PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1822291

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1822291

Lateral Flow Assay Components Market by Type (Membrane, Pad), Application (Clinical Testing (Infectious, Cardiac Marker Test, Fertility, Pregnancy, Cholesterol Testing), Veterinary, Food Safety), Technique, End User & Region - Global Forecast to 2030

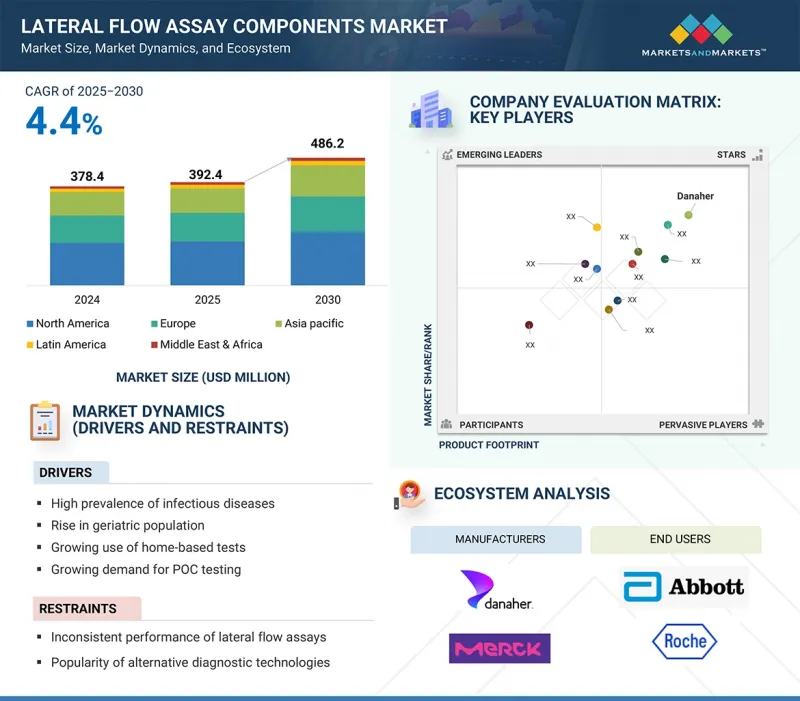

The global lateral flow assay (LFA) components market is projected to reach USD 486.2 million by 2030 from USD 392.4 million in 2025, at a CAGR of 4.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Product, Application, Technique, Sample Type, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries |

In recent years, the lateral flow assay components market has gained significant momentum, driven by the increasing prevalence of infectious diseases, rising demand for point-of-care testing, and greater adoption of home-based diagnostics. Ongoing improvements in membranes, pads, and related materials have improved test accuracy and reduced turnaround times, expanding their use in clinical, veterinary, food safety, and drug development settings. Along with established companies, a growing number of small and specialized manufacturers are leading innovation in material design and production methods, offering unique solutions that meet diverse end-user needs and requirements.

"The sandwich assays segment of the lateral flow assay components market, by technique, is expected to hold the largest position during the forecast period."

The lateral flow assay components market is divided into sandwich assays, competitive assays, and multiplex detection assays. Among these, sandwich assays held the largest market share in 2024, due to their higher sensitivity, specificity, and suitability for detecting larger analytes like bacterial pathogens, viral antigens, and key biomarkers. In this method, the analyte is "sandwiched" between two highly specific antibodies, creating a signal that directly correlates with analyte concentration, ensuring reliable and quantitative results. The dominance of sandwich assays is further supported by their use in some of the most common diagnostic tests, including pregnancy testing (hCG), infectious disease testing (HIV, hepatitis B, H. pylori), and cardiac marker detection (troponin, CK-MB, myoglobin). Their ability to consistently produce strong control line signals, regardless of analyte levels, improves test reliability-a vital aspect for clinical and home-based diagnostics. As healthcare providers increasingly adopt point-of-care solutions, the demand for membranes, conjugate pads, and nanoparticles tailored to sandwich assay formats continues to grow. In contrast, competitive assays-more suitable for small molecules with a single antigenic determinant-remain important in areas like drug-of-abuse testing and certain food safety applications. Meanwhile, multiplex detection assays are gaining popularity for their capacity to analyze multiple targets simultaneously. Nevertheless, it is the extensive clinical applications and established diagnostic accuracy of sandwich assays that primarily drive the consumption of components worldwide market.

"The medical device manufacturing companies accounted for the largest market share in the lateral flow assay components market, by end user."

The lateral flow assay components market, by end user, is divided into medical device manufacturing companies and medical device contract manufacturing companies. Among these, medical device manufacturing companies led the market in 2024, holding the largest share because of their extensive role in designing, engineering, and producing a wide range of diagnostic devices. These companies, including Abbott (US), Hoffmann-La Roche (Switzerland), Danaher Corporation (US), Siemens Healthineers (Germany), Bio-Rad Laboratories (US), Thermo Fisher Scientific (US), PerkinElmer (US), Hologic (US), and Merck KGaA (Germany), are the main consumers of membranes, pads, conjugates, and housing materials. The increasing prevalence of infectious diseases, the growing elderly population, and the rising adoption of home-based and point-of-care diagnostics have driven the integration of LFA components into diagnostic product portfolios. This has made medical device manufacturers the primary demand drivers in the component market. Meanwhile, medical device contract manufacturing companies form a steadily growing segment. As OEMs outsource production for cost savings, faster scalability, and access to specialized expertise, contract manufacturers are becoming important buyers of membranes, pads, and other consumables. This trend is especially strong in Asia-Pacific, where favorable labor costs and supportive manufacturing ecosystems encourage global companies to partner with local producers, further boosting demand for components from this segment.

"The Asia Pacific is the fastest-growing region of the lateral flow assay components market by region."

The global lateral flow assay components market is segmented into five segments, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific region is expected to achieve the highest CAGR in the lateral flow assay components market during the forecast period, driven by rapid healthcare expansion, strong economic growth, and increasing investments from both domestic and international players. Key contributors to this growth include high-growth countries such as China, India, Japan, South Korea, Taiwan, Australia, and Singapore. Factors like rising healthcare expenditure, an aging population, longer life expectancy, and the increasing demand for point-of-care and home-based testing are boosting demand for membranes, conjugate pads, gold nanoparticles, and other LFA components. China and India remain the most influential markets due to their expanding healthcare infrastructure, rising incomes, and government focus on diagnostics. India's increased health budget for FY 2023-24 underscores this commitment. Meanwhile, Southeast Asian economies like Vietnam, Indonesia, and the Philippines are emerging as new growth centers, driven by strong GDP growth, increased manufacturing capacity, and foreign investment. Despite these growth drivers, challenges such as limited awareness of near-patient testing benefits, inadequate reimbursement structures, and infrastructural gaps in rural and remote areas pose barriers to full adoption. Nevertheless, the presence of competitive local manufacturers such as Advanced Microdevices Ltd. (India), J. Mitra & Co. (India), Nupore Filtration (China), and Equinox (China), alongside multinational suppliers, is strengthening the region's LFA component ecosystem and maintaining its position as the fastest-growing regional market.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1: 38%, Tier 2: 29%, and Tier 3: 33%

- By Designation: C Level: 27%, Director Level: 18%, and Others: 55%

- By Region: North America: 50%, Europe: 20%, Asia Pacific: 20%, Latin America: 7%, and Middle East & Africa: 3%

Note 1: Companies are classified into tiers based on their total revenue. As of 2023, Tier 1 = >USD 10.00 billion, Tier 2 = USD 1.00 billion to USD 10.00 billion, and Tier 3 = <USD 1.00 billion.

Note 2: C-level primaries include CEOs, CFOs, COOs, and VPs.

Note 3: Other designations include sales managers, marketing managers, business development managers, product managers, distributors, and suppliers.

The major players operating in the lateral flow assay components market are Danaher Corporation (US), Sartorius AG (Germany), Merck KGaA (Germany), Ahlstrom (Finland), Advanced Microdevices Pvt. Ltd. (India), DCN Diagnostics (US), Fortis Life Sciences, LLC. (US), Cobetter (China), Axiva Sichem Pvt. Ltd. (India), and Nupore Filtration Systems (India).

Research Coverage

This report examines the lateral flow assay components market based on product, application, technique, end user, and region. It also evaluates factors such as drivers, restraints, opportunities, and challenges impacting market growth, and provides details about the competitive landscape of market leaders. Additionally, the report analyzes micro-markets concerning their individual growth trends. It forecasts the revenue of market segments across five major regions and their respective countries regions).

Reasons to Buy the Report

The report will help both established firms and smaller entrants assess the market, which can assist them in gaining a larger market share. Companies purchasing the report can utilize one or a combination of the strategies listed below to strengthen their market position presence.

This report provides insights into the following pointers:

- Analysis of: key drivers (High prevalence of infectious diseases driving market demand, Rise in geriatric population boosting demand, Growing use of home-based tests driving component consumption, Growing demand for POC testing), restraints (Inconsistent performance of LFAs impacting component demand, Alternative diagnostic technologies limiting adoption), opportunities (Expanding Applications Driving Demand for LFA Components, Rising Demand for LFA Components in the Food & Beverage Sector), challenges (Limited Reimbursements Restricting LFA Component Market, Need for Specialized Storage and Shipping for LFA Membranes)

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the lateral flow assay components market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product launches in the lateral flow assay components market

- Market Development: Comprehensive information on lucrative emerging regions.

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the lateral flow assay components market

- Competitive Assessment: In-depth assessment of market segments, growth strategies, revenue analysis, and products of the leading market players

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.4.1 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.2 RESEARCH APPROACH

- 2.2.1 SECONDARY DATA

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Primary sources

- 2.2.2.2 Key industry insights

- 2.2.2.3 Key data from primary sources

- 2.2.2.4 Breakdown of primary interviews

- 2.2.1 SECONDARY DATA

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Approach 1: Company revenue estimation approach

- 2.3.1.2 Approach 2: Based on cost of goods sold & component share

- 2.3.1.3 Approach 3: Primary interviews

- 2.3.1.4 Growth forecast

- 2.3.1.5 CAGR projections

- 2.3.2 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.5.1 STUDY-RELATED ASSUMPTIONS

- 2.5.2 PARAMETRIC ASSUMPTIONS

- 2.5.3 GROWTH RATE ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 LATERAL FLOW ASSAY (LFA) COMPONENTS MARKET OVERVIEW

- 4.2 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT AND COUNTRY

- 4.3 LATERAL FLOW ASSAY COMPONENTS MARKET, BY KEY COUNTRY

- 4.4 LATERAL FLOW ASSAY COMPONENTS MARKET, REGIONAL MIX, 2025 VS. 2030

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 High prevalence of infectious diseases

- 5.2.1.2 Rise in geriatric population

- 5.2.1.3 Growing use of home-based tests driving consumption of components

- 5.2.1.4 Growing demand for POC testing

- 5.2.2 RESTRAINTS

- 5.2.2.1 Inconsistent performance of LFAs impacting demand for components

- 5.2.2.2 Alternative diagnostic technologies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expanding applications driving demand for LFA components

- 5.2.3.2 Rising demand for LFA components in food & beverage industry

- 5.2.4 CHALLENGES

- 5.2.4.1 Limited reimbursements

- 5.2.4.2 Need for specialized storage and shipping for LFA components

- 5.2.1 DRIVERS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND OF LATERAL FLOW ASSAY COMPONENTS, BY KEY PLAYERS, 2023-2025

- 5.4.2 AVERAGE SELLING PRICE TREND OF LATERAL FLOW ASSAY COMPONENTS, BY REGION, 2023-2025

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 ECOSYSTEM ANALYSIS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 TECHNOLOGY ANALYSIS

- 5.9.1 KEY TECHNOLOGIES

- 5.9.1.1 Membrane technology

- 5.9.2 COMPLEMENTARY TECHNOLOGIES

- 5.9.2.1 Lyophilization

- 5.9.3 ADJACENT TECHNOLOGIES

- 5.9.3.1 Enzyme-linked immunosorbent assays

- 5.9.1 KEY TECHNOLOGIES

- 5.10 PATENT ANALYSIS

- 5.10.1 LIST OF MAJOR PATENTS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT DATA (HS CODE 382200)

- 5.11.2 EXPORT DATA (HS CODE 382200)

- 5.12 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.13 REGULATORY LANDSCAPE

- 5.13.1 REGULATORY ANALYSIS

- 5.13.1.1 North America

- 5.13.1.2 Europe

- 5.13.1.3 Asia Pacific

- 5.13.1.3.1 India

- 5.13.1.3.2 China

- 5.13.1.3.3 Japan

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.2.1 North America

- 5.13.2.2 Europe

- 5.13.2.3 Asia Pacific

- 5.13.2.4 Latin America

- 5.13.2.5 Rest of the World

- 5.13.1 REGULATORY ANALYSIS

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF BUYERS

- 5.14.4 BARGAINING POWER OF SUPPLIERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 IMPACT OF AI ON LATERAL FLOW ASSAY COMPONENTS MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 POTENTIAL OF AI IN LATERAL FLOW ASSAY COMPONENTS MARKET

- 5.16.3 AI USE CASES

- 5.16.4 FUTURE OF AI IN LATERAL FLOW ASSAY COMPONENTS MARKET

- 5.17 IMPACT OF 2025 US TARIFFS

- 5.17.1 INTRODUCTION

- 5.17.2 KEY TARIFF RATES

- 5.17.3 PRICE IMPACT ANALYSIS

- 5.17.4 KEY IMPACTS ON REGIONS

- 5.17.4.1 North America

- 5.17.4.2 Europe

- 5.17.4.3 Asia Pacific

- 5.17.5 IMPACT ON END-USE INDUSTRIES

- 5.17.5.1 Medical device manufacturing companies

6 LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT

- 6.1 INTRODUCTION

- 6.2 MEMBRANES

- 6.2.1 NITROCELLULOSE MEMBRANES

- 6.2.1.1 High protein-binding affinity to drive growth

- 6.2.2 OTHER MEMBRANES

- 6.2.1 NITROCELLULOSE MEMBRANES

- 6.3 PADS

- 6.3.1 SAMPLE PADS

- 6.3.1.1 Role of sample pads in ensuring even and controlled sample distribution to drive growth

- 6.3.2 CONJUGATE PADS

- 6.3.2.1 Conjugate pads as key performance controllers in lateral flow immunoassays to drive growth

- 6.3.3 ABSORBENT PADS

- 6.3.3.1 Absorbent pads as critical backflow preventers in l ateral flow immunoassays to drive growth

- 6.3.1 SAMPLE PADS

- 6.4 OTHERS

7 LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE

- 7.1 INTRODUCTION

- 7.2 SANDWICH ASSAYS

- 7.2.1 SUPERIOR SENSITIVITY AND SPECIFICITY TO DRIVE DEMAND

- 7.3 COMPETITIVE ASSAYS

- 7.3.1 LOWER SENSITIVITY OF COMPETITIVE ASSAYS COMPARED TO SANDWICH FORMATS TO LIMIT GROWTH

- 7.4 MULTIPLEX DETECTION ASSAYS

- 7.4.1 ADOPTION OF MULTI-ANALYTE ASSAYS TO DRIVE GROWTH

8 LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 CLINICAL TESTING

- 8.2.1 INFECTIOUS DISEASE TESTING

- 8.2.1.1 Rising demand in emerging markets to drive growth

- 8.2.2 CARDIAC MARKER TESTING

- 8.2.2.1 Cardiovascular disease prevalence to drive demand

- 8.2.3 PREGNANCY & FERTILITY TESTING

- 8.2.3.1 Lifestyle changes and rising infertility rates to fuel demand

- 8.2.4 CHOLESTEROL TESTING/LIPID PROFILING

- 8.2.4.1 Growing prevalence of obesity and cardiovascular diseases to drive demand

- 8.2.5 DRUG-OF-ABUSE TESTING

- 8.2.5.1 Technological advancements and workplace testing initiatives to fuel growth

- 8.2.6 OTHER CLINICAL TESTING APPLICATIONS

- 8.2.1 INFECTIOUS DISEASE TESTING

- 8.3 VETERINARY DIAGNOSTICS

- 8.3.1 INFECTIOUS DISEASE OUTBREAKS IN LARGE LIVESTOCK ANIMALS TO DRIVE DEMAND

- 8.4 FOOD SAFETY & ENVIRONMENTAL TESTING

- 8.4.1 HIGH SENSITIVITY AND EASE OF USE TO FUEL DEMAND FOR LATERAL FLOW ASSAYS IN FOOD SAFETY

- 8.5 DRUG DEVELOPMENT & QUALITY TESTING

- 8.5.1 RISING EMPHASIS ON PRODUCT SAFETY AND QUALITY ASSURANCE TO DRIVE GROWTH

9 LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.2 MEDICAL DEVICE MANUFACTURING COMPANIES

- 9.2.1 RISING POINT-OF-CARE TESTING TO BOOST ADOPTION

- 9.3 MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES

- 9.3.1 GROWING FOCUS ON FAST AND EARLY DIAGNOSIS TO DRIVE GROWTH

10 LATERAL FLOW ASSAY COMPONENTS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 MACROECONOMIC OUTLOOK

- 10.2.2 US

- 10.2.2.1 Expanding patient base and healthcare needs to drive demand

- 10.2.3 CANADA

- 10.2.3.1 Research funding and policy support to drive demand

- 10.3 EUROPE

- 10.3.1 MACROECONOMIC OUTLOOK

- 10.3.2 GERMANY

- 10.3.2.1 Rising point-of-care testing to drive growth

- 10.3.3 FRANCE

- 10.3.3.1 Aging population and healthcare policies shaping demand for LFA components

- 10.3.4 UK

- 10.3.4.1 Rising burden of chronic conditions to drive demand

- 10.3.5 ITALY

- 10.3.5.1 Decentralization of healthcare services to support demand

- 10.3.6 SPAIN

- 10.3.6.1 Aging demographics and strong healthcare system to fuel demand

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 MACROECONOMIC OUTLOOK

- 10.4.2 CHINA

- 10.4.2.1 Modernized healthcare system to drive market

- 10.4.3 JAPAN

- 10.4.3.1 Aging population and advanced healthcare system to fuel demand

- 10.4.4 INDIA

- 10.4.4.1 Growing base of local manufacturers to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Rising infectious disease burden and healthcare spending to drive market

- 10.4.6 REST OF ASIA PACIFIC

- 10.5 LATIN AMERICA

- 10.5.1 MACROECONOMIC OUTLOOK

- 10.5.2 BRAZIL

- 10.5.2.1 Growing healthcare investments and aging population to drive market

- 10.5.3 MEXICO

- 10.5.3.1 Expanding healthcare access and rising chronic disease burden to drive demand

- 10.5.4 REST OF LATIN AMERICA

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 EXPANDING HEALTHCARE BUDGETS TO DRIVE GROWTH

- 10.6.2 MACROECONOMIC OUTLOOK

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN LATERAL FLOW ASSAY COMPONENTS MARKET

- 11.3 REVENUE ANALYSIS, 2022-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- 11.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.5.5.1 Company footprint

- 11.5.5.2 Region footprint

- 11.5.5.3 Product footprint

- 11.5.5.4 Application footprint

- 11.5.5.5 Technique footprint

- 11.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- 11.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.6.5.1 List of key startups/SMEs

- 11.6.5.2 Competitive benchmarking of key startups/SMEs

- 11.7 COMPANY VALUATION AND FINANCIAL METRICS

- 11.7.1 COMPANY VALUATION

- 11.7.2 FINANCIAL METRICS

- 11.8 BRAND/PRODUCT COMPARISON

- 11.9 COMPETITIVE SCENARIO

- 11.9.1 EXPANSIONS

- 11.9.2 OTHER DEVELOPMENTS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 DANAHER CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Expansions

- 12.1.1.3.2 Others

- 12.1.1.4 MnM view

- 12.1.1.4.1 Key strengths

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 SARTORIUS AG

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 MnM view

- 12.1.2.3.1 Key strengths

- 12.1.2.3.2 Strategic choices

- 12.1.2.3.3 Weaknesses and competitive threats

- 12.1.3 AHLSTROM

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 MnM view

- 12.1.3.3.1 Key strengths

- 12.1.3.3.2 Strategic choices

- 12.1.3.3.3 Weaknesses and competitive threats

- 12.1.4 MERCK KGAA

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Expansions

- 12.1.5 ADVANCED MICRODEVICES PVT. LTD.

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.6 DCN DIAGNOSTICS

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.7 FORTIS LIFE SCIENCES, LLC.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.8 COBETTER

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.9 AXIVA SICHEM PVT. LTD.

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.10 NUPORE FILTRATION SYSTEMS

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.1 DANAHER CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 BALLYA

- 12.2.2 EQUINOX

- 12.2.3 CYTODIAGNOSTICS INC

- 12.2.4 POREX

- 12.2.5 KENOSHA

- 12.2.6 ANTITECK LIFE SCIENCES LIMITED

- 12.2.7 MINIPORE MICRO PRODUCTS

- 12.2.8 PRAHAS HEALTHCARE

- 12.2.9 NANOHYBRIDS

- 12.2.10 PROGNOSIS BIOTECH S.A.

- 12.2.11 LATERAL DX

- 12.2.12 BANGS LABORATORIES

- 12.2.13 BBI SOLUTIONS

- 12.2.14 SONA NANOTECH

- 12.2.15 ZHEJIANG TAILIN BIOENGINEERING CO., LTD.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 LATERAL FLOW ASSAY COMPONENTS MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 LATERAL FLOW ASSAY COMPONENTS MARKET: RISK ASSESSMENT

- TABLE 3 REAL INCIDENCE OF HIV, 2023 (MILLION PEOPLE)

- TABLE 4 TOTAL TB INCIDENCE, 2023

- TABLE 5 POPULATION AGED 65 AND ABOVE (% OF TOTAL POPULATION), 2024

- TABLE 6 AVERAGE SELLING PRICE TREND OF LATERAL FLOW ASSAY COMPONENTS, BY KEY PLAYERS, 2023-2025

- TABLE 7 AVERAGE SELLING PRICE TREND OF LATERAL FLOW ASSAY COMPONENTS, BY REGION, 2023-2025

- TABLE 8 LATERAL FLOW ASSAY COMPONENTS MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 9 LATERAL FLOW ASSAY COMPONENTS MARKET: LIST OF MAJOR PATENTS

- TABLE 10 IMPORT DATA (HS CODE 382200), BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 11 EXPORT DATA (HS CODE 382200), BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 12 LATERAL FLOW ASSAY COMPONENTS MARKET: KEY CONFERENCES & EVENTS, 2025-2026

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 LATERAL FLOW ASSAY COMPONENTS MARKET: IMPACT OF PORTER'S FIVE FORCES

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR LATERAL FLOW ASSAY COMPONENTS, BY END USER (%)

- TABLE 20 KEY BUYING CRITERIA FOR LATERAL FLOW ASSAY COMPONENTS, BY END USER

- TABLE 21 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 22 LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 23 LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 24 LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEMBRANES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 25 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 26 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 27 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 28 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 29 LATERAL FLOW ASSAY COMPONENTS MARKET FOR NITROCELLULOSE MEMBRANES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 30 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR NITROCELLULOSE MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 31 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR NITROCELLULOSE MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 32 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR NITROCELLULOSE MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 33 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR NITROCELLULOSE MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 34 LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER MEMBRANES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 35 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 36 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 37 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 38 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER MEMBRANES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 39 EXAMPLES OF DIFFERENT MATERIALS USED IN MANUFACTURING LATERAL FLOW ASSAY PADS

- TABLE 40 LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 41 LATERAL FLOW ASSAY COMPONENTS MARKET FOR PADS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 42 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 43 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 44 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 45 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 46 LATERAL FLOW ASSAY COMPONENTS MARKET FOR SAMPLE PADS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 47 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SAMPLE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 48 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SAMPLE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 49 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SAMPLE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 50 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SAMPLE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 51 LATERAL FLOW ASSAY COMPONENTS MARKET FOR CONJUGATE PADS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 52 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CONJUGATE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 53 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CONJUGATE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 54 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CONJUGATE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 55 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CONJUGATE PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 56 LATERAL FLOW ASSAY COMPONENTS MARKET FOR ABSORBENT PADS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 57 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR ABSORBENT PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 58 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR ABSORBENT PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 59 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR ABSORBENT PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 60 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR ABSORBENT PADS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 61 LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER COMPONENTS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 62 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER COMPONENTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 63 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER COMPONENTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 64 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER COMPONENTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 65 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER COMPONENTS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 66 LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 67 LATERAL FLOW ASSAY COMPONENTS MARKET FOR SANDWICH ASSAYS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 68 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SANDWICH ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 69 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SANDWICH ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 70 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SANDWICH ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 71 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR SANDWICH ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 72 LATERAL FLOW ASSAY COMPONENTS MARKET FOR COMPETITIVE ASSAYS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 73 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR COMPETITIVE ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 74 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR COMPETITIVE ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 75 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR COMPETITIVE ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 76 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR COMPETITIVE ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 77 LATERAL FLOW ASSAY COMPONENTS MARKET FOR MULTIPLEX DETECTION ASSAYS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 78 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MULTIPLEX DETECTION ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 79 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MULTIPLEX DETECTION ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 80 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MULTIPLEX DETECTION ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 81 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MULTIPLEX DETECTION ASSAYS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 82 LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 83 LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 84 LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 85 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 86 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 87 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 88 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 89 GLOBAL NUMBER OF NEWLY DIAGNOSED TB CASES, 2023-2030 (MILLION)

- TABLE 90 LATERAL FLOW ASSAY COMPONENTS MARKET FOR INFECTIOUS DISEASE TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 91 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR INFECTIOUS DISEASE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 92 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR INFECTIOUS DISEASE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 93 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR INFECTIOUS DISEASE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 94 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR INFECTIOUS DISEASE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 95 LATERAL FLOW ASSAY COMPONENTS MARKET FOR CARDIAC MARKER TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 96 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CARDIAC MARKER TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 97 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CARDIAC MARKER TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 98 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CARDIAC MARKER TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 99 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CARDIAC MARKER TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 100 LATERAL FLOW ASSAY COMPONENTS MARKET FOR PREGNANCY & FERTILITY TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 101 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PREGNANCY & FERTILITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 102 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PREGNANCY & FERTILITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 103 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PREGNANCY & FERTILITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 104 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR PREGNANCY & FERTILITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 105 LATERAL FLOW ASSAY COMPONENTS MARKET FOR CHOLESTEROL TESTING/ LIPID PROFILING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 106 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CHOLESTEROL TESTING/LIPID PROFILING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 107 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CHOLESTEROL TESTING/LIPID PROFILING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 108 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CHOLESTEROL TESTING/LIPID PROFILING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 109 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CHOLESTEROL TESTING/LIPID PROFILING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 110 LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG-OF-ABUSE TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 111 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG-OF-ABUSE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 112 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG-OF-ABUSE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 113 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG-OF-ABUSE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 114 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG-OF-ABUSE TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 115 LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER CLINICAL TESTING APPLICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 116 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER CLINICAL TESTING APPLICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 117 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER CLINICAL TESTING APPLICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 118 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER CLINICAL TESTING APPLICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 119 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR OTHER CLINICAL TESTING APPLICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 120 LATERAL FLOW ASSAY COMPONENTS MARKET FOR VETERINARY DIAGNOSTICS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 121 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR VETERINARY DIAGNOSTICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 122 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR VETERINARY DIAGNOSTICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 123 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR VETERINARY DIAGNOSTICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 124 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR VETERINARY DIAGNOSTICS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 125 LATERAL FLOW ASSAY COMPONENTS MARKET FOR FOOD SAFETY & ENVIRONMENTAL TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 126 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR FOOD SAFETY & ENVIRONMENTAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 127 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR FOOD SAFETY & ENVIRONMENTAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 128 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR FOOD SAFETY & ENVIRONMENTAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 129 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR FOOD SAFETY & ENVIRONMENTAL TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 130 LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG DEVELOPMENT & QUALITY TESTING, BY REGION, 2023-2030 (USD MILLION)

- TABLE 131 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG DEVELOPMENT & QUALITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 132 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG DEVELOPMENT & QUALITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 133 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG DEVELOPMENT & QUALITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 134 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR DRUG DEVELOPMENT & QUALITY TESTING, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 135 LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 136 LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE MANUFACTURING COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 137 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 138 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 139 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 140 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 141 LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES, BY REGION, 2023-2030 (USD MILLION)

- TABLE 142 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 143 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 144 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 145 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 146 LATERAL FLOW ASSAY COMPONENTS MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 147 NORTH AMERICA: MACROECONOMIC INDICATORS

- TABLE 148 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 149 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 150 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 151 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 152 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 153 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 154 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 155 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 156 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 157 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 158 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 159 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 160 US: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 161 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 162 US: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 163 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 164 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 165 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 166 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 167 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 168 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 169 CANADA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 170 EUROPE: MACROECONOMIC INDICATORS

- TABLE 171 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 172 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 173 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 174 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 175 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 176 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 177 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 178 EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 179 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 180 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 181 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 182 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 183 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 184 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 185 GERMANY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 186 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 187 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 188 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 189 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 190 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 191 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 192 FRANCE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 193 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 194 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 195 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 196 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 197 UK: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 198 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 199 UK: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 200 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 201 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 202 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 203 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 204 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 205 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 206 ITALY: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 207 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 208 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 209 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 210 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 211 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 212 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 213 SPAIN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 214 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 215 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 216 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 217 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 218 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 219 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 220 REST OF EUROPE: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 221 ASIA PACIFIC: KEY MACROECONOMIC INDICATORS

- TABLE 222 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 223 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 224 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 225 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 226 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 227 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 228 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 229 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 230 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 231 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 232 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 233 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 234 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 235 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 236 CHINA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 237 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 238 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 239 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 240 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 241 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 242 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 243 JAPAN: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 244 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 245 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 246 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 247 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 248 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 249 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 250 INDIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 251 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 252 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 253 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 254 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 255 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 256 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 257 AUSTRALIA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 258 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 259 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 260 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 261 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 262 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 263 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 264 REST OF ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 265 LATIN AMERICA: KEY MACROECONOMIC INDICATORS

- TABLE 266 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 267 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 268 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 269 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 270 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 271 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 272 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 273 LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 274 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 275 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 276 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 277 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 278 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 279 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 280 BRAZIL: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 281 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 282 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 283 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 284 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 285 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 286 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 287 MEXICO: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 288 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 289 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 290 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 291 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 292 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 293 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 294 REST OF LATIN AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 295 MIDDLE EAST & AFRICA: KEY MACROECONOMIC INDICATORS

- TABLE 296 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2023-2030 (USD MILLION)

- TABLE 297 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY MEMBRANE TYPE, 2023-2030 (USD MILLION)

- TABLE 298 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY PAD TYPE, 2023-2030 (USD MILLION)

- TABLE 299 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- TABLE 300 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET FOR CLINICAL TESTING APPLICATIONS, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 301 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2023-2030 (USD MILLION)

- TABLE 302 MIDDLE EAST & AFRICA: LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2023-2030 (USD MILLION)

- TABLE 303 LATERAL FLOW ASSAY COMPONENTS MARKET: OVERVIEW OF STRATEGIES DEPLOYED BY KEY MANUFACTURING COMPANIES, JANUARY 2022-JULY 2025

- TABLE 304 LATERAL FLOW ASSAY COMPONENTS MARKET: DEGREE OF COMPETITION

- TABLE 305 LATERAL FLOW ASSAY COMPONENTS MARKET: REGION FOOTPRINT

- TABLE 306 LATERAL FLOW ASSAY COMPONENTS MARKET: PRODUCT FOOTPRINT

- TABLE 307 LATERAL FLOW ASSAY COMPONENTS MARKET: APPLICATION FOOTPRINT

- TABLE 308 LATERAL FLOW ASSAY COMPONENTS MARKET: TECHNIQUE FOOTPRINT

- TABLE 309 LATERAL FLOW ASSAY COMPONENTS MARKET: LIST OF STARTUPS/SMES

- TABLE 310 LATERAL FLOW ASSAY COMPONENTS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 311 LATERAL FLOW ASSAY COMPONENTS MARKET: EXPANSIONS, JANUARY 2022- JULY 2025

- TABLE 312 LATERAL FLOW ASSAY COMPONENTS MARKET: OTHER DEVELOPMENTS, JANUARY 2022- JULY 2025

- TABLE 313 DANAHER CORPORATION: COMPANY OVERVIEW

- TABLE 314 DANAHER CORPORATION: PRODUCTS OFFERED

- TABLE 315 DANAHER CORPORATION: EXPANSIONS, JANUARY 2022-JULY 2025

- TABLE 316 DANAHER CORPORATION: OTHERS, JANUARY 2022-JULY 2025

- TABLE 317 SARTORIUS AG: COMPANY OVERVIEW

- TABLE 318 SARTORIUS AG: PRODUCTS OFFERED

- TABLE 319 AHLSTROM: COMPANY OVERVIEW

- TABLE 320 AHLSTROM: PRODUCTS OFFERED

- TABLE 321 MERCK KGAA: COMPANY OVERVIEW

- TABLE 322 MERCK KGAA: PRODUCTS OFFERED

- TABLE 323 MERCK KGAA: EXPANSIONS, JANUARY 2022-JULY 2025

- TABLE 324 ADVANCED MICRODEVICES PVT. LTD.: COMPANY OVERVIEW

- TABLE 325 ADVANCED MICRODEVICES PVT. LTD.: PRODUCTS OFFERED

- TABLE 326 DCN DIAGNOSTICS: COMPANY OVERVIEW

- TABLE 327 DCN DIAGNOSTICS: PRODUCTS OFFERED

- TABLE 328 FORTIS LIFE SCIENCES, LLC.: COMPANY OVERVIEW

- TABLE 329 FORTIS LIFE SCIENCES, LLC.: PRODUCTS OFFERED

- TABLE 330 COBETTER: COMPANY OVERVIEW

- TABLE 331 COBETTER: PRODUCTS OFFERED

- TABLE 332 AXIVA SICHEM PVT. LTD.: COMPANY OVERVIEW

- TABLE 333 AXIVA SICHEM PVT. LTD.: PRODUCTS OFFERED

- TABLE 334 NUPORE FILTRATION SYSTEMS: COMPANY OVERVIEW

- TABLE 335 NUPORE FILTRATION SYSTEMS: PRODUCTS OFFERED

List of Figures

- FIGURE 1 LATERAL FLOW ASSAY COMPONENTS MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 LATERAL FLOW ASSAY COMPONENTS MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 BOTTOM-UP APPROACH: COMPANY REVENUE ESTIMATION APPROACH

- FIGURE 5 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS

- FIGURE 6 LATERAL FLOW ASSAY COMPONENTS MARKET: TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION METHODOLOGY

- FIGURE 8 LATERAL FLOW ASSAY COMPONENTS MARKET, BY PRODUCT, 2025 VS. 2030 (USD MILLION)

- FIGURE 9 LATERAL FLOW ASSAY COMPONENTS MARKET, BY TECHNIQUE, 2025 VS. 2030 (USD MILLION)

- FIGURE 10 LATERAL FLOW ASSAY COMPONENTS MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 11 LATERAL FLOW ASSAY COMPONENTS MARKET, BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 12 GEOGRAPHICAL SNAPSHOT OF LATERAL FLOW ASSAY COMPONENTS MARKET

- FIGURE 13 RISING NUMBER OF LOCAL MANUFACTURERS FOR COMPONENTS TO DRIVE MARKET

- FIGURE 14 MEMBRANES ACCOUNTED FOR LARGEST SHARE OF ASIA PACIFIC MARKET IN 2024

- FIGURE 15 CHINA TO RECORD HIGHEST GROWTH RATE FROM 2025 TO 2030

- FIGURE 16 ASIA PACIFIC TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 17 LATERAL FLOW ASSAY COMPONENTS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 LATERAL FLOW ASSAY COMPONENTS MARKET: TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 19 LATERAL FLOW ASSAY COMPONENTS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 20 LATERAL FLOW ASSAY COMPONENTS MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 21 LATERAL FLOW ASSAY COMPONENTS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 22 LATERAL FLOW ASSAY COMPONENTS MARKET: FUNDING AND NUMBER OF DEALS, 2021-2025

- FIGURE 23 PATENT ANALYSIS FOR LATERAL FLOW ASSAY COMPONENTS, JANUARY 2015-DECEMBER 2024

- FIGURE 24 LATERAL FLOW ASSAY COMPONENTS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 25 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR LATERAL FLOW ASSAY COMPONENTS, BY END USER

- FIGURE 26 KEY BUYING CRITERIA FOR LATERAL FLOW ASSAY COMPONENTS, BY END USER

- FIGURE 27 AI USE CASES

- FIGURE 28 NORTH AMERICA: LATERAL FLOW ASSAY COMPONENTS MARKET SNAPSHOT

- FIGURE 29 ASIA PACIFIC: LATERAL FLOW ASSAY COMPONENTS MARKET SNAPSHOT

- FIGURE 30 LATERAL FLOW ASSAY COMPONENTS MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2022-2024

- FIGURE 31 LATERAL FLOW ASSAY COMPONENTS MARKET SHARE ANALYSIS OF KEY PLAYERS, 2024

- FIGURE 32 RANKING OF KEY PLAYERS IN LATERAL FLOW ASSAY COMPONENTS MARKET, 2024

- FIGURE 33 LATERAL FLOW ASSAY COMPONENTS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 34 LATERAL FLOW ASSAY COMPONENTS MARKET: COMPANY FOOTPRINT

- FIGURE 35 LATERAL FLOW ASSAY COMPONENTS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 36 YEAR-TO-DATE (YTD) PRICE, TOTAL RETURN, AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 37 EV/EBITDA OF KEY VENDORS

- FIGURE 38 LATERAL FLOW ASSAY COMPONENTS MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 39 DANAHER CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 40 SARTORIUS AG: COMPANY SNAPSHOT (2024)

- FIGURE 41 AHLSTROM: COMPANY SNAPSHOT (2024)

- FIGURE 42 MERCK KGAA: COMPANY SNAPSHOT (2024)