PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1838152

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1838152

Aircraft Seals Market by Seal Type (Dynamic, Static) Material (Composites, Polymers, Metals), Aircraft Type (Commercial, Business & General Aviation, Military Aircraft, AAM, UAV), Application, End Use - Global Forecast to 2030

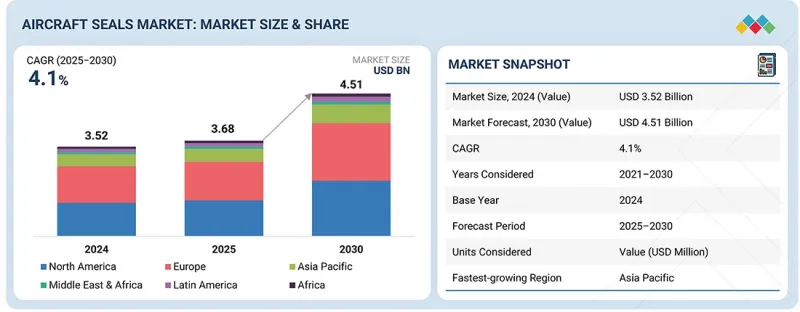

The aircraft seals market is expected to reach USD 4.51 billion by 2030, from USD 3.68 billion in 2025, at a CAGR of 4.1%. The aircraft seals market is set to grow steadily as fleet expansion, rising MRO cycles, and new-generation platforms drive higher demand for advanced sealing solutions.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Seal Type, Material, Application, Aircraft Type, End Use and Region |

| Regions covered | North America, Europe, APAC, RoW |

With increased focus on reducing cabin noise, enhancing fuel efficiency, and ensuring safety across critical systems, manufacturers are shifting toward high-performance materials such as silicone, FKM, and PTFE. Additionally, sustainability pressures and stricter chemical regulations are accelerating the reformulation of elastomers to meet compliance without compromising durability.

"Based on application, the engine systems segment is estimated to account for the largest market share in 2025."

Engine systems are estimated to lead the aircraft seals market through 2030, primarily due to the critical role seals play in maintaining safety, efficiency, and reliability in high-temperature and high-pressure environments. Modern aircraft engines operate at significantly higher overall pressure ratios and turbine inlet temperatures, which demand advanced sealing solutions capable of withstanding extreme thermal cycles and aggressive fluids. As engine OEMs such as GE, Rolls-Royce, and Pratt & Whitney pursue performance gains and fuel efficiency targets, the adoption of advanced elastomers, metal seals, and spring-energized PTFE components is accelerating.

The engine segment benefits from higher replacement rates in the aftermarket. Seals within combustors, nacelles, bleed-air ducts, and lubrication systems are subject to constant wear and require frequent inspection and replacement during maintenance cycles. This drives recurring demand, particularly in narrowbody fleets with high daily utilization. The global emphasis on reducing fuel burn and emissions intensifies the importance of minimizing leakage in engine seals, linking sealing performance directly to airline operating costs.

"Based on end use, the OEM segment is estimated to grow at the highest rate during the forecast period."

The OEM segment is projected to grow at the highest rate in the aircraft seals market, driven by substantial production backlogs across major commercial and regional aircraft programs. Airbus, Boeing, and emerging regional jet and turboprop manufacturers collectively hold multi-year order pipelines, ensuring consistent demand for factory-installed sealing components. Each new aircraft requires thousands of seals across nacelles, doors, windows, fuel tanks, and flight control systems, making OEM deliveries a primary revenue generator.

A key growth driver is the increasing integration of lightweight and more-electric designs at the assembly stage. Aircraft manufacturers are prioritizing seals that support simplified installation, tolerance flexibility, and compatibility with next-generation composites and metallic alloys. Unlike aftermarket replacements, OEM demand benefits from long-term design partnerships, where suppliers are locked into platform programs for decades.

"The Asia Pacific region is estimated to grow at the highest rate during the forecast period."

Asia-Pacific is projected to register the highest growth rate in the aircraft seals market through 2030, supported by rapid fleet expansion, infrastructure development, and rising air travel demand across emerging economies. China and India are spearheading commercial aircraft acquisitions, with large orders from Airbus and Boeing aimed at meeting strong passenger growth. Southeast Asian nations, including Indonesia, Vietnam, and the Philippines, are also expanding fleets, driving OEM seal demand for narrowbody and regional jets.

On the defense side, governments in Asia Pacific invest heavily in indigenous aircraft programs and modernization efforts. India's Tejas, South Korea's KF-21, and Japan's next-generation fighter programs all integrate advanced sealing technologies in engines, avionics, and airframes, creating opportunities for both local and global seal suppliers. The region also exhibits strong aftermarket potential. Harsh climatic conditions-ranging from tropical humidity to desert heat-accelerate wear in door, window, and nacelle seals, boosting replacement cycles. Rapid MRO expansion in Singapore, Malaysia, and China supports localized seal manufacturing and supply-chain presence.

Combined with government policies encouraging domestic aerospace production, APAC's scale of fleet growth and operational intensity will fuel the highest CAGR for aircraft seals, positioning the region as the fastest-growing market globally.

The breakdown of the profile of primary participants in the aircraft seals market:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East - 10%, Rest of the World (RoW) - 5%

Research Coverage

This market study covers the aircraft seals market across various segments and subsegments. It aims to estimate this market's size and growth potential across different parts based on the region. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to Buy This Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall aircraft seals market. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The aircraft seals market experiences growth and evolution driven by various factors. The report provides insights into the following pointers:

- Market drivers (fleet modernization & expansion. stringent safety & efficiency standards, growth in MRO activities), restraints (high material & certification costs, long qualification & replacement cycles, supply chain volatility), opportunities (next-generation aircraft programs, sustainability focus, regional demand growth), challenges (extreme operating conditions, intense competition, customization needs) several factors could contribute to an increase in the Aircraft Seals Market.

- Market Penetration: Comprehensive information on aircraft seals offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the aircraft seals market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the aircraft seals market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the aircraft seals market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, products, and manufacturing capabilities of leading players in the aircraft seals market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 MARKET SCOPE

- 1.4.1 AIRCRAFT SEALS MARKET SEGMENTATION & REGIONAL SCOPE

- 1.5 YEARS CONSIDERED

- 1.6 CURRENCY CONSIDERED

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Primary interview details

- 2.1.1 SECONDARY DATA

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.2.1 Increase in global aircraft fleet size to boost demand for seals from OEMs and aftermarket

- 2.2.2.2 Frequent replacement of aircraft seals

- 2.2.3 SUPPLY-SIDE ANALYSIS

- 2.2.3.1 Technological advancements and material innovations in seal manufacturing

- 2.3 MARKET SIZE ESTIMATION AND METHODOLOGY

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Aircraft seals market for OEMs

- 2.3.1.2 Aircraft seals aftermarket

- 2.3.2 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- 2.4.1 DATA TRIANGULATION THROUGH PRIMARY AND SECONDARY RESEARCH

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AIRCRAFT SEALS MARKET

- 4.2 AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS

- 4.3 AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT

- 4.4 AIRCRAFT SEALS MARKET, BY COMPOSITES

- 4.5 AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Fleet modernization and expansion

- 5.2.1.2 Growth in aircraft MRO

- 5.2.1.3 Material advancements

- 5.2.2 RESTRAINTS

- 5.2.2.1 High material and certification costs

- 5.2.2.2 Long qualification and replacement cycles

- 5.2.2.3 Volatile supply chain

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Next-generation aircraft programs

- 5.2.3.2 Focus on sustainability

- 5.2.3.3 Regional demand growth

- 5.2.4 CHALLENGES

- 5.2.4.1 Extreme operating conditions

- 5.2.4.2 Intense competition

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIALS

- 5.3.2 R&D

- 5.3.3 MANUFACTURING

- 5.3.4 DISTRIBUTION

- 5.3.5 END USERS

- 5.3.6 AFTER-SALES SERVICES

- 5.4 ECOSYSTEM MAPPING

- 5.4.1 MANUFACTURERS

- 5.4.2 SYSTEM INTEGRATORS

- 5.4.3 MRO

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 TRADE DATA

- 5.6.1 IMPORT SCENARIO (HS CODE 401693)

- 5.6.2 EXPORT SCENARIO (HS CODE 401693)

- 5.7 KEY CONFERENCES AND EVENTS, 2025-2027

- 5.8 TARIFF & REGULATORY LANDSCAPE

- 5.8.1 TARIFF DATA

- 5.8.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 BUYING CRITERIA

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ROLLS-ROYCE TRENT XWB ENGINE SEALS FOR WIDE-BODY AIRCRAFT

- 5.10.2 COMPOSITE AIRFRAME SEALING FOR BOEING 787 DREAMLINER

- 5.10.3 MAINTENANCE-FRIENDLY SEALS FOR EMBRAER E2 JETS

- 5.10.4 HYDRAULIC & FUEL SYSTEM SEALS FOR LOCKHEED MARTIN F-35 LIGHTNING II

- 5.11 TECHNOLOGY ANALYSIS

- 5.11.1 KEY TECHNOLOGIES

- 5.11.1.1 High temperature- and pressure-resistant seal architectures

- 5.11.1.2 Dynamic sealing solutions

- 5.11.1.3 Advanced manufacturing methods

- 5.11.2 COMPLEMENTARY TECHNOLOGIES

- 5.11.2.1 Coating and surface engineering

- 5.11.2.2 MRO process automation

- 5.11.3 ADJACENT TECHNOLOGIES

- 5.11.3.1 Electric & hybrid propulsion systems

- 5.11.3.2 Lightweight aircraft structures

- 5.11.1 KEY TECHNOLOGIES

- 5.12 PATENT ANALYSIS

- 5.13 INVESTMENT AND FUNDING SCENARIO

- 5.14 PRICING ANALYSIS

- 5.15 TOTAL COST OF OWNERSHIP

- 5.16 TECHNOLOGY ROADMAP

- 5.17 BUSINESS MODELS

- 5.18 IMPACT OF AI

- 5.18.1 INTRODUCTION

- 5.18.2 ADOPTION OF AI IN COMMERCIAL AVIATION BY TOP COUNTRIES

- 5.18.3 IMPACT OF AI ON AIRCRAFT SEALS MARKET

- 5.19 MACROECONOMIC OUTLOOK

- 5.19.1 NORTH AMERICA

- 5.19.2 EUROPE

- 5.19.3 ASIA PACIFIC

- 5.19.4 MIDDLE EAST

- 5.19.5 LATIN AMERICA

- 5.19.6 AFRICA

6 AIRCRAFT SEALS MARKET, BY MATERIAL

- 6.1 INTRODUCTION

- 6.2 COMPOSITES

- 6.2.1 THERMAL ADAPTABILITY AND RESISTANCE TO DEFORMATION TO DRIVE DEMAND

- 6.2.2 CARBON FIBER COMPOSITES

- 6.2.3 GLASS FIBER COMPOSITES

- 6.3 POLYMERS

- 6.3.1 WIDE VERSATILITY AND ADAPTABILITY TO DRIVE DEMAND

- 6.3.2 FLUOROELASTOMER (FKM)

- 6.3.3 PERFLUOROELASTOMER (FFKM)

- 6.3.4 POLYTETRAFLUOROETHYLENE (PTFE)

- 6.3.5 ETHYLENE PROPYLENE DIENE MONOMER (EPDM)

- 6.3.6 POLYURETHANE

- 6.4 METALS

- 6.4.1 HIGH DURABILITY AND STRUCTURAL INTEGRITY TO DRIVE DEMAND

- 6.4.2 STAINLESS STEEL & ALLOYS

- 6.4.3 NICKEL & ALLOYS

- 6.4.4 OTHERS

7 AIRCRAFT SEALS MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 DYNAMIC SEALS

- 7.2.1 REDUCED FRICTION AND EXTENDED LIFE TO DRIVE DEMAND

- 7.2.2 CONTACT SEALS

- 7.2.3 CLEARANCE SEALS

- 7.3 STATIC SEALS

- 7.3.1 INCREASING DEMAND FOR LIGHTWEIGHT MATERIALS AND FLEET MAINTENANCE TO DRIVE GROWTH

- 7.3.2 O-RINGS & GASKETS

- 7.3.3 OTHER STATIC SEALS

- 7.4 OTHERS

- 7.4.1 MECHANICAL SEALS

- 7.4.2 THERMAL/FIRE SEALS

- 7.4.3 ELECTRICAL SEALS

- 7.4.4 ENVIRONMENTAL & STRUCTURAL SEALS

8 AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE

- 8.1 INTRODUCTION

- 8.2 COMMERCIAL AIRCRAFT

- 8.2.1 INCREASING DEMAND IN NARROW-BODY AIRCRAFT TO DRIVE MARKET

- 8.2.2 NARROW-BODY AIRCRAFT

- 8.2.3 WIDE-BODY AIRCRAFT

- 8.2.4 REGIONAL TRANSPORT AIRCRAFT

- 8.3 BUSINESS & GENERAL AVIATION

- 8.3.1 GROWING FOCUS ON PASSENGER COMFORT AND UTILITY SOLUTIONS TO DRIVE MARKET

- 8.3.2 BUSINESS JETS

- 8.3.3 LIGHT AIRCRAFT

- 8.3.4 ELECTRIC AIRCRAFT

- 8.3.5 COMMERCIAL HELICOPTERS

- 8.4 MILITARY AIRCRAFT

- 8.4.1 HIGH OEM AND AFTERMARKET DEMAND TO DRIVE GROWTH

- 8.4.2 FIGHTER JETS

- 8.4.3 SPECIAL MISSION AIRCRAFT

- 8.4.4 TRANSPORT AIRCRAFT

- 8.4.5 MILITARY HELICOPTERS

- 8.5 ADVANCED AIR MOBILITY

- 8.5.1 FUTURE APPLICATIONS AND INNOVATIONS IN SEALS TECHNOLOGY TO DRIVE MARKET

- 8.5.2 EVTOL AIRCRAFT

- 8.5.3 HYBRID ELECTRIC AIRCRAFT

- 8.6 UNMANNED AERIAL VEHICLES

- 8.6.1 RISING ADOPTION IN DEFENSE APPLICATIONS TO DRIVE MARKET

9 AIRCRAFT SEALS MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 ENGINE SYSTEMS

- 9.2.1 FLEET MODERNIZATION PROGRAM AND MRO TO DRIVE MARKET

- 9.3 AEROSTRUCTURES

- 9.3.1 APPLICATIONS IN STRUCTURAL INTEGRITY AND CABIN PRESSURIZATION TO DRIVE MARKET

- 9.4 AVIONICS & ELECTRICAL SYSTEMS

- 9.4.1 RISING PASSENGER TRAFFIC TO DRIVE MARKET

- 9.5 FLIGHT CONTROL & HYDRAULIC SYSTEMS

- 9.5.1 INCREASING DEMAND IN HIGH-PRESSURE APPLICATIONS TO DRIVE MARKET

- 9.6 LANDING GEAR SYSTEMS

- 9.6.1 SHOCK ABSORBANCE AND REDUCED STRESS CAPABILITIES TO DRIVE DEMAND

- 9.7 FUEL SYSTEMS

- 9.7.1 INCREASE IN GLOBAL JET FUEL CONSUMPTION TO DRIVE DEMAND

- 9.8 OTHERS

10 AIRCRAFT SEALS MARKET, BY END USE

- 10.1 INTRODUCTION

- 10.2 OEM

- 10.2.1 RISING AIRCRAFT PRODUCTION AND DELIVERIES TO DRIVE MARKET

- 10.3 AFTERMARKET

- 10.3.1 RISING REGULATORY MANDATES FOR REPLACEMENT AND MRO TO DRIVE MARKET

11 AIRCRAFT SEALS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 PESTLE ANALYSIS

- 11.2.2 US

- 11.2.2.1 Presence of major aircraft OEMs to govern market growth

- 11.2.3 CANADA

- 11.2.3.1 Domestic defense upgrades and civil aviation to drive market

- 11.3 EUROPE

- 11.3.1 PESTLE ANALYSIS

- 11.3.2 UK

- 11.3.2.1 Defense modernization program to drive market

- 11.3.3 FRANCE

- 11.3.3.1 Commitment to aviation decarbonization to drive market

- 11.3.4 GERMANY

- 11.3.4.1 Presence of major independent MRO providers to drive market

- 11.3.5 ITALY

- 11.3.5.1 Ongoing fleet modernization to drive market

- 11.3.6 SPAIN

- 11.3.6.1 Rising OEM partnerships and defense programs to drive market

- 11.3.7 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 PESTLE ANALYSIS

- 11.4.2 CHINA

- 11.4.2.1 Large-scale domestic manufacturing to boost market

- 11.4.3 INDIA

- 11.4.3.1 Increased investment in MRO to propel market

- 11.4.4 JAPAN

- 11.4.4.1 Shift toward carbon-neutral aviation to support market

- 11.4.5 AUSTRALIA

- 11.4.5.1 Increasing demand from airlines to boost market

- 11.4.6 SOUTH KOREA

- 11.4.6.1 Heavy investment in aviation infrastructure to drive market

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 MIDDLE EAST

- 11.5.1 PESTLE ANALYSIS

- 11.5.2 UAE

- 11.5.2.1 Rising traffic levels to drive market

- 11.5.3 SAUDI ARABIA

- 11.5.3.1 Large-scale aviation infrastructure projects to drive market

- 11.5.4 TURKEY

- 11.5.4.1 Expansion of aerospace industrial base to drive market

- 11.5.5 QATAR

- 11.5.5.1 Push toward aerospace industrialization to drive market

- 11.6 LATIN AMERICA

- 11.6.1 PESTLE ANALYSIS

- 11.6.2 BRAZIL

- 11.6.2.1 Presence of major aircraft OEMs to drive market

- 11.6.3 MEXICO

- 11.6.3.1 Presence of strong manufacturing hub to fuel market

- 11.6.4 REST OF LATIN AMERICA

- 11.7 AFRICA

- 11.7.1 PESTLE ANALYSIS

- 11.7.2 SOUTH AFRICA

- 11.7.2.1 Recovery of aviation industry to be beneficial for market growth

- 11.7.3 NIGERIA

- 11.7.3.1 Expansion of aviation industry to influence market growth

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 MARKET SHARE ANALYSIS, 2024

- 12.3 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS, 2021-2024

- 12.4 BRAND/PRODUCT COMPARISON

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.6 COMPANY EVALUATION MATRIX

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Material footprint

- 12.6.5.4 Aircraft type footprint

- 12.7 STARTUP/SME EVALUATION MATRIX

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING

- 12.7.5.1 List of startups/SMEs

- 12.7.5.2 Competitive benchmarking of startups/SMEs

- 12.8 COMPETITIVE SCENARIO

- 12.8.1 DEALS

- 12.8.2 OTHERS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 SKF

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 MnM view

- 13.1.1.3.1 Right to win

- 13.1.1.3.2 Strategic choices

- 13.1.1.3.3 Weaknesses and competitive threats

- 13.1.2 PARKER HANNIFIN CORP

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 TRELLEBORG SEALING SOLUTIONS

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 EATON CORPORATION PLC

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 SAINT-GOBAIN

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 SEAL SCIENCE, INC.

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.7 DP SEALS

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.8 REXNORD CORPORATION

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.9 GREENE TWEED

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.10 W. L. GORE & ASSOCIATES, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.11 PERFORMANCE SEALING INC.

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.12 BROWN AIRCRAFT SUPPLY

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.13 PRECISION POLYMER ENGINEERING LTD.

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.14 STACEM

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.15 NICHOLSONS SEALING TECHNOLOGIES LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.16 ICON AEROSPACE TECHNOLOGY

- 13.1.16.1 Business overview

- 13.1.16.2 Products offered

- 13.1.17 FREUDENBURG SEALING TECHNOLOGIES

- 13.1.17.1 Business overview

- 13.1.17.2 Products offered

- 13.1.18 HUTCHINSON

- 13.1.18.1 Business overview

- 13.1.18.2 Products offered

- 13.1.1 SKF

- 13.2 OTHER PLAYERS

- 13.2.1 PPG AEROSPACE

- 13.2.2 KIRKHILL, INC.

- 13.2.3 DUPONT

- 13.2.4 JACOTTET INDUSTRIE

- 13.2.5 TECHNETICS GROUP

- 13.2.6 NORTHWEST RUBBER EXTRUDERS, INC.

- 13.2.7 STEIN SEAL COMPANY

- 13.2.8 EMI SEALS & GASKETS

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2022-2024

- TABLE 2 AIRCRAFT SEALS MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 3 IMPORT DATA FOR HS CODE 401693-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 4 EXPORT DATA FOR HS CODE 401693-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- TABLE 5 AIRCRAFT SEALS MARKET: KEY CONFERENCES AND EVENTS , 2025-2027

- TABLE 6 TARIFF DATA FOR HS CODE 401693-COMPLIANT PRODUCTS, 2024

- TABLE 7 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 MIDDLE EAST: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USE (%)

- TABLE 12 KEY BUYING CRITERIA, BY AIRCRAFT TYPE

- TABLE 13 PATENT REGISTRATIONS

- TABLE 14 INDICATIVE PRICING OF AIRCRAFT SEALS, OEMS' PERSPECTIVE

- TABLE 15 INDICATIVE PRICING FOR AFTERMARKET, BY AIRCRAFT TYPE

- TABLE 16 COMPARISON BETWEEN BUSINESS MODELS

- TABLE 17 AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 18 AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 19 AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 20 AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 21 AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 22 AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 23 AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 24 AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 25 AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 26 AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 27 AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 28 AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 29 AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 30 AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 31 AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 32 AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 33 AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 34 AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 35 COMMERCIAL AIRCRAFT SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 36 COMMERCIAL AIRCRAFT SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 37 AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 38 AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 39 BUSINESS & GENERAL AVIATION SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 40 BUSINESS & GENERAL AVIATION SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 41 AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION TYPE, 2021-2024 (USD MILLION)

- TABLE 42 AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION TYPE, 2025-2030 (USD MILLION)

- TABLE 43 MILITARY AIRCRAFT SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 44 MILITARY AIRCRAFT SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 45 AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 46 AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 47 ADVANCED AIR MOBILITY SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 48 ADVANCED AIR MOBILITY SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 49 AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY TYPE, 2021-2024 (USD MILLION)

- TABLE 50 AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY TYPE, 2025-2030 (USD MILLION)

- TABLE 51 UNMANNED AERIAL VEHICLE SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 52 UNMANNED AERIAL VEHICLE SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 53 AIRCRAFT SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 54 AIRCRAFT SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 55 AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 56 AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 57 AIRCRAFT SEALS MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 58 AIRCRAFT SEALS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 60 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 61 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 62 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 63 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 64 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 65 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 66 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 67 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 68 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 69 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 70 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 71 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 72 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 73 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 74 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 75 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 76 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 77 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 78 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 79 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 80 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 81 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 82 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 83 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 84 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 85 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 86 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 87 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 88 NORTH AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 89 US: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 90 US: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 91 US: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 92 US: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 93 US: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 94 US: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 95 US: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 96 US: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 97 US: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 98 US: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 99 US: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 100 US: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 101 CANADA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 102 CANADA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 103 CANADA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 104 CANADA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 105 CANADA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 106 CANADA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 107 CANADA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 108 CANADA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 109 CANADA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 110 CANADA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 111 CANADA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 112 CANADA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 113 EUROPE: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 114 EUROPE: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 115 EUROPE: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 116 EUROPE: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 117 EUROPE: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 118 EUROPE: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 119 EUROPE: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 120 EUROPE: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 121 EUROPE: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 122 EUROPE: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 123 EUROPE: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 124 EUROPE: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 125 EUROPE: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 126 EUROPE: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 127 EUROPE: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 128 EUROPE: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 129 EUROPE: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 130 EUROPE: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 131 EUROPE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 132 EUROPE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 133 EUROPE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 134 EUROPE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 135 EUROPE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 136 EUROPE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 137 EUROPE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 138 EUROPE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 139 EUROPE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 140 EUROPE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 141 EUROPE: AIRCRAFT SEALS MARKET, BY APPLICATION, 2021-2024 (USD MILLION)

- TABLE 142 EUROPE: AIRCRAFT SEALS MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 143 EUROPE: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 144 EUROPE: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 145 UK: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 146 UK: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 147 UK: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 148 UK: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 149 UK: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 150 UK: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 151 UK: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 152 UK: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 153 UK: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 154 UK: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 155 UK: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 156 UK: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 157 FRANCE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 158 FRANCE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 159 FRANCE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 160 FRANCE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 161 FRANCE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 162 FRANCE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 163 FRANCE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 164 FRANCE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 165 FRANCE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 166 FRANCE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 167 FRANCE: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 168 FRANCE: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 169 GERMANY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 170 GERMANY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 171 GERMANY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 172 GERMANY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 173 GERMANY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 174 GERMANY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 175 GERMANY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 176 GERMANY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 177 GERMANY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 178 GERMANY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 179 GERMANY: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 180 GERMANY: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 181 ITALY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 182 ITALY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 183 ITALY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 184 ITALY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 185 ITALY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 186 ITALY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 187 ITALY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 188 ITALY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 189 ITALY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 190 ITALY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 191 ITALY: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 192 ITALY: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 193 SPAIN: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 194 SPAIN: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 195 SPAIN: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 196 SPAIN: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 197 SPAIN: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 198 SPAIN: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 199 SPAIN: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 200 SPAIN: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 201 SPAIN: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 202 SPAIN: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 203 SPAIN: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 204 SPAIN: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 205 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 206 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 207 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 208 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 209 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 210 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 211 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 212 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 213 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 214 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 215 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 216 REST OF EUROPE: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 217 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 218 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 219 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 220 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 221 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 222 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 223 ASIA PACIFIC :AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 224 ASIA PACIFIC :AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 225 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 226 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 227 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 228 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 229 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 230 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 231 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 232 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 233 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 234 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 235 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 236 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 237 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 238 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 239 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 240 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 241 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 242 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 243 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 244 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 245 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 246 ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 247 CHINA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 248 CHINA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 249 CHINA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 250 CHINA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 251 CHINA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 252 CHINA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 253 CHINA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 254 CHINA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 255 CHINA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 256 CHINA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 257 CHINA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 258 CHINA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 259 INDIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 260 INDIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 261 INDIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 262 INDIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 263 INDIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 264 INDIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 265 INDIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 266 INDIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 267 INDIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 268 INDIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 269 INDIA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 270 INDIA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 271 JAPAN: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 272 JAPAN: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 273 JAPAN: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 274 JAPAN: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 275 JAPAN: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 276 JAPAN: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 277 JAPAN: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 278 JAPAN: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 279 JAPAN: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 280 JAPAN: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 281 JAPAN: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 282 JAPAN: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 283 AUSTRALIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 284 AUSTRALIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 285 AUSTRALIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 286 AUSTRALIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 287 AUSTRALIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 288 AUSTRALIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 289 AUSTRALIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 290 AUSTRALIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 291 AUSTRALIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 292 AUSTRALIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 293 AUSTRALIA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 294 AUSTRALIA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 295 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 296 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 297 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 298 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 299 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 300 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 301 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 302 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 303 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 304 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 305 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 306 SOUTH KOREA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 307 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 308 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 309 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 310 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 311 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 312 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 313 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 314 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 315 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 316 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 317 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 318 REST OF ASIA PACIFIC: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 319 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 320 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 321 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 322 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 323 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 324 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 325 MIDDLE EAST :AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 326 MIDDLE EAST :AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 327 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 328 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 329 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 330 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 331 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 332 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 333 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 334 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 335 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 336 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 337 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 338 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 339 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 340 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 341 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 342 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 343 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 344 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 345 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 346 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 347 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 348 MIDDLE EAST: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 349 UAE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 350 UAE: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 351 UAE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 352 UAE: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 353 UAE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 354 UAE: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 355 UAE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 356 UAE: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 357 UAE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 358 UAE: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 359 UAE: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 360 UAE: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 361 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 362 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 363 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 364 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 365 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 366 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 367 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 368 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 369 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 370 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 371 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 372 SAUDI ARABIA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 373 TURKEY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 374 TURKEY: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 375 TURKEY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 376 TURKEY: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 377 TURKEY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 378 TURKEY: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 379 TURKEY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 380 TURKEY: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 381 TURKEY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 382 TURKEY: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 383 TURKEY: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 384 TURKEY: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 385 QATAR: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 386 QATAR: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 387 QATAR: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 388 QATAR: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 389 QATAR: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 390 QATAR: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 391 QATAR: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 392 QATAR: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 393 QATAR: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 394 QATAR: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 395 QATAR: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 396 QATAR: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 397 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 398 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 399 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 400 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 401 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 402 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 403 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 404 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 405 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 406 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 407 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 408 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 409 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 410 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 411 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 412 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 413 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 414 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 415 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 416 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 417 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 418 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 419 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 420 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 421 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 422 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 423 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 424 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 425 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 426 LATIN AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 427 BRAZIL: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 428 BRAZIL: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 429 BRAZIL: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 430 BRAZIL: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 431 BRAZIL: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 432 BRAZIL: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 433 BRAZIL: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 434 BRAZIL: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 435 BRAZIL: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 436 BRAZIL: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 437 BRAZIL: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 438 BRAZIL: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 439 MEXICO: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 440 MEXICO: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 441 MEXICO: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 442 MEXICO: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 443 MEXICO: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 444 MEXICO: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 445 MEXICO: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 446 MEXICO: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 447 MEXICO: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 448 MEXICO: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 449 MEXICO: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 450 MEXICO: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 451 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 452 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 453 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 454 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 455 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 456 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 457 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 458 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 459 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 460 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 461 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 462 REST OF LATIN AMERICA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 463 AFRICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 464 AFRICA: AIRCRAFT SEALS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 465 AFRICA: AIRCRAFT SEALS MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 466 AFRICA: AIRCRAFT SEALS MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 467 AFRICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2021-2024 (USD MILLION)

- TABLE 468 AFRICA: AIRCRAFT SEALS MARKET, BY DYNAMIC SEALS, 2025-2030 (USD MILLION)

- TABLE 469 AFRICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2021-2024 (USD MILLION)

- TABLE 470 AFRICA: AIRCRAFT SEALS MARKET, BY STATIC SEALS, 2025-2030 (USD MILLION)

- TABLE 471 AFRICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2021-2024 (USD MILLION)

- TABLE 472 AFRICA: AIRCRAFT SEALS MARKET, BY OTHER SEALS, 2025-2030 (USD MILLION)

- TABLE 473 AFRICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2021-2024 (USD MILLION)

- TABLE 474 AFRICA: AIRCRAFT SEALS MARKET, BY MATERIAL, 2025-2030 (USD MILLION)

- TABLE 475 AFRICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2021-2024 (USD MILLION)

- TABLE 476 AFRICA: AIRCRAFT SEALS MARKET, BY COMPOSITES, 2025-2030 (USD MILLION)

- TABLE 477 AFRICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2021-2024 (USD MILLION)

- TABLE 478 AFRICA: AIRCRAFT SEALS MARKET, BY POLYMERS, 2025-2030 (USD MILLION)

- TABLE 479 AFRICA: AIRCRAFT SEALS MARKET, BY METALS, 2021-2024 (USD MILLION)

- TABLE 480 AFRICA: AIRCRAFT SEALS MARKET, BY METALS, 2025-2030 (USD MILLION)

- TABLE 481 AFRICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 482 AFRICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 483 AFRICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 484 AFRICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 485 AFRICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 486 AFRICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 487 AFRICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 488 AFRICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 489 AFRICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 490 AFRICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 491 AFRICA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 492 AFRICA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 493 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 494 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 495 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 496 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 497 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 498 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 499 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 500 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 501 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 502 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 503 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 504 SOUTH AFRICA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 505 NIGERIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2021-2024 (USD MILLION)

- TABLE 506 NIGERIA: AIRCRAFT SEALS MARKET, BY AIRCRAFT TYPE, 2025-2030 (USD MILLION)

- TABLE 507 NIGERIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 508 NIGERIA: AIRCRAFT SEALS MARKET, BY COMMERCIAL AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 509 NIGERIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2021-2024 (USD MILLION)

- TABLE 510 NIGERIA: AIRCRAFT SEALS MARKET, BY BUSINESS & GENERAL AVIATION, 2025-2030 (USD MILLION)

- TABLE 511 NIGERIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2021-2024 (USD MILLION)

- TABLE 512 NIGERIA: AIRCRAFT SEALS MARKET, BY MILITARY AIRCRAFT, 2025-2030 (USD MILLION)

- TABLE 513 NIGERIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2021-2024 (USD MILLION)

- TABLE 514 NIGERIA: AIRCRAFT SEALS MARKET, BY ADVANCED AIR MOBILITY, 2025-2030 (USD MILLION)

- TABLE 515 NIGERIA: AIRCRAFT SEALS MARKET, BY END USE, 2021-2024 (USD MILLION)

- TABLE 516 NIGERIA: AIRCRAFT SEALS MARKET, BY END USE, 2025-2030 (USD MILLION)

- TABLE 517 AIRCRAFT SEALS MARKET: DEGREE OF COMPETITION

- TABLE 518 KEY PLAYER STRATEGIES/RIGHT TO WIN IN AIRCRAFT SEALS MARKET

- TABLE 519 AIRCRAFT SEALS MARKET: REGION FOOTPRINT

- TABLE 520 AIRCRAFT SEALS MARKET: MATERIAL FOOTPRINT

- TABLE 521 AIRCRAFT SEALS MARKET: AIRCRAFT TYPE FOOTPRINT

- TABLE 522 AIRCRAFT SEALS MARKET: LIST OF STARTUPS/SMES

- TABLE 523 AIRCRAFT SEALS MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 524 AIRCRAFT SEALS MARKET: DEALS, JANUARY 2021-AUGUST 2025

- TABLE 525 AIRCRAFT SEALS MARKET: OTHERS, JANUARY 2021-AUGUST 2025

- TABLE 526 SKF: COMPANY OVERVIEW

- TABLE 527 SKF: PRODUCTS OFFERED

- TABLE 528 PARKER HANNIFIN CORP: COMPANY OVERVIEW

- TABLE 529 PARKER HANNIFIN CORP: PRODUCTS OFFERED

- TABLE 530 PARKER HANNIFIN CORP: DEALS

- TABLE 531 TRELLEBORG SEALING SOLUTIONS: COMPANY OVERVIEW

- TABLE 532 TRELLEBORG SEALING SOLUTIONS: PRODUCTS OFFERED

- TABLE 533 TRELLEBORG SEALING SOLUTIONS: DEALS

- TABLE 534 EATON CORPORATION PLC: COMPANY OVERVIEW

- TABLE 535 EATON CORPORATION PLC : PRODUCTS OFFERED

- TABLE 536 EATON CORPORATION PLC: DEALS

- TABLE 537 SAINT-GOBAIN: COMPANY OVERVIEW

- TABLE 538 SAINT-GOBAIN: PRODUCTS OFFERED

- TABLE 539 SAINT-GOBAIN: DEALS

- TABLE 540 SEAL SCIENCE, INC.: COMPANY OVERVIEW

- TABLE 541 SEAL SCIENCE, INC.: PRODUCTS OFFERED

- TABLE 542 DP SEALS: COMPANY OVERVIEW

- TABLE 543 DP SEALS: PRODUCTS OFFERED

- TABLE 544 DP SEALS: DEALS

- TABLE 545 REXNORD CORPORATION: COMPANY OVERVIEW

- TABLE 546 REXNORD CORPORATION: PRODUCTS OFFERED

- TABLE 547 GREENE TWEED: COMPANY OVERVIEW

- TABLE 548 GREENE TWEED: PRODUCTS OFFERED

- TABLE 549 W. L. GORE & ASSOCIATES, INC.: COMPANY OVERVIEW

- TABLE 550 W. L. GORE & ASSOCIATES, INC.: PRODUCTS OFFERED

- TABLE 551 PERFORMANCE SEALING INC.: COMPANY OVERVIEW

- TABLE 552 PERFORMANCE SEALING INC.: PRODUCTS OFFERED

- TABLE 553 BROWN AIRCRAFT SUPPLY: COMPANY OVERVIEW

- TABLE 554 BROWN AIRCRAFT SUPPLY: PRODUCTS OFFERED

- TABLE 555 PRECISION POLYMER ENGINEERING LTD.: COMPANY OVERVIEW

- TABLE 556 PRECISION POLYMER ENGINEERING LTD.: PRODUCTS OFFERED

- TABLE 557 STACEM: COMPANY OVERVIEW

- TABLE 558 STACEM: PRODUCTS OFFERED

- TABLE 559 NICHOLSONS SEALING TECHNOLOGIES LTD.: COMPANY OVERVIEW

- TABLE 560 NICHOLSONS SEALING TECHNOLOGIES LTD.: PRODUCTS OFFERED

- TABLE 561 ICON AEROSPACE TECHNOLOGY: COMPANY OVERVIEW

- TABLE 562 ICON AEROSPACE TECHNOLOGY: PRODUCTS OFFERED

- TABLE 563 FREUDENBURG SEALING TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 564 FREUDENBURG SEALING TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 565 HUTCHINSON: COMPANY OVERVIEW

- TABLE 566 HUTCHINSON: PRODUCTS OFFERED

List of Figures

- FIGURE 1 REPORT PROCESS FLOW

- FIGURE 2 AIRCRAFT SEALS MARKET: RESEARCH DESIGN

- FIGURE 3 KEY PRIMARY INSIGHTS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 6 AIRCRAFT SEALS MARKET: DATA TRIANGULATION

- FIGURE 7 COMMERCIAL AIRCRAFT TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 8 DYNAMIC SEALS SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 9 OEM SEGMENT TO ACQUIRE LARGER SHARE THAN AFTERMARKET SEGMENT IN 2030

- FIGURE 10 ASIA PACIFIC TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 11 RISING GLOBAL AIRCRAFT FLEET SIZE TO DRIVE MARKET

- FIGURE 12 CONTACT SEALS TO HOLD LARGER SHARE THAN CLEARANCE SEALS IN 2025

- FIGURE 13 FIGHTER JETS TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 14 CARBON FIBER COMPOSITES TO BE DOMINANT SEGMENT DURING FORECAST PERIOD

- FIGURE 15 NARROW-BODY AIRCRAFT SEGMENT TO BE PREVALENT DURING FORECAST PERIOD

- FIGURE 16 AIRCRAFT SEALS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 17 AIRCRAFT SEALS MARKET ECOSYSTEM

- FIGURE 18 IMPORT DATA FOR HS CODE 401693-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 19 EXPORT DATA FOR HS CODE 401693-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD THOUSAND)

- FIGURE 20 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY END USE

- FIGURE 21 KEY BUYING CRITERIA, BY AIRCRAFT TYPE

- FIGURE 22 PATENT ANALYSIS, 2014-2024

- FIGURE 23 PRIVATE EQUITY/VENTURE CAPITAL TRENDS, 2019-2024

- FIGURE 24 Y-O-Y FUNDING TRENDS ACROSS CIVIL AND MILITARY AIRCRAFT, 2019-2024

- FIGURE 25 Y-O-Y FUNDING TRENDS ACROSS UAV AND AAM, 2019-2024

- FIGURE 26 BREAKDOWN OF TOTAL COST OF OWNERSHIP

- FIGURE 27 TECHNOLOGY ROADMAP OF AIRCRAFT SEALS MARKET

- FIGURE 28 EVOLUTION OF TECHNOLOGIES IN AIRCRAFT SEALS MARKET

- FIGURE 29 BUSINESS MODELS IN AIRCRAFT SEALS MARKET

- FIGURE 30 ADOPTION OF AI IN AVIATION

- FIGURE 31 ADOPTION OF AI IN COMMERCIAL AVIATION BY TOP COUNTRIES

- FIGURE 32 IMPACT OF AI ON AIRCRAFT SEALS MARKET

- FIGURE 34 DYNAMIC SEALS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 35 COMMERCIAL AIRCRAFT SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2025

- FIGURE 36 ENGINE SYSTEMS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2025

- FIGURE 37 AFTERMARKET TO HAVE LEADING MARKET SHARE IN 2025

- FIGURE 38 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- FIGURE 39 NORTH AMERICA: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 40 EUROPE: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 42 MIDDLE EAST: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 43 LATIN AMERICA: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 44 AFRICA: AIRCRAFT SEALS MARKET SNAPSHOT

- FIGURE 45 AIRCRAFT SEALS MARKET SHARE OF KEY PLAYERS, 2024

- FIGURE 46 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS, 2021-2024

- FIGURE 47 BRAND/PRODUCT COMPARISON

- FIGURE 48 FINANCIAL METRICS (EV/EBITDA), 2025

- FIGURE 49 COMPANY VALUATION (USD BILLION), 2025

- FIGURE 50 AIRCRAFT SEALS MARKET: COMPANY EVALUATION MATRIX, 2024

- FIGURE 51 AIRCRAFT SEALS MARKET: COMPANY FOOTPRINT

- FIGURE 52 AIRCRAFT SEALS MARKET: STARTUP/SME EVALUATION MATRIX, 2024

- FIGURE 53 SKF: COMPANY SNAPSHOT

- FIGURE 54 PARKER HANNIFIN CORP: COMPANY SNAPSHOT

- FIGURE 55 TRELLEBORG SEALING SOLUTIONS: COMPANY SNAPSHOT

- FIGURE 56 EATON CORPORATION PLC: COMPANY SNAPSHOT

- FIGURE 57 SAINT-GOBAIN: COMPANY SNAPSHOT

- FIGURE 58 REXNORD CORPORATION: COMPANY SNAPSHOT