (2025-2030)

- FIGURE 10 DIGITAL HEALTH MARKET: CAGR PROJECTIONS

- FIGURE 11 DATA TRIANGULATION METHODOLOGY

- FIGURE 12 DIGITAL HEALTH MARKET, BY OFFERING, 2025 VS. 2030 (USD MILLION)

- FIGURE 13 DIGITAL HEALTH MARKET, BY DISEASE, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 DIGITAL HEALTH MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 GEOGRAPHICAL SNAPSHOT OF DIGITAL HEALTH MARKET

- FIGURE 16 RISING FOCUS ON PATIENT-CENTRIC HEALTHCARE SOLUTIONS TO DRIVE MARKET

- FIGURE 17 HEALTHCARE PROVIDERS HELD LARGEST SHARE OF NORTH AMERICAN MARKET IN 2024

- FIGURE 18 MARKET IN INDIA TO REGISTER HIGHEST GROWTH

- FIGURE 19 ASIA PACIFIC TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 20 EMERGING ECONOMIES TO REGISTER HIGHER GROWTH BETWEEN 2025 & 2030

- FIGURE 21 DIGITAL HEALTH MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 22 SMARTPHONE USERS WORLDWIDE, 2016-2027 (BILLION)

- FIGURE 23 GERIATRIC POPULATION, BY REGION, 2010-2030 (% OF TOTAL POPULATION)

- FIGURE 24 DIGITAL HEALTH MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 25 DIGITAL HEALTH MARKET: ECOSYSTEM ANALYSIS

- FIGURE 26 DIGITAL HEALTH MARKET: SUPPLY CHAIN ANALYSIS (2024)

- FIGURE 27 DIGITAL HEALTH MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- FIGURE 29 KEY BUYING CRITERIA FOR DIGITAL HEALTH OFFERINGS

- FIGURE 30 PATENT PUBLICATION TRENDS IN DIGITAL HEALTH MARKET, 2015-2025

- FIGURE 31 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR "DIGITAL HEALTH" PATENTS (JANUARY 2015-MARCH 2025)

- FIGURE 32 MAJOR PATENTS IN DIGITAL HEALTH MARKET (JANUARY 2015-MARCH 2025)

- FIGURE 33 INVESTMENT LANDSCAPE AND FUNDING SCENARIO, 2025 (USD MILLION)

- FIGURE 34 IMPORTS OF PRODUCTS UNDER HSN CODE 8518, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 35 EXPORTS OF PRODUCTS UNDER HSN CODE 8518, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 36 IMPORTS OF PRODUCTS UNDER HSN CODE 9021, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 37 EXPORTS OF PRODUCTS UNDER HSN CODE 9021, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 38 IMPORTS OF PRODUCTS UNDER HSN CODE 9022, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 39 EXPORTS OF PRODUCTS UNDER HSN CODE 9022, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 40 IMPORTS OF PRODUCTS UNDER HSN CODE 9018, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 41 EXPORTS OF PRODUCTS UNDER HSN CODE 9018, BY COUNTRY, 2024 (USD THOUSAND)

- FIGURE 42 MARKET POTENTIAL OF AI/GENERATIVE AI DIGITAL HEALTH ACROSS INDUSTRIES

- FIGURE 43 NORTH AMERICA: DIGITAL HEALTH MARKET SNAPSHOT

- FIGURE 44 ASIA PACIFIC: DIGITAL HEALTH MARKET SNAPSHOT

- FIGURE 45 REVENUE ANALYSIS OF KEY PLAYERS IN DIGITAL HEALTH MARKET, 2020-2024 (USD MILLION)

- FIGURE 46 MARKET SHARE ANALYSIS OF KEY PLAYERS IN DIGITAL HEALTH MARKET (2024)

- FIGURE 47 DIGITAL HEALTH MARKET: BRAND/SOFTWARE COMPARATIVE ANALYSIS

- FIGURE 48 EV/EBITDA OF KEY VENDORS, 2025

- FIGURE 49 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS, 2025

- FIGURE 50 DIGITAL HEALTH MARKET: COMPANY EVALUATION MATRIX, 2024

- FIGURE 51 DIGITAL HEALTH MARKET: COMPANY FOOTPRINT

- FIGURE 52 DIGITAL HEALTH MARKET: STARTUP/SME EVALUATION MATRIX, 2024

- FIGURE 53 MEDTRONIC: COMPANY SNAPSHOT (2025)

- FIGURE 54 ABBOTT: COMPANY SNAPSHOT (2024)

- FIGURE 55 DEXCOM, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 56 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT (2024)

- FIGURE 57 GOOGLE: COMPANY SNAPSHOT (2024)

- FIGURE 58 OMRON HEALTHCARE, INC.: COMPANY SNAPSHOT (2023)

- FIGURE 59 APPLE, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 60 BOSTON SCIENTIFIC CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 61 MASIMO: COMPANY SNAPSHOT (2024)

- FIGURE 62 TELADOC HEALTH, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 63 AMERICAN WELL: COMPANY SNAPSHOT (2024)

- FIGURE 64 HIMS & HERS HEALTH, INC.: COMPANY SNAPSHOT (2024)

- FIGURE 65 OMADA HEALTH INC.: COMPANY SNAPSHOT (2024)

- FIGURE 66 ORACLE: COMPANY SNAPSHOT (2025)