PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1883942

PUBLISHER: MarketsandMarkets | PRODUCT CODE: 1883942

Spare Parts Management (SPM) Market by Solutions (Spare Part Tracking & Automation, Inventory Management, Procurement & Order Management, Reporting & Analytics, Planning & Forecasting), Spare Part Management Services, Type - Global Forecast to 2030

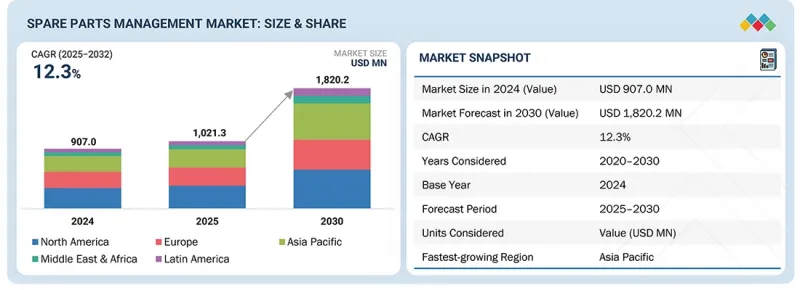

The spare parts management market is projected to expand at a CAGR of 12.3%, reaching USD 1,820.2 million by 2030 from an estimated USD 1,021.3 million in 2025.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD Million |

| Segments | Offering, Type, Deployment Mode, Organization Size, Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The market is expanding steadily, driven by escalating unplanned downtime asset-hour costs, rising demands for precise service planning, and the growing dependence on the aftermarket as a profit center for manufacturers. As organizations face increasing financial exposure due to equipment failures, they are adopting intelligent planning platforms that enhance parts availability, expedite replenishment, and minimize service interruptions across their distributed operations.

AI-driven demand forecasting enhances fill-rate precision by interpreting asset health signals, usage variability, and repair histories, which improves stocking accuracy and service-level performance. The aftermarket's expanding role in margin growth is also increasing demand for unified capabilities that connect planning, pricing, warranty, and repair-return workflows. The market's expansion is restrained by proprietary lock-ins that limit data access across OEM and service ecosystems, as well as by inaccurate and inconsistent parts data that reduces forecasting reliability and inventory alignment. Weak taxonomy structures and non-standardized classification frameworks further hinder operational efficiency by restricting interoperability and slowing down harmonization across global networks. Despite these restraints, investment in data quality, advanced analytics, and service supply chain integration continues to underscore the critical role of modern spare parts management systems in enhancing uptime and bolstering aftermarket profitability.

"By type, the standalone SPM software segment is projected to witness a higher growth rate than the integrated SPM software segment during the forecast period"

Standalone spare parts management (SPM) software delivers purpose-built, domain-focused control over spare parts operations, giving enterprises greater flexibility and speed compared to monolithic enterprise suites. These platforms utilize AI-driven demand modeling, digital twin integration, and advanced replenishment logic to enable organizations to manage multi-tier spare parts inventories independently. In May 2024, Baxter Planning enhanced its BaxterPredict standalone platform with automated service parts planning and integrated sustainability metrics, enabling clients to cut parts excess by up to 25% and improve planning accuracy by 20%. In October 2024, Facilio launched a standalone Connected Maintenance Hub designed to unify facility maintenance and spare parts visibility, providing enterprises with real-time part utilization analytics and automated replacement scheduling. These developments highlight the growing maturity and adoption of standalone solutions purpose-engineered for modern service ecosystems. Standalone SPM solutions present a strategic advantage for organizations seeking independence from complex enterprise IT infrastructures. By integrating predictive intelligence, modular scalability, and mobile accessibility, these platforms allow faster deployment and measurable impact on uptime and cost efficiency. Vendors that design configurable, cloud-native systems with interoperability via APIs and embedded analytics will shape the next phase of digital spare parts operations, enabling customers to operate with agility, precision, and control.

"By organization size, the large enterprises segment is estimated to lead the market during the forecast period"

Large enterprises represent the most mature segment of the spare parts management (SPM) market, driven by complex global supply chains, multi-site maintenance operations, and high-value asset bases. These organizations rely on deeply integrated, enterprise-grade SPM platforms that synchronize procurement, logistics, and service operations under unified digital control. In October 2024, Limble CMMS announced its integration with SAP S/4HANA, allowing real-time synchronization of spare parts inventory, vendor data, and purchase orders within SAP's enterprise ecosystem. This advancement demonstrates how large organizations are prioritizing interoperability and data cohesion across systems to ensure continuous parts availability and operational efficiency. For large enterprises, SPM platforms serve as strategic enablers of uptime, working capital optimization, and service reliability across geographically dispersed networks. Advanced integrations, AI-enabled forecasting, and unified analytics dashboards allow decision-makers to align maintenance strategies with global inventory intelligence. Vendors focusing on this segment should emphasize scalable architectures, multi-region support, and compliance-ready reporting, ensuring seamless coordination across procurement, warehousing, and service delivery functions. As digital transformation reshapes asset management, large enterprises will continue to drive adoption of SPM platforms that combine predictive intelligence with enterprise-level process orchestration to achieve sustainable performance outcomes.

"North America is estimated to lead the market due to its strong adoption of AI-enabled planning platforms, mature aftermarket service ecosystems, and high investment in uptime-focused inventory optimization across asset-intensive industries, while Asia Pacific is projected to be the fastest-growing region, driven by rapid industrial digitalization, expanding manufacturing bases, and increasing reliance on service-led revenue models that require advanced, data-driven parts lifecycle management"

The spare parts management (SPM) market in North America is being shaped by strong digital infrastructure, resilient logistics networks, and evolving trade frameworks that promote regional sourcing and supply chain integration. According to GSMA (2025), around 60% of mobile connections in the region are now 5G, while nearly 320 million people use mobile internet, creating an environment ideal for IoT-based monitoring, predictive maintenance, and connected field service operations. This widespread connectivity allows technicians and OEMs to access real-time diagnostics, e-parts catalogs, and asset telemetry across large service networks. At the same time, the GEP Volatility Index for North America improved to -0.24 (June 2025), signaling a gradual recovery in supply chain activity. However, manufacturers continue to face delivery delays tied to trade and tariff adjustments, prompting the need for safety-stock optimization and automated lead-time management in SPM systems. Logistics and transport indicators further highlight the region's readiness for data-driven parts management. Rail volumes across North America grew 2.4% year-to-date through 2025 (Association of American Railroads), improving inland parts repositioning and warehouse connectivity. Port operations have largely stabilized, according to the World Bank's CPPI 2024, which has reduced variability in inbound lead times. Meanwhile, trade policies such as the USMCA's 75% regional content rule for vehicles and parts (Trade.gov) are pushing manufacturers to localize sourcing and strengthen regional inventory pools. Together, these dynamics, including high connectivity, nearshoring, and supply-chain modernization, are reinforcing North America's shift toward predictive, digitally coordinated spare parts management.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the spare parts management market.

- By Company: Tier I - 30%, Tier II - 40%, and Tier III - 30%

- By Designation: C-Level Executives - 50%, D-Level Executives -35%, and others - 15%

- By Region: North America - 50%, Europe - 30%, Asia Pacific - 15%, and Rest of the World - 5%

The report includes a study of key players offering spare parts management products. It profiles major market players, which include PTC (US), Syncron (Sweden), Fiix (Canada), Dassault Systemes (France), IBM (US), Oracle (US), Baxter Planning (US), IFS (Sweden), Tavant (US), Cryotos (India), eMaint (US), Erpag (US), Megaventory (US), Upkeep (US), Infraon (US), ValueApex (China), MPulse Software (US), AntMyErp (India), Limble CMMS (US), Fleataable (Canada), Verusen (Georgia), Mastek (India), Raseed (India), PartsCloud (Germany), Spartech (Germany), Partful (England), Facilio (US), and ToolsGroup (US).

Research Coverage

This research report categorizes the spare parts management market based on offering (solutions [planning & forecasting, procurement & order management, inventory management, spare parts tracking & automation, reporting & analytics, others] and professional services [training & consultation, integration & implementation, support & maintenance]), type (standalone SPM software, integration SPM software), deployment mode (on-premises, cloud), organization size (large enterprises, SMEs), vertical (manufacturing, transportation & logistics, construction & real estate, healthcare & life sciences, energy & utilities, IT & telecom, oil & gas, other verticals [BFSI, retail & consumer goods]), and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The report's scope covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the spare parts management market. A detailed analysis of key industry players was conducted to provide insights into their business overview, solutions, and services, as well as key strategies, contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the spare parts management market. This report also covers the competitive analysis of upcoming startups in the spare parts management market ecosystem.

Reason to Buy this Report

The report would provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall spare parts management market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. It also helps stakeholders understand the market's pulse and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Escalating unplanned downtime asset-hour costs, improvement in fill-rate precision with AI demand forecasting, growing dependence on aftermarket as a profit center), restraints (Proprietary lock-ins and restricted data access, inaccurate and inconsistent spare parts data, weak parts taxonomy and inconsistent classification standards), opportunities (Real-time IoT telemetry for inventory visibility, shift toward servitization and uptime-based contracts, expanding maintenance intensity across asset-heavy industries), and challenges (Managing long-tail, low-turn spare parts complexity, supplier lead-time volatility impacting fill rates).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the spare parts management market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the spare parts management market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the spare parts management market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as PTC (US), Syncron (Sweden), Fiix (Canada), Dassault Systemes (France), IBM (US), Oracle (US), Baxter Planning (US), IFS (Sweden), Tavant (US), Cryotos (India), eMaint (US), Erpag (US), Megaventory (US), Upkeep (US), Infraon (US), ValueApex (China), MPulse Software (US), AntMyErp (India), Limble CMMS (US), Fleataable (Canada), Verusen (Georgia), Mastek (India), Raseed (India), PartsCloud (Germany), Spartech (Germany), Partful (England), Facilio (US), and ToolsGroup (US). The report also helps stakeholders understand the spare parts management market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary interviews

- 2.1.2.3 Key industry insights

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.3 DATA TRIANGULATION

- 2.4 FACTOR ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 3.2 KEY MARKET PARTICIPANTS: INSIGHTS AND STRATEGIC DEVELOPMENTS

- 3.3 DISRUPTIVE TRENDS SHAPING MARKET

- 3.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 3.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SPARE PARTS MANAGEMENT MARKET

- 4.2 SPARE PARTS MANAGEMENT MARKET, BY OFFERING

- 4.3 SPARE PARTS MANAGEMENT MARKET, BY TYPE

- 4.4 SPARE PARTS MANAGEMENT MARKET, BY VERTICAL

- 4.5 SPARE PARTS MANAGEMENT MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Escalating unplanned downtime asset-hour costs

- 5.2.1.2 Improvement in fill-rate precision with AI demand forecasting

- 5.2.1.3 Growing dependence on aftermarket as profit center

- 5.2.2 RESTRAINTS

- 5.2.2.1 Proprietary lock-ins and restricted data access

- 5.2.2.2 Inaccurate and inconsistent spare parts data

- 5.2.2.3 Weak parts taxonomy and inconsistent classification standards

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Real-time IoT telemetry for inventory visibility

- 5.2.3.2 Shift toward servitization and uptime-based contracts

- 5.2.3.3 Expanding maintenance intensity across asset-heavy industries

- 5.2.4 CHALLENGES

- 5.2.4.1 Managing long-tail, low-turn spare parts complexity

- 5.2.4.2 Supplier lead-time volatility impacting fill rates

- 5.2.1 DRIVERS

- 5.3 UNMET NEEDS AND WHITE SPACES

- 5.3.1 UNMET NEEDS IN SPARE PARTS MANAGEMENT MARKET

- 5.3.2 WHITE SPACE OPPORTUNITIES

- 5.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 5.4.1 INTERCONNECTED MARKETS

- 5.4.2 CROSS-SECTOR OPPORTUNITIES

- 5.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 5.5.1 EMERGING BUSINESS MODELS

- 5.5.1.1 Spare parts management business models

- 5.5.2 ECOSYSTEM SHIFTS

- 5.5.1 EMERGING BUSINESS MODELS

- 5.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 5.6.1 KEY MOVES AND STRATEGIC FOCUS

6 INDUSTRY TRENDS

- 6.1 PORTER'S FIVE FORCES ANALYSIS

- 6.1.1 THREAT OF NEW ENTRANTS

- 6.1.2 THREAT OF SUBSTITUTES

- 6.1.3 BARGAINING POWER OF SUPPLIERS

- 6.1.4 BARGAINING POWER OF BUYERS

- 6.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.2 MACROECONOMIC INDICATORS

- 6.2.1 INTRODUCTION

- 6.2.2 GDP TRENDS & FORECASTS

- 6.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 6.3 SUPPLY CHAIN ANALYSIS

- 6.3.1 TECHNOLOGY ENABLERS & PLATFORM PROVIDERS

- 6.3.2 SOLUTION INTEGRATORS & SERVICE PARTNERS

- 6.3.3 CHANNEL PARTNERS & MANAGED SERVICE PROVIDERS

- 6.3.4 VERTICALS

- 6.4 ECOSYSTEM ANALYSIS

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE OF SPARE PARTS MANAGEMENT, BY REGION, 2024-2025

- 6.5.1.1 Average selling price of spare parts management, by offering, 2024-2025

- 6.5.1 AVERAGE SELLING PRICE OF SPARE PARTS MANAGEMENT, BY REGION, 2024-2025

- 6.6 KEY CONFERENCES AND EVENTS, 2025-2026

- 6.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.8 INVESTMENT AND FUNDING SCENARIO

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 EMBRAER SUCCESSFULLY OPTIMIZES SPARE PARTS PLANNING WITH SERVIGISTICS AND SAVES MORE THAN USD 50 MILLION

- 6.9.2 SYNCRON ENABLES AL MASAOOD AUTOMOBILES TO ENHANCE INVENTORY EFFICIENCY AND SERVICE PERFORMANCE

- 6.9.3 EMAINT STREAMLINES SPARE PARTS MANAGEMENT FOR CERAPEDICS THROUGH CMMS INTEGRATION

- 6.9.4 TOOLSGROUP ENABLES LENNOX TO OPTIMIZE SERVICE PARTS PLANNING AND REDUCE STOCKOUTS

- 6.9.5 TRIANGLE TUBE ENHANCES AFTER-SALES EXPERIENCE THROUGH 3D DIGITAL TRANSFORMATION WITH PARTFUL

- 6.10 IMPACT OF 2025 US TARIFF - SPARE PARTS MANAGEMENT MARKET

- 6.10.1 INTRODUCTION

- 6.10.2 KEY TARIFF RATES

- 6.10.3 PRICE IMPACT ANALYSIS

- 6.10.4 IMPACT ON COUNTRY/REGION

- 6.10.4.1 US

- 6.10.4.2 Europe

- 6.10.4.3 Asia Pacific

- 6.10.5 IMPACT ON VERTICALS

- 6.10.5.1 Manufacturing

- 6.10.5.2 Transportation & logistics

- 6.10.5.3 Construction & real estate

- 6.10.5.4 Healthcare & life sciences

- 6.10.5.5 Energy & utilities

- 6.10.5.6 IT & telecom

- 6.10.5.7 Oil & gas

7 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 7.1 TECHNOLOGY ANALYSIS

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.1.1.1 Predictive analytics and AI-driven demand forecasting

- 7.1.1.2 Digital twin and asset lifecycle intelligence

- 7.1.1.3 Cloud-native spare parts management platforms

- 7.1.2 COMPLEMENTARY TECHNOLOGIES

- 7.1.2.1 IoT-enabled asset tracking and condition monitoring

- 7.1.2.2 Computer vision and 3D recognition for parts identification

- 7.1.2.3 Blockchain-based parts traceability and warranty management

- 7.1.3 ADJACENT TECHNOLOGIES

- 7.1.3.1 Augmented reality (AR) for service and training applications

- 7.1.3.2 Low-code / no-code workflow automation platforms

- 7.1.3.3 Knowledge graphs and semantic search

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.2 TECHNOLOGY/PRODUCT ROADMAP

- 7.2.1 SHORT-TERM (2025-2027) | CLOUD CONSOLIDATION & DATA UNIFICATION

- 7.2.2 MID-TERM (2027-2030) | PREDICTIVE INTELLIGENCE & SERVICE AUTOMATION

- 7.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, CONNECTED & CIRCULAR SERVICE PLATFORMS

- 7.3 PATENT ANALYSIS

- 7.4 FUTURE APPLICATIONS

- 7.4.1 AI-DRIVEN PREDICTIVE PARTS ORCHESTRATION (DIGITAL-TWIN INTEGRATED)

- 7.4.2 AUTONOMOUS SMART CONTRACTS FOR PARTS (BLOCKCHAIN / PART-PASSPORT)

- 7.4.3 ON-DEMAND DIGITAL INVENTORY WITH ADDITIVE MANUFACTURING INTEGRATION

- 7.4.4 COGNITIVE FIELD SERVICE AND AR-GUIDED PARTS FULFILMENT

- 7.4.5 CIRCULAR AND SUSTAINABILITY-LINKED PARTS LIFECYCLE MANAGEMENT

- 7.5 IMPACT OF AI/GENERATIVE AI ON SPARE PARTS MANAGEMENT MARKET

- 7.5.1 TOP USE CASES AND MARKET POTENTIAL

- 7.5.2 BEST PRACTICES IN SPARE PARTS MANAGEMENT

- 7.5.3 CASE STUDY OF AI IMPLEMENTATION IN SPARE PARTS MANAGEMENT MARKET

- 7.5.3.1 DMG MORI and Syncron drive AI-enabled efficiency and forecast accuracy in global spare parts management

- 7.5.4 INTERCONNECTED ADJACENCY ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.5.5 CLIENT READINESS TO ADOPT GENERATIVE AI IN SPARE PARTS MANAGEMENT MARKET

- 7.5.6 PARTSCLOUD: PARTSOS PLANNING

- 7.5.7 FIIX: PARTS & INVENTORY MANAGEMENT SOFTWARE

8 REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS, BY REGION

- 8.1.2.1 North America

- 8.1.2.2 Europe

- 8.1.2.3 Asia Pacific

- 8.1.2.4 Middle East & South Africa

- 8.1.2.5 Latin America

9 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 9.1 DECISION-MAKING PROCESS

- 9.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 9.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 9.2.2 BUYING CRITERIA

- 9.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 9.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 9.5 MARKET PROFITABILITY

- 9.5.1 REVENUE POTENTIAL

- 9.5.2 COST DYNAMICS

- 9.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

10 SPARE PARTS MANAGEMENT MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.1.1 OFFERING: SPARE PARTS MANAGEMENT MARKET DRIVERS

- 10.2 SOLUTIONS

- 10.2.1 PLANNING & FORECASTING

- 10.2.1.1 Driving predictive spare parts readiness through AI-led planning and intelligent demand forecasting

- 10.2.2 PROCUREMENT & ORDER MANAGEMENT

- 10.2.2.1 Digitizing spare-parts procurement to enhance supplier visibility, accelerate orders, and reduce operational latency

- 10.2.3 INVENTORY MANAGEMENT

- 10.2.3.1 Transforming spare parts inventory into predictive, self-optimizing network that drives uptime and agility

- 10.2.4 SPARE PARTS TRACKING & AUTOMATION

- 10.2.4.1 Enabling autonomous spare part tracking and automation to drive precision, speed, and service continuity

- 10.2.5 REPORTING & ANALYTICS

- 10.2.5.1 Leveraging analytics-driven dashboards and reports to transform spare parts data into actionable intelligence

- 10.2.6 OTHERS

- 10.2.1 PLANNING & FORECASTING

- 10.3 PROFESSIONAL SERVICES

- 10.3.1 TRAINING & CONSULTATION

- 10.3.1.1 Enhancing workforce capability through analytics-driven training and consultative programs

- 10.3.2 INTEGRATION & IMPLEMENTATION

- 10.3.2.1 Enabling seamless digital deployment and process alignment through precise, domain-led integration and implementation expertise

- 10.3.3 SUPPORT & MAINTENANCE

- 10.3.3.1 Delivering intelligent, proactive support and maintenance services to ensure uptime, adaptability, and long-term system resilience

- 10.3.1 TRAINING & CONSULTATION

11 SPARE PARTS MANAGEMENT MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.1.1 TYPE: SPARE PARTS MANAGEMENT MARKET DRIVERS

- 11.2 STANDALONE SPM SOFTWARE

- 11.2.1 ACHIEVING PREDICTIVE ACCURACY, OPERATIONAL INDEPENDENCE, AND MEASURABLE EFFICIENCY GAINS IN SPARE PARTS MANAGEMENT

- 11.3 INTEGRATED SPM SOFTWARE

- 11.3.1 UNIFYING SPARE PARTS, MAINTENANCE, AND SUPPLY CHAIN SYSTEMS TO ACHIEVE CONTINUOUS VISIBILITY, PREDICTIVE CONTROL, AND OPERATIONAL RESILIENCE

12 SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE

- 12.1 INTRODUCTION

- 12.1.1 DEPLOYMENT MODE: SPARE PARTS MANAGEMENT MARKET DRIVERS

- 12.2 ON-PREMISES

- 12.2.1 PROVIDING DATA SOVEREIGNTY, LOW LATENCY, AND CERTIFIED LOCAL SUPPORT

- 12.3 CLOUD

- 12.3.1 UNIFYING GLOBAL SPARE PARTS OPERATIONS, ENHANCING PREDICTIVE INTELLIGENCE, AND ACHIEVING AGILE, DATA-DRIVEN SERVICE EXCELLENCE

13 SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE

- 13.1 INTRODUCTION

- 13.1.1 ORGANIZATION SIZE: SPARE PARTS MANAGEMENT MARKET DRIVERS

- 13.2 LARGE ENTERPRISES

- 13.2.1 UNIFYING PARTS INTELLIGENCE, AUTOMATION, AND CROSS-SITE COLLABORATION TO ENHANCE UPTIME AND EFFICIENCY

- 13.3 SMES

- 13.3.1 COMBINING AUTOMATION, TRACEABILITY, AND MOBILE USABILITY TO DRIVE OPERATIONAL DISCIPLINE AND UPTIME

14 SPARE PARTS MANAGEMENT MARKET, BY VERTICAL

- 14.1 INTRODUCTION

- 14.1.1 VERTICAL: SPARE PARTS MANAGEMENT MARKET DRIVERS

- 14.2 MANUFACTURING

- 14.2.1 DELIVERING MANUFACTURING-CENTRIC SPM SOLUTIONS TO MAXIMIZE UPTIME AND OPERATIONAL EFFICIENCY

- 14.3 TRANSPORTATION & LOGISTICS

- 14.3.1 DEPLOYING TRANSPORT-GRADE SPM TO MAXIMIZE FLEET UPTIME AND REDUCE REPAIR CYCLE TIME

- 14.4 CONSTRUCTION & REAL ESTATE

- 14.4.1 PROVIDING CONNECTED SPM SOLUTIONS FOR PROPERTY PORTFOLIOS TO PROTECT UPTIME AND PROJECT DELIVERY

- 14.5 HEALTHCARE & LIFE SCIENCES

- 14.5.1 DEVELOPING COMPLIANT, PREDICTIVE SPM PLATFORMS TO ENSURE CONTINUOUS EQUIPMENT READINESS AND UNCOMPROMISED PATIENT SAFETY

- 14.6 ENERGY & UTILITIES

- 14.6.1 DELIVERING ENERGY-SPECIFIC SPM SOLUTIONS TO ENHANCE GRID RELIABILITY AND OPERATIONAL RESILIENCE

- 14.7 IT & TELECOM

- 14.7.1 IMPLEMENTING CLOUD-ENABLED, FIELD-FIRST SPM TO MINIMIZE TRUCK ROLLS AND ACCELERATE REPAIRS

- 14.8 OIL & GAS

- 14.8.1 CREATING OIL AND GAS-OPTIMIZED SPM SOLUTIONS TO ENSURE RELIABILITY AND UNINTERRUPTED PRODUCTION

- 14.9 OTHER VERTICALS

15 SPARE PARTS MANAGEMENT MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Rising downtime costs and aftermarket scale to drive adoption of data-driven spare parts management

- 15.2.2 CANADA

- 15.2.2.1 High inventories, workforce gaps, and digital adoption to accelerate shift toward smarter spare parts management

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 UK

- 15.3.1.1 Rising supply delays, ageing vehicle fleet, and AI adoption to drive next phase of spare parts management growth

- 15.3.2 GERMANY

- 15.3.2.1 Rising service workloads, ageing vehicle fleet, and persistent supply delays to drive market

- 15.3.3 FRANCE

- 15.3.3.1 Persistent supply strain, rising costs, and expanding digital readiness to accelerate smart spare parts management adoption

- 15.3.4 ITALY

- 15.3.4.1 Digital maturity, automation, and aging assets to reshape spare parts management landscape

- 15.3.5 REST OF EUROPE

- 15.3.1 UK

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Industrial digitalization, expanding asset base, and renewal policies to boost market

- 15.4.2 INDIA

- 15.4.2.1 Nationwide connectivity, expanding vehicle base, and policy modernization to fuel market

- 15.4.3 JAPAN

- 15.4.3.1 Inventory build-up, supply delays, and ageing assets to drive demand for data-driven spare parts management

- 15.4.4 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 GCC COUNTRIES

- 15.5.1.1 Saudi Arabia

- 15.5.1.1.1 Industrial growth, logistics modernization, and AI integration to drive market

- 15.5.1.2 UAE

- 15.5.1.2.1 Industrial localization, 5G integration, and fleet growth to propel market

- 15.5.1.3 Other GCC countries

- 15.5.1.1 Saudi Arabia

- 15.5.2 SOUTH AFRICA

- 15.5.2.1 Growing focus on reliability, digital maintenance tools, and fleet modernization to strengthen demand for spare parts management

- 15.5.3 REST OF MIDDLE EAST & AFRICA

- 15.5.1 GCC COUNTRIES

- 15.6 LATIN AMERICA

- 15.6.1 BRAZIL

- 15.6.1.1 Digital connectivity, industrial modernization, and aging assets to drive predictive spare parts management adoption

- 15.6.2 MEXICO

- 15.6.2.1 Digitalization, supply chain realignment, and fleet aging to propel demand for predictive spare parts management

- 15.6.3 REST OF LATIN AMERICA

- 15.6.1 BRAZIL

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.2.1 COMPETITIVE STRATEGIES

- 16.3 REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS

- 16.5 PRODUCT COMPARISON

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 16.6.5.1 Company footprint

- 16.6.5.2 Region footprint

- 16.6.5.3 Offering footprint

- 16.6.5.4 Type footprint

- 16.6.5.5 Deployment mode footprint

- 16.6.5.6 Organization size footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPANY VALUATION AND FINANCIAL METRICS

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 INTRODUCTION

- 17.2 MAJOR PLAYERS

- 17.2.1 SYNCRON

- 17.2.1.1 Business overview

- 17.2.1.2 Products/Solutions/Services offered

- 17.2.1.3 Recent developments

- 17.2.1.3.1 Product launches and enhancements

- 17.2.1.3.2 Deals

- 17.2.1.4 MnM view

- 17.2.1.4.1 Right to win

- 17.2.1.4.2 Strategic choices

- 17.2.1.4.3 Weaknesses and competitive threats

- 17.2.2 IFS

- 17.2.2.1 Business overview

- 17.2.2.2 Products/Solutions/Services offered

- 17.2.2.3 Recent developments

- 17.2.2.3.1 Deals

- 17.2.2.4 MnM view

- 17.2.2.4.1 Right to win

- 17.2.2.4.2 Strategic choices

- 17.2.2.4.3 Weaknesses and competitive threats

- 17.2.3 BAXTER PLANNING

- 17.2.3.1 Business overview

- 17.2.3.2 Products/Solutions/Services offered

- 17.2.3.3 Recent developments

- 17.2.3.3.1 Product launches and enhancements

- 17.2.3.3.2 Deals

- 17.2.3.4 MnM view

- 17.2.3.4.1 Right to win

- 17.2.3.4.2 Strategic choices

- 17.2.3.4.3 Weaknesses and competitive threats

- 17.2.4 PTC

- 17.2.4.1 Business overview

- 17.2.4.2 Products/Solutions/Services offered

- 17.2.4.3 Recent developments

- 17.2.4.3.1 Product launches and enhancements

- 17.2.4.3.2 Deals

- 17.2.4.4 MnM view

- 17.2.4.4.1 Right to win

- 17.2.4.4.2 Strategic choices

- 17.2.4.4.3 Weaknesses and competitive threats

- 17.2.5 FIIX

- 17.2.5.1 Business overview

- 17.2.5.2 Products/Solutions/Services offered

- 17.2.5.3 Recent developments

- 17.2.5.3.1 Deals

- 17.2.5.4 MnM view

- 17.2.5.4.1 Right to win

- 17.2.5.4.2 Strategic choices

- 17.2.5.4.3 Weaknesses and competitive threats

- 17.2.6 SAP

- 17.2.6.1 Business overview

- 17.2.6.2 Products/Solutions/Services offered

- 17.2.6.3 Recent developments

- 17.2.6.3.1 Product launches and enhancements

- 17.2.6.3.2 Deals

- 17.2.7 IBM

- 17.2.7.1 Business overview

- 17.2.7.2 Products/Solutions/Services offered

- 17.2.7.3 Recent developments

- 17.2.7.3.1 Product launches and enhancements

- 17.2.8 ORACLE

- 17.2.8.1 Business overview

- 17.2.8.2 Products/Solutions/Services offered

- 17.2.8.3 Recent developments

- 17.2.8.3.1 Product launches and enhancements

- 17.2.8.3.2 Deals

- 17.2.9 TAVANT

- 17.2.9.1 Business overview

- 17.2.9.2 Products/Solutions/Services offered

- 17.2.9.3 Recent developments

- 17.2.9.3.1 Product launches and enhancements

- 17.2.9.3.2 Deals

- 17.2.9.3.3 Expansions

- 17.2.10 DASSAULT SYSTEMES

- 17.2.10.1 Business overview

- 17.2.10.2 Products/Solutions/Services offered

- 17.2.10.3 Recent developments

- 17.2.10.3.1 Deals

- 17.2.1 SYNCRON

- 17.3 OTHER PLAYERS

- 17.3.1 CRYOTOS

- 17.3.2 EMAINT

- 17.3.3 ERPAG

- 17.3.4 MEGAVENTORY

- 17.3.5 UPKEEP

- 17.3.6 INFRAON

- 17.3.7 VALUEAPEX

- 17.3.8 MPULSE SOFTWARE

- 17.3.9 ANTMYERP

- 17.3.10 LIMBLE CMMS

- 17.3.11 FLEETABLE 290 17.3.12 VERUSEN

- 17.3.13 MASTEK

- 17.3.14 RASEED

- 17.3.15 PARTSCLOUD

- 17.3.16 SPARETECH

- 17.3.17 PARTFUL

- 17.3.18 FACILIO

- 17.3.19 TOOLSGROUP

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2019-2024

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 IMPACT OF PORTER'S FIVE FORCES ON SPARE PARTS MANAGEMENT MARKET

- TABLE 4 GDP PERCENTAGE CHANGE, BY KEY COUNTRIES, 2021-2029

- TABLE 5 SPARE PARTS MANAGEMENT MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 6 AVERAGE SELLING PRICE OF SPARE PARTS MANAGEMENT, BY REGION, 2024-2025

- TABLE 7 SPARE PARTS MANAGEMENT MARKET: LIST OF KEY CONFERENCES AND EVENTS, 2025-2026

- TABLE 8 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 9 LIST OF GRANTED PATENTS IN SPARE PARTS MANAGEMENT MARKET, 2022-2021

- TABLE 10 TOP USE CASES AND MARKET POTENTIAL

- TABLE 11 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 12 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS (%)

- TABLE 18 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 19 SPARE PARTS MANAGEMENT MARKET: UNMET NEEDS IN KEY END-USER INDUSTRIES

- TABLE 20 SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 21 SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 22 SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 23 SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 24 SOLUTIONS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 25 SOLUTIONS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 26 PLANNING & FORECASTING: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 27 PLANNING & FORECASTING: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 28 PROCUREMENT & ORDER MANAGEMENT: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 29 PROCUREMENT & ORDER MANAGEMENT: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 30 INVENTORY MANAGEMENT: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 31 INVENTORY MANAGEMENT: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 SPARE PARTS TRACKING & AUTOMATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 33 SPARE PARTS TRACKING & AUTOMATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 34 REPORTING & ANALYTICS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 35 REPORTING & ANALYTICS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 OTHERS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 37 OTHERS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 38 SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 39 SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 40 PROFESSIONAL SERVICES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 41 PROFESSIONAL SERVICES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 42 TRAINING & CONSULTATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 43 TRAINING & CONSULTATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 44 INTEGRATION & IMPLEMENTATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 45 INTEGRATION & IMPLEMENTATION: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 46 SUPPORT & MAINTENANCE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 47 SUPPORT & MAINTENANCE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 49 SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 50 STANDALONE SPM SOFTWARE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 51 STANDALONE SPM SOFTWARE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 52 INTEGRATED SPM SOFTWARE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 53 INTEGRATED SPM SOFTWARE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 54 SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 55 SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT TYPE, 2025-2030 (USD MILLION)

- TABLE 56 ON-PREMISES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 57 ON-PREMISES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 CLOUD: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 59 CLOUD: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 60 SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 61 SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 62 LARGE ENTERPRISES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 63 LARGE ENTERPRISES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 64 SMES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 65 SMES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 66 SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 67 SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 68 MANUFACTURING: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 69 MANUFACTURING: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 70 TRANSPORTATION & LOGISTICS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 71 TRANSPORTATION & LOGISTICS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 72 CONSTRUCTION & REAL ESTATE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 CONSTRUCTION & REAL ESTATE: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 HEALTHCARE & LIFE SCIENCES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 75 HEALTHCARE & LIFE SCIENCES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 ENERGY & UTILITIES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 ENERGY & UTILITIES: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 IT & TELECOM: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 79 IT & TELECOM: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 OIL & GAS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 OIL & GAS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 OTHER VERTICALS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 83 OTHER VERTICALS: SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 SPARE PARTS MANAGEMENT MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 85 SPARE PARTS MANAGEMENT MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 87 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 88 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 89 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 90 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 91 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 92 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 93 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 94 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 95 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 96 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 97 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 98 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 99 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 101 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 102 US: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 103 US: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 104 CANADA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 105 CANADA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 106 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 107 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 108 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 109 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 110 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 111 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 112 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 113 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 114 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 115 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 116 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 117 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 118 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 119 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 120 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 121 EUROPE: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 122 UK: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 123 UK: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 124 GERMANY: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 125 GERMANY: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 126 FRANCE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 127 FRANCE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 128 ITALY: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 129 ITALY: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 130 REST OF EUROPE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 131 REST OF EUROPE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 132 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 133 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 134 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 135 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 136 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 137 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 138 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 139 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 140 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 141 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 142 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 143 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 144 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 145 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 146 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 147 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 148 CHINA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 149 CHINA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 150 INDIA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 151 INDIA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 152 JAPAN: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 153 JAPAN: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 154 REST OF ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 155 REST OF ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 163 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 164 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 169 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 170 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 171 MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 172 GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 173 GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 174 GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 175 GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 176 SAUDI ARABIA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 177 SAUDI ARABIA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 178 UAE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 179 UAE: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 180 OTHER GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 181 OTHER GCC COUNTRIES: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 182 SOUTH AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 183 SOUTH AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 184 REST OF MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 185 REST OF MIDDLE EAST & AFRICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 186 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 187 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 188 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2020-2024 (USD MILLION)

- TABLE 189 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY SOLUTION, 2025-2030 (USD MILLION)

- TABLE 190 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2020-2024 (USD MILLION)

- TABLE 191 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY PROFESSIONAL SERVICE, 2025-2030 (USD MILLION)

- TABLE 192 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 193 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 194 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2020-2024 (USD MILLION)

- TABLE 195 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY DEPLOYMENT MODE, 2025-2030 (USD MILLION)

- TABLE 196 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 197 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 198 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2020-2024 (USD MILLION)

- TABLE 199 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 200 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 201 LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 202 BRAZIL: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 203 BRAZIL: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 204 MEXICO: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 205 MEXICO: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 206 REST OF LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2020-2024 (USD MILLION)

- TABLE 207 REST OF LATIN AMERICA: SPARE PARTS MANAGEMENT MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 208 SPARE PARTS MANAGEMENT MARKET: OVERVIEW OF COMPETITIVE STRATEGIES: 2022-2025

- TABLE 209 SPARE PARTS MANAGEMENT MARKET: DEGREE OF COMPETITION, 2024

- TABLE 210 SPARE PARTS MANAGEMENT MARKET: REGION FOOTPRINT

- TABLE 211 SPARE PARTS MANAGEMENT MARKET: OFFERING FOOTPRINT

- TABLE 212 SPARE PARTS MANAGEMENT MARKET: TYPE FOOTPRINT

- TABLE 213 SPARE PARTS MANAGEMENT MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 214 SPARE PARTS MANAGEMENT MARKET: ORGANIZATION SIZE FOOTPRINT

- TABLE 215 SPARE PARTS MANAGEMENT MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 216 SPARE PARTS MANAGEMENT MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 217 SPARE PARTS MANAGEMENT MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, 2022-OCTOBER 2025

- TABLE 218 SPARE PARTS MANAGEMENT MARKET: DEALS, 2022-AUGUST 2025

- TABLE 219 SPARE PARTS MANAGEMENT MARKET: EXPANSIONS, 2022-MARCH 2025

- TABLE 220 SYNCRON: COMPANY OVERVIEW

- TABLE 221 SYNCRON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 SYNCRON: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 223 SYNCRON: DEALS

- TABLE 224 IFS: COMPANY OVERVIEW

- TABLE 225 IFS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 IFS: DEALS

- TABLE 227 BAXTER PLANNING: COMPANY OVERVIEW

- TABLE 228 BAXTER PLANNING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 229 BAXTER PLANNING: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 230 BAXTER PLANNING: DEALS

- TABLE 231 PTC: COMPANY OVERVIEW

- TABLE 232 PTC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 233 PTC: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 234 PTC: DEALS

- TABLE 235 FIIX: COMPANY OVERVIEW

- TABLE 236 FIIX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 FIIX: DEALS

- TABLE 238 SAP: COMPANY OVERVIEW

- TABLE 239 SAP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 240 SAP: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 241 SAP: DEALS

- TABLE 242 IBM: COMPANY OVERVIEW

- TABLE 243 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 IBM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 245 ORACLE: COMPANY OVERVIEW

- TABLE 246 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 247 ORACLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 248 ORACLE: DEALS

- TABLE 249 TAVANT: COMPANY OVERVIEW

- TABLE 250 TAVANT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 251 TAVANT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 252 TAVANT: DEALS

- TABLE 253 TAVANT: EXPANSIONS

- TABLE 254 DASSAULT SYSTEMES: COMPANY OVERVIEW

- TABLE 255 DASSAULT SYSTEMES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 256 DASSAULT SYSTEMES: DEALS

List of Figures

- FIGURE 1 SPARE PARTS MANAGEMENT MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 SPARE PARTS MANAGEMENT MARKET: RESEARCH DESIGN

- FIGURE 3 SPARE PARTS MANAGEMENT MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH (SUPPLY SIDE): COLLECTIVE REVENUE OF SPARE PARTS MANAGEMENT VENDORS

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2 (DEMAND SIDE): REVENUE GENERATED FROM OFFERINGS

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2 (DEMAND SIDE): SPARE PARTS MANAGEMENT MARKET

- FIGURE 8 SPARE PARTS MANAGEMENT MARKET: DATA TRIANGULATION

- FIGURE 9 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 10 GLOBAL SPARE PARTS MANAGEMENT MARKET, 2025-2030

- FIGURE 11 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN SPARE PARTS MANAGEMENT MARKET (2022-2025)

- FIGURE 12 DISRUPTIVE TRENDS IMPACTING GROWTH OF SPARE PARTS MANAGEMENT MARKET

- FIGURE 13 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS IN SPARE PARTS MANAGEMENT MARKET, 2025

- FIGURE 14 ASIA PACIFIC TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 15 RISING EQUIPMENT UPTIME DEMANDS AND SERVICE COMPLEXITY TO DRIVE MARKET

- FIGURE 16 PROFESSIONAL SERVICES SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 17 STANDALONE SPM SOFTWARE SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 18 MANUFACTURING TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 19 NORTH AMERICA TO EMERGE AS MOST SIGNIFICANT MARKET IN NEXT FIVE YEARS

- FIGURE 20 SPARE PARTS MANAGEMENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 SPARE PARTS MANAGEMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 22 SPARE PARTS MANAGEMENT MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 23 SPARE PARTS MANAGEMENT MARKET: ECOSYSTEM ANALYSIS

- FIGURE 24 AVERAGE SELLING PRICE OF SPARE PARTS MANAGEMENT, BY OFFERING, 2024-2025

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 SPARE PARTS MANAGEMENT MARKET: INVESTMENT AND FUNDING SCENARIO

- FIGURE 27 PATENTS APPLIED AND GRANTED, 2015-2025

- FIGURE 28 FUTURE APPLICATIONS OF SPARE PARTS MANAGEMENT

- FIGURE 29 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- FIGURE 30 SPARE PARTS MANAGEMENT MARKET: DECISION-MAKING FACTORS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- FIGURE 32 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- FIGURE 33 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 34 SOLUTIONS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 35 STANDALONE SPM SOFTWARE SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 36 ON-PREMISES SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 37 LARGE ENTERPRISES SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 38 MANUFACTURING SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 39 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 40 NORTH AMERICA: SPARE PARTS MANAGEMENT MARKET SNAPSHOT

- FIGURE 41 ASIA PACIFIC: SPARE PARTS MANAGEMENT MARKET SNAPSHOT

- FIGURE 42 SPARE PARTS MANAGEMENT MARKET: REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024 (USD MILLION)

- FIGURE 43 SPARE PARTS MANAGEMENT MARKET SHARE ANALYSIS, 2024

- FIGURE 44 SPARE PARTS MANAGEMENT MARKET: PRODUCT COMPARISON

- FIGURE 45 SPARE PARTS MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 46 SPARE PARTS MANAGEMENT MARKET: COMPANY FOOTPRINT

- FIGURE 47 SPARE PARTS MANAGEMENT MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 48 SPARE PARTS MANAGEMENT MARKET: EV/EBITDA OF KEY VENDORS

- FIGURE 49 SPARE PARTS MANAGEMENT MARKET: YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY MANUFACTURERS

- FIGURE 50 SAP: COMPANY SNAPSHOT

- FIGURE 51 IBM: COMPANY SNAPSHOT

- FIGURE 52 ORACLE: COMPANY SNAPSHOT

- FIGURE 53 DASSAULT SYSTEMES: COMPANY SNAPSHOT